There are a lot of good methods to repay a mortgage quicker. Most lenders will suggest that householders with a traditional 30-year mortgage merely refinance right into a shorter 15-year time period. However one other strong possibility is for a borrower to easily add slightly more money on prime of their month-to-month fee every month to go in direction of the principal.

As a financially savvy home-owner for over 17 years now, I’ve been on the lookout for each trick I can to eradicate my mortgage as rapidly as doable. I’ve tried each of those choices, and after a variety of evaluation, that is what I can inform you:

The choice of whether or not householders ought to refinance or pay further mortgage principal will probably be a private one. Each choices will assist to speed up the payoff timeline and scale back the entire curiosity paid to the lender over the lifetime of the mortgage.

Nevertheless, there’s extra to it than simply cash. Every path comes with its personal set of professionals and cons, and debtors should contemplate them each.

On this publish, we’ll totally discover every of those choices and the way they’ll affect a home-owner’s funds.

Why Refinance or Make Further Funds within the First Place?

For anybody on this scenario, let me start by saying there isn’t a mistaken reply right here. Each methods can shave years off the reimbursement schedule in addition to dramatically scale back how a lot curiosity a borrower can pay over the lifetime of the mortgage.

To raised perceive why that’s, it helps to take a better take a look at how the cash inside a mortgage fee truly will get used.

What’s Inside a Mortgage Fee

Do not forget that lenders construction mortgage funds utilizing one thing referred to as an amortization schedule. Every fee may have two fundamental elements:

- Principal – The portion that goes in direction of paying off the mortgage stability

- Curiosity – The portion that the lender retains as fee for loaning out the cash

For instance, assume somebody needs to purchase a $250,000 dwelling. They put down a 20 p.c down fee ($50,000) and borrow the remaining $200,000 with a 30-year mortgage at a hard and fast fee of three.25 p.c.

The month-to-month fee can be $870.00. Below this amortization schedule, the primary fee would break down as follows:

- Principal: $328.33

- Curiosity: $541.67

As successive funds are remodeled the subsequent 30 years, the proportion of this fee going in direction of the principal will progressively improve whereas the curiosity portion will lower. Lenders do that on objective as a result of they wish to acquire the curiosity they’re owed as quickly as doable.

How a 15-Yr Refinance Modifications Your Fee

Clearly, when somebody refinances right into a 15-year mortgage, they may pay again their mortgage in 15 years. However what won’t be as well-known is how a lot of their mortgage fee will now go in direction of the principal moderately than the curiosity.

As an example this, right here is similar mortgage however modified to a 15-year time period with a 2.50 p.c mounted fee. (It’s frequent for lenders to supply charges which might be 0.5 to 0.75 much less on 15-year mortgages.)

- Fee: $1,333.00

- Principal: $916.33

- Curiosity: $416.67

The month-to-month fee is, after all, considerably larger due to the shorter interval. However the borrower can also be paying much more every month in direction of the principal and fewer in curiosity. That is going to assist them to construct fairness quicker whereas on the identical time minimizing the general value of the mortgage by means of curiosity discount.

How Further Principal Funds Change Your Mortgage

As a result of most lenders welcome the chance to be paid again forward of schedule, they’ll enable debtors so as to add more money on prime of their mortgage funds. This cash is then utilized in direction of the principal portion of the mortgage stability.

Further principal funds could be any quantity: $50, $100, $500 … and so forth. It additionally doesn’t should be the identical every time.

As an example, a borrower might begin by including $50 to their mortgage fee, bump this as much as $100 just a few years later, after which drop all the way down to $0 if different monetary priorities come up. There is no such thing as a dedication.

The extra money {that a} borrower provides to their mortgage fee and the longer they keep it up, the quicker they may repay their mortgage. And by taking years off the again finish of their fee schedule, they can even save themselves the curiosity on these funds they’ve erased.

Easy methods to Decide If You Ought to Refinance or Make Further Funds

With regards to any monetary resolution, I imagine the most effective place to begin is with the numbers. The numbers provide you with a strong basis that can assist you justify one path or the opposite. From there, an individual can then contemplate qualitative elements earlier than making their final resolution.

