Jack Monroe in a single nook, the Don’t Pay marketing campaign within the different…

You could have heard numerous leftfield approaches to rising payments within the UK, from advisors on TV to radicals on-line advising you what to do (or not do) within the face of big vitality payments.

Are you able to merely refuse to pay? Or can you’re taking a much less radical method?

FIRST STEPS

First off, TALK to your vitality provider. Can they assist by placing you on a fairer fee scheme? Most suppliers need some form of common fee from their prospects but when they’re conscious of your bother paying the quantity you’ve been set, they might simply need to see how a lot you’ll be able to pay.

Change Your Provider

Altering your vitality provider is the subsequent step, in case your present one gained’t play ball. The Super Smart Energy Savers Report is price studying: it was arrange earlier this 12 months to supply choices for folks having bother paying their vitality payments, and MoneyMagpie have an ideal comparability device here.

JACK MONROE

Anti-poverty campaigner Jack Monroe has been quoted as advising these having bother altering their vitality provider to arrange a standing order for an quantity they will afford, as a substitute of their present direct debit.

“They gained’t prefer it however… they gained’t be capable of change the quantity on a standing order like they will on direct debit. It places YOU again in management. In the event that they use threatening/bullying techniques to attempt to intimidate you into altering it again or paying extra, make a grievance to the Ombudsman. For each grievance they obtain, the vitality co will get fined round £375. They’d haven’t any qualms about fining you. Hit them the place it hurts them.”

The mass media are reporting that the common UK family could expertise an vitality invoice rise of as much as £4000, with many saying they will’t afford the worth improve. Some are already paying almost £400 per invoice.

DON’T PAY

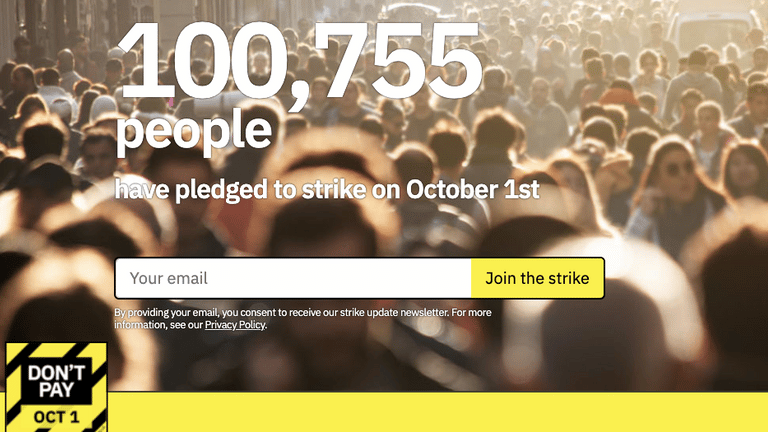

Extra radically, over 100,000 folks have signed as much as the Don’t Pay campaign, which began in June and which claims: “It’s a easy thought: We demand the Authorities scrap the vitality value rises and ship inexpensive vitality for all. We’ll construct one million pledges and by October 1 if the Authorities and vitality firms fail to behave we’ll cancel our direct debits.”

“Even when a fraction of these of us who’re paying by direct debit cease our funds, will probably be sufficient to place vitality firms in deep trouble, and so they know this. We need to deliver them to the desk and pressure them to finish this disaster.”

THE COUNTER-ARGUMENT

Jack Monroe, nonetheless, does NOT essentially assume it is a nice thought as a result of, she says, “in case your vitality firm gained’t allow you to change your direct debit, you’ll be able to cancel it. Word down the banking particulars and reference quantity and arrange a standing order for the quantity you ACTUALLY use/can afford as a substitute.”

Monroe goes on to say that you need to fastidiously verify the phrases and circumstances of your settlement together with your vitality firm. She additionally directs folks on prepay meters to assert advantages and help out there to them, directing them to the Gasoline Financial institution web site.

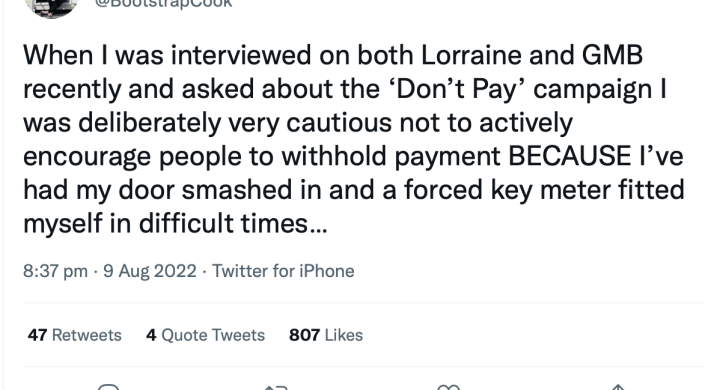

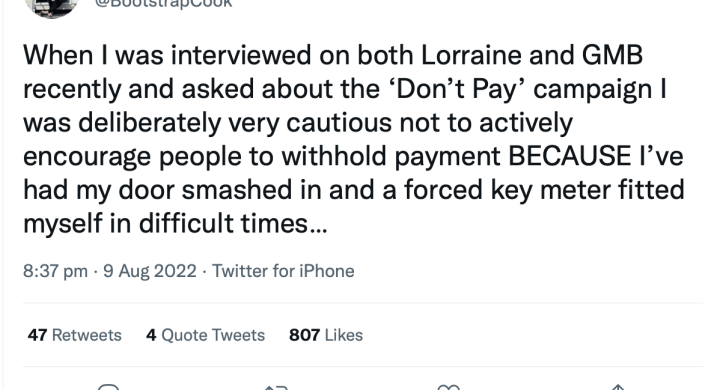

Her ultimate phrase on the Don’t Pay scheme is that this: “Once I was interviewed on each Lorraine and GMB just lately and requested concerning the ‘Don’t Pay’ marketing campaign, I used to be intentionally very cautious to not actively encourage folks to withhold fee BECAUSE I’ve had my door smashed in and a compelled key meter fitted myself in troublesome occasions.

My credit standing is STILL recovering from CCJs from that interval, so the LAST factor I’d do is to advise folks to take any motion that may result in related penalties.”

Jasmine Birtle’s Says

“I’m very cautious of the Don’t Pay marketing campaign and I feel that anybody contemplating merely not paying ought to think about the potential penalties. Power payments are ‘precedence funds’ and never paying them, or not even making an attempt to barter together with your vitality supplier, can significantly harm your credit standing. The vitality firms can cross your debt on to debt assortment companies which, as Jack Monroe mentions, can contain stop disagreeable run-ins with bailiffs.

“It actually is healthier to talk first to your vitality supplier – many have charitable funds that they will use to assist – and likewise chatting with one of many free debt recommendation charities like StepChange, Citizen’s Recommendation and Group Cash Recommendation as in addition they might be able to level you within the route of additional assist. Converse to your native Council too as they will typically assist when you haven’t certified for advantages or different assist.”

{kind=link}