The best investor of all time has made the majority of his cash shopping for dominant manufacturers.

Warren Buffett’s unimaginable 70 years’ value of inventory market success has been constructed on taking large positions in family names.

Buffett’s largest winners embrace American Specific (NYSE: AXP), Coca-Cola (NYSE: KO) and, extra not too long ago, Apple (Nasdaq: AAPL).

These companies’ model power protects them in opposition to competitors and creates pricing energy that enables for robust revenue margins.

And most significantly, it helps these firms develop.

Their robust manufacturers drive earnings development for years and years. And over the long run, it’s earnings development that drives an organization’s inventory value.

With that in thoughts, Harley-Davidson (NYSE: HOG) feels like a worth investor’s dream! Its 120-year-old model is iconic.

The corporate’s model power has created an extremely loyal buyer base and permits Harley-Davidson to cost a premium value for its bikes.

On prime of that, the inventory at present trades at a minuscule seven instances earnings!

It feels like a slam dunk, doesn’t it?

On the floor, sure. However after a bit digging, not a lot.

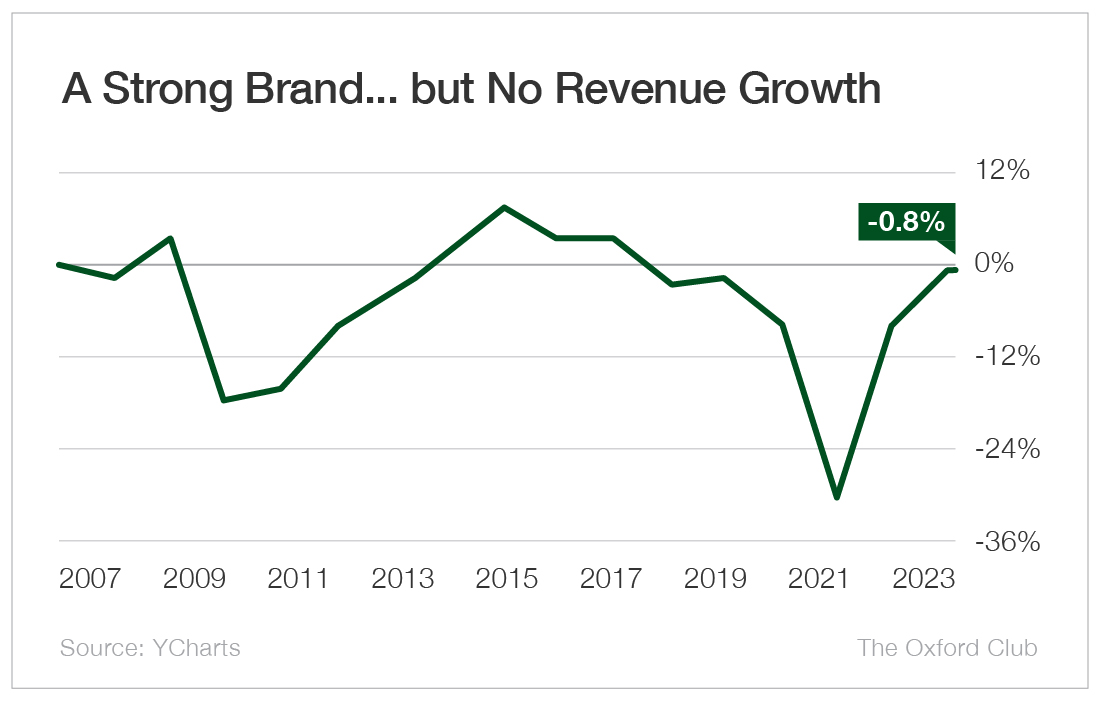

The Harley-Davidson enterprise has stalled.

Actually.

Since 2006, the corporate has not been in a position to develop its gross sales in any respect.

In truth, Harley-Davidson’s income is definitely down barely from the place it was 17 years in the past.

The corporate’s bike gross sales reached a peak of 260,000 in 2006.

However since then, annual gross sales have steadily declined.

Final yr, Harley-Davidson’s gross sales dropped to solely 178,000 bikes.

Thank goodness the corporate has been in a position to elevate costs, or else income would’ve dropped off a cliff!

And whereas the income story appears to be like grim, the underside line appears to be like even worse.

Harley-Davidson’s internet revenue is down about 29% since 2006.

That may be a brutal disappointment for shareholders.

Based mostly on that decline in internet revenue, it’s no shock that Harley-Davidson’s share value has carried out terribly since 2006.

Whereas the S&P 500 is up 241%, shares of Harley-Davidson have misplaced greater than half their worth.

Going ahead, I don’t assume issues are going to get any simpler for the corporate.

In 1985, the typical motorbike purchaser was 27 years outdated.

At this time, the typical purchaser is over 50.

The corporate’s loyal buyer base is getting outdated, and the subsequent era isn’t all that within the Harley-Davidson product.

The model nonetheless has unimaginable power, however it exists solely inside that buyer group, which is getting older out of bike purchases.

Moreover, the corporate has to cope with the world’s transition away from combustion engine automobiles.

That may be a vital menace.

And Harley-Davidson’s LiveWire electrical motorbike is anticipated to ship simply 600 to 1,000 models this yr and lose $115 million to $125 million.

It’s not possible to foretell how a lot success – if any – Harley-Davidson could have with this product.

On condition that earnings have been in decline since 2006 and there’s no purpose to assume that may change going ahead, I don’t see any purpose to purchase shares of Harley-Davidson.

Even with the inventory buying and selling at simply seven instances earnings, The Worth Meter charges Harley-Davidson as being “Barely Overvalued.”

You probably have a inventory