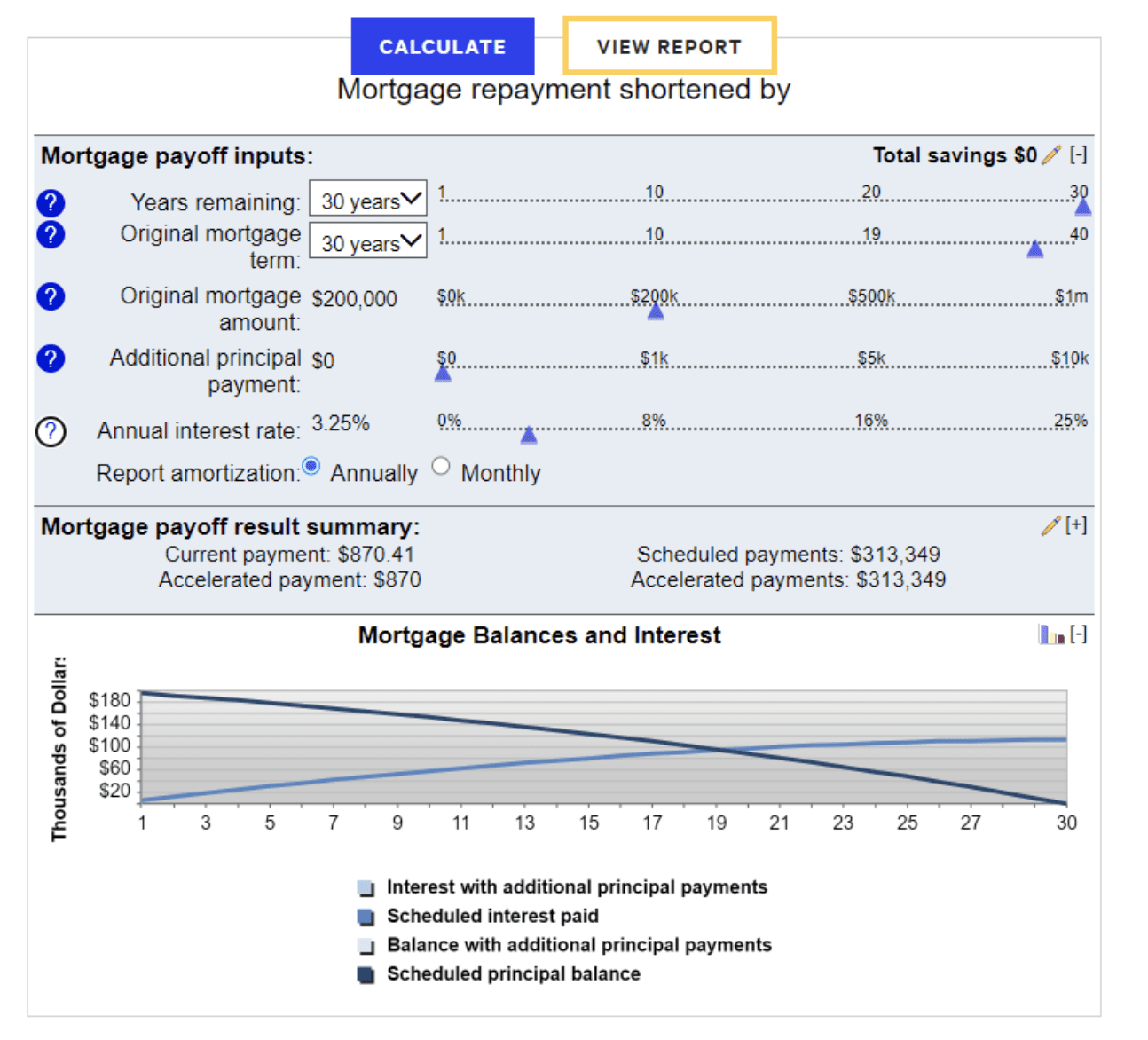

For the monetary evaluation, you may make any of those calculations your self by utilizing this free online mortgage calculator.

