Controlling 9% of the world’s manufacturing, Freeport-McMoRan (NYSE: FCX) is certainly one of largest producers of copper on the earth.

Why ought to traders care?

As a result of the long-term future for copper costs is wanting extraordinarily bullish.

Renewable vitality is a big long-term tailwind for copper demand.

Electrical automobiles, energy grids, and wind and photo voltaic vitality buildouts are all going to require extra copper. Renewable vitality methods use, on common, 5 instances extra copper than conventional methods.

In the meantime, an increasing number of of our vitality methods are transitioning to renewables.

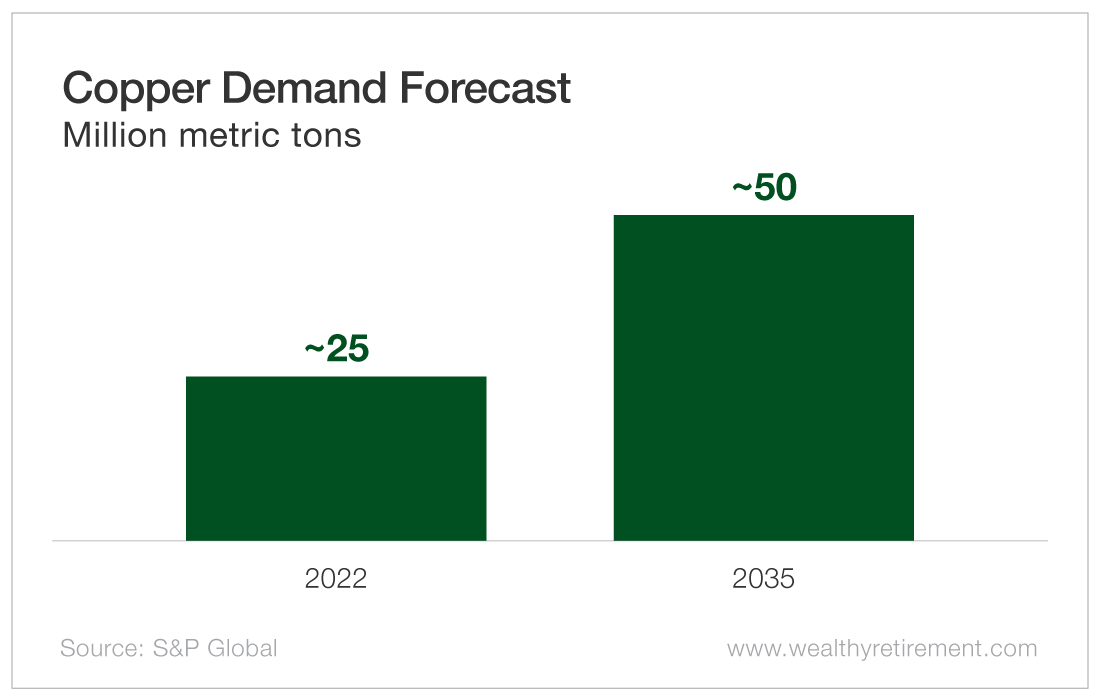

The estimates of how way more annual copper manufacturing we’re going to want are staggering.

S&P World, for instance, is estimating that copper demand goes to double by 2035.

To place into perspective how wild copper demand goes to be, contemplate that S&P’s numbers undertaking that we’ll use extra copper between 2021 and 2050 than we did from 1900 to 2021.

Whereas demand is exploding, there additionally seems to be a provide drawback.

After a decade of underinvestment, there are only a few new copper initiatives scheduled to come back to manufacturing in time to satisfy the projected demand.

That is regarding as a result of it takes 10 to twenty years to allow and construct new copper mines.

Easy economics tells us what’s going to occur within the copper market. Large demand and a scarcity of provide merely will drive the value of copper increased.

That’s the solely method to carry new provide to market.

For producers like Freeport that have already got large quantities of current copper manufacturing, an increase in copper costs goes to create large will increase in money movement.

Just lately, the value of copper has been hovering round $4 per pound.

For Freeport particularly, each $0.10 improve within the value of copper ends in a rise of $335 million in working money movement.

Unquestionably, this firm has lots to realize from long-term rising copper costs.

However proper now, we have to contemplate whether or not Freeport’s market valuation is engaging at in the present day’s costs.

With copper at $4 per pound, Freeport ought to generate $7.5 billion in working money movement this yr.

With a present market valuation (enterprise worth) of just below $60 billion, Freeport is buying and selling at eight instances working money movement.

That doesn’t strike me as costly… nevertheless it isn’t drop-dead low-cost both.

In case you imagine that copper costs are headed increased (which I do), then the $10.5 billion in working money movement that the corporate initiatives producing at $5 per pound copper costs is probably going extra related.

At that stage of working money movement, Freeport’s $60 billion enterprise worth would have the corporate buying and selling at 5.7 instances working money movement. That’s a sexy a number of.

And I don’t assume $5 per pound goes to be the highest for copper pricing. I count on copper costs to common significantly increased than that over the following decade.

Whereas I like this inventory for the long run, I don’t assume there’s a actual rush to purchase it.

With some weak point within the international financial system occurring, there’s a likelihood we might see a short-term dip in copper costs. That might provide an opportunity to purchase Freeport at a fair higher value.

The Worth Meter charges Freeport-McMoRan as “Barely Undervalued,” with a notice that this is a chance for traders keen to attend for the long-term bullish copper story to play out.

{kind=link}