Warren Buffett simply can’t cease shopping for shares of Occidental Petroleum (NYSE: OXY).

He now holds virtually 25% of all Occidental shares by means of his conglomerate Berkshire Hathaway (NYSE: BRK-A).

However in case you are occupied with proudly owning an oil and fuel producer, I’m undecided Occidental is the one to go for.

Devon Power (NYSE: DVN) is cheaper, is rising sooner and has an intriguing dividend.

With greater than 650,000 barrels per day of manufacturing, Devon is likely one of the largest unbiased producers targeted completely on the USA.

Roughly two-thirds of that manufacturing comes from the extremely prolific Delaware Basin, positioned within the large Permian Basin.

Not like a lot of the bigger oil and fuel producers – which at the moment are planning on holding manufacturing flat – Devon goes to develop in 2023.

Administration’s steering is for year-over-year manufacturing development of 9% per share.

This development is spectacular as a result of Devon goes to perform it whereas nonetheless pumping out vital free money stream. That’s uncommon on this enterprise.

As traders, we wish to see robust free money stream. That is money stream that may be distributed to shareholders as dividends or by means of share repurchases.

Normally, to develop at a virtually double-digit fee, producers should reinvest all their money stream. That leaves little to no free money stream for shareholders.

With practically double-digit development and free money stream, Devon is letting shareholders have their cake and eat it too.

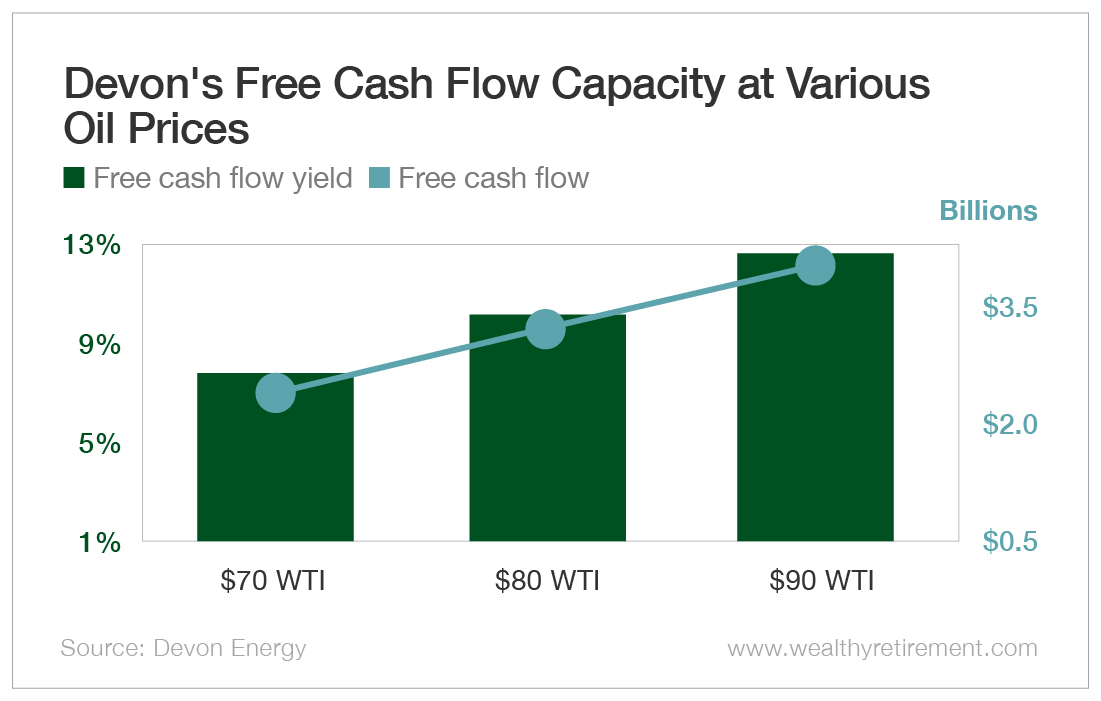

Within the chart beneath, you’ll see that administration has quantified how a lot free money stream the corporate can generate at varied oil costs.

With oil at $70 (round the place we’re in the present day), Devon is predicted to generate practically $3 billion in free money stream for the yr.

That equates to a formidable 8% free money stream yield on Devon’s present share value.

Administration intends to distribute this free money stream to shareholders by means of a mix of dividends and share repurchases.

It’s the dividend that has my consideration.

Devon’s administration adjusts its dividend primarily based on how a lot free money stream the corporate is producing – which means it has a variable dividend.

If oil costs and free money stream go up, administration will enhance the dividend. And vice versa. That’s the reason the Security Internet system gave the corporate an “F” for dividend security again in March.

However has it redeemed itself since?

With oil at $70 at present, Devon’s dividend yield is about 6%.

That appears fairly good when put next with the 1.7% common dividend yield of the businesses within the S&P 500 and the measly 0.9% common dividend yield of the businesses within the Nasdaq.

You must have an opinion on the place oil and fuel costs are going.

Personally, I’m bullish on oil costs.

I imagine that our provide and demand stability for oil goes to be tight within the years forward at the same time as we switch to greener vitality sources.

With Devon buying and selling at an 8% free money stream yield at present oil costs and providing a 6%-plus dividend, I believe this inventory offers a compelling alternative in the present day.

If oil costs go larger, then shopping for Devon Power at present costs goes to work out very effectively.

There’s upside within the inventory, and the 6% dividend can pay you effectively to attend for it to be realized.

Assuming a bullish view on oil costs, The Worth Meter charges Devon Power as “Barely Undervalued.”

{kind=link}