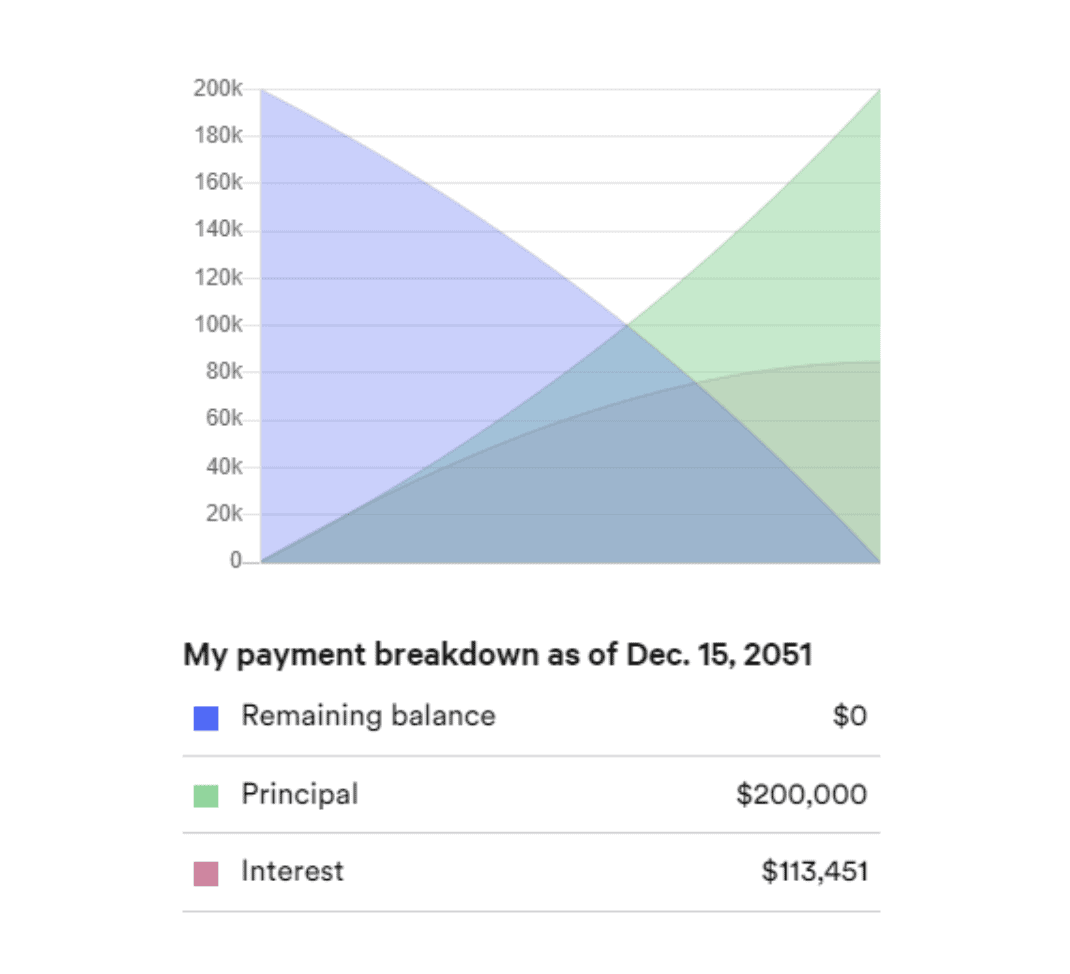

Customary 30-Yr Mortgage

For the baseline calculation, let’s use the identical variables as earlier than assuming a traditional 30-year mortgage:

- Mortgage quantity: $200,000 ($250,000 minus a 20 p.c down fee)

- Rate of interest: 3.25 p.c.

(Be aware: For simplicity, we’ll ignore closing prices, factors, and so forth.)

Below these standards, the entire curiosity paid over the lifetime of the mortgage can be $113,349.

15-Yr Refinance Possibility

Subsequent, let’s have a look at how this situation would change for somebody who refinanced from a 30-year to a 15-year time period.

In actuality, debtors can refinance at any time throughout their mortgage. Nevertheless, for the sake of this instance, we’ll assume we refinance proper from Day-1.

Once more, keep in mind that the rate of interest on a 15-year mortgage will probably be decrease than a 30-year. On this instance, we’ll once more use 2.50 p.c.

Below this new construction, the entire curiosity paid over the lifetime of the mortgage would solely be $40,044. That’s an astonishing $73,305 lower than the 30-year mortgage!

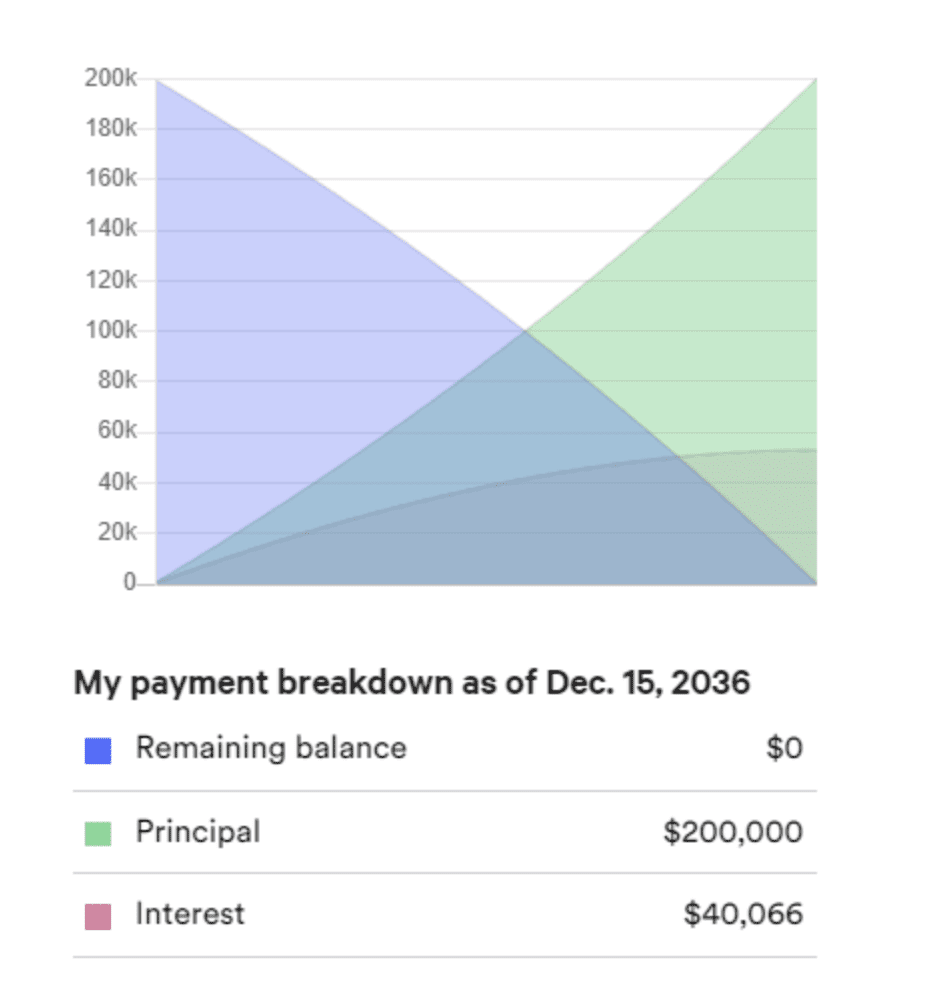

Making Extra Principal Funds

Lastly, let’s contemplate what would occur for somebody who maintains the unique 30-year mortgage however constantly sends in further principal funds.

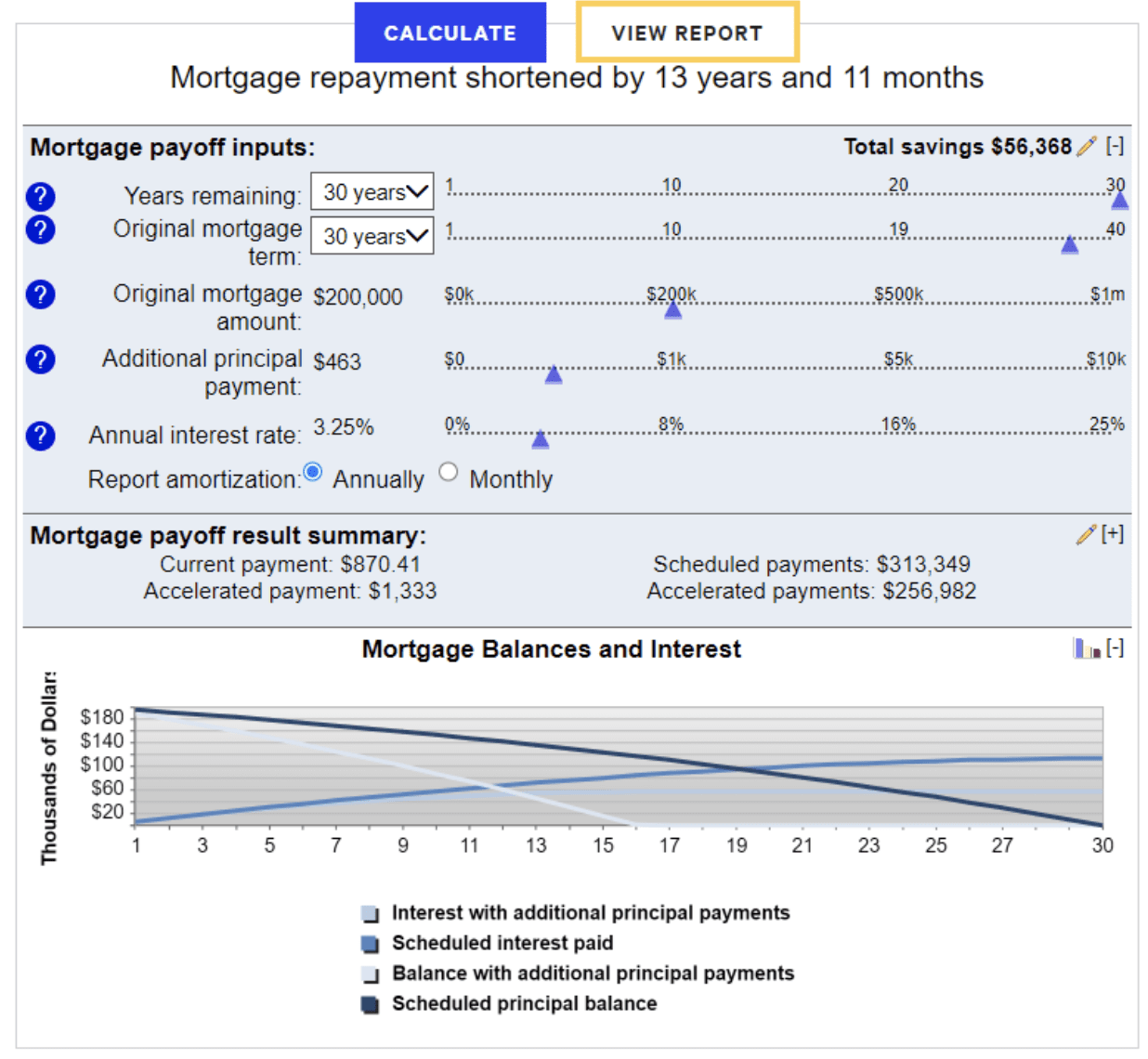

Once more, in actuality, these further funds could be any quantity and made at any time. However for the sake of this instance and to make it a real apples-to-apples comparability, let’s merely add the distinction between the 15 yr and 30-year funds: $463.17 further per thirty days.

Utilizing this technique, the entire curiosity paid over the lifetime of the mortgage would once more drop dramatically to $56,982. That’s a wholesome financial savings of $56,367 lower than the unique timeline.

Nevertheless, it’s additionally nonetheless $16,938 greater than the 15-year refinance possibility. The rationale for that is that the amortization proportions didn’t truly change. The borrower nonetheless paid larger quantities of curiosity at the start of the fee schedule than somebody who took the 15-year possibility.

In consequence, although we deliberately adjusted our month-to-month fee to match the 15-year quantity, not as a lot of that fee was going in direction of the principal. This is the reason the mortgage will truly take 16 years and 1 month to repay in full (versus 15 years).

Different Causes to Refinance or Make Further Funds

As we will see from the earlier instance, somebody who chooses to refinance to the 15-year possibility will in the end save essentially the most quantity of curiosity over the lifetime of the mortgage. However that’s not the one issue that ought to drive this resolution.

There could be a number of different the explanation why a borrower is likely to be completely validated to go down one path or the opposite. Listed below are just a few extra elements to think about.

When Does Refinancing Make Sense?

Right here’s why a borrower would possibly resolve to go together with the 15-year refinance:

- Paying as little curiosity as doable. The considered handing over tens of 1000’s of {dollars} to a financial institution drives some individuals insane. If lowering it as a lot as doable is the borrower’s prime precedence, then the refinance is an effective strategy to go.

- Decide to paying off the mortgage in 15 years. As soon as a borrower refinances to a 15-year time period, good or dangerous, they’re caught with this new fee. This may be precisely the push they should follow their resolution to pay it off as rapidly as doable. However it may well additionally chew them later if the upper fee turns into an excessive amount of of a monetary burden.

- Construct fairness as rapidly as doable. As a result of the next proportion of the month-to-month fee will go in direction of the principal, homebuyers will purchase 2 to three instances extra fairness with every fee than they’d with a 30-year mortgage. Until they plan to ship in a considerable further fee for the subsequent 15 years, the refinance will possible be a more sensible choice.

- They qualify for a refinance. To refinance a mortgage, an individual must be in good monetary standing and have an awesome FICO rating. Somebody with these attributes would possibly wish to seize this chance.

They plan to remain in the home for a very long time. Individuals who plan to reside of their home for a very long time gained’t be as financially preoccupied as those that plan to maneuver in just a few years. This implies they’ll afford to place all of their vitality into paying off the mortgage and taking up the next month-to-month fee.

When Does Paying Further Every Month Make Sense?

Not everybody will wish to go together with a refinance. Right here’s why a borrower would possibly resolve to only make further principal funds every month:

- They’ll’t decide to the upper fee. For the typical home-owner, a 15-year refinance can simply add between $400 to $600 to their month-to-month invoice. In the event that they miss that fee, it may well imply risking foreclosures. If there’s any doubt by a borrower that they’ll’t lock into this larger fee, then the additional fee route could also be higher.

- They need flexibility. What if a home-owner doesn’t wish to be locked into paying an additional $500 per thirty days? What if they need the choice to regulate it as their revenue fluctuates, or shut it off if instances get robust? The additional fee possibility offers them the flexibility to do that.

- Somebody who’s already nicely into their mortgage. When somebody has paid into their mortgage for the previous 10 years or so, they’ve already paid a major quantity of curiosity due to the best way the amortization schedule was structured. Subsequently, refinancing right into a 15-year mortgage would possibly not likely present any benefit.

- There’s no credit score test wanted. If somebody has not too long ago modified jobs or executed one thing which may have jeopardized their credit score rating, then there is a good likelihood they could not qualify for a refinance. However, the additional fee route has no pink tape.

- They plan on promoting the home comparatively quickly. Somebody who plans on shifting could not wish to decide to the next month-to-month fee as a result of they could wish to save up further cash for his or her new home. Or, if the home will get offered and sits available on the market for a number of months, they could not wish to be caught paying this bigger mortgage along with their new dwelling. In that case, utilizing the additional fee route will give them the pliability to modify backwards and forwards between the upper and decrease fee quantities.

Bonus Possibility – The Mortgage Recast

There’s one other strategy to restructure a mortgage with out refinancing or sending in further funds: recasting.

A mortgage recast is when a home-owner makes a request to their lender to have their month-to-month funds recalculated. That is typically after the borrower makes a comparatively massive lump-sum fee, maybe after receiving a small windfall similar to:

- A office bonus

- Inheritance fee

- Fairness from the sale of one other dwelling

All the pieces in regards to the mortgage stays the identical: Rate of interest, the remaining variety of funds, and so forth. With the massive one-time fee, recasting reduces the remainder of the remaining funds.

The large benefit is that with decrease funds the borrower may have better month-to-month money circulation. It additionally helps keep away from refinancing and all of the closing prices that come together with it.

The drawback is that it doesn’t speed up the timeline in any respect. Additionally, as a result of the month-to-month funds are actually smaller, the borrower builds fairness slower and can possible pay extra curiosity than refinancing or making further principal funds.

Ought to I Refinance or Simply Pay Further Mortgage Every Month?

The choice to refinance or pay further mortgage principal will primarily be a matter of private choice. The numbers could inform one story, however there will also be compelling causes for a home-owner to go in a distinct path.

For those who’re contemplating the refinance possibility, attempt a device like Credible*. Quite than logging on to a number of completely different lenders, Credible acts as a one-stop-shop so that you can enter your info and obtain a number of presents with no obligations. From there, you possibly can resolve which lenders will provide you with the most effective supply and make you’re feeling essentially the most comfy.

For those who’re leaning extra in direction of the additional fee possibility, take a superb take a look at your price range and decide how a lot you possibly can afford. If the extra quantity doesn’t convey you near the 15-year possibility, otherwise you merely need the pliability to regulate your fee at will, then simply proceed together with your present mortgage and make further funds as you see match.

Once more, both possibility is sweet. It’s going to simply be a matter of how badly you wish to speed up your timeline and scale back the general curiosity paid. Do not forget that regardless of which method you resolve to go, working down your mortgage goes to assist guarantee your monetary safety for years to come back.

{kind=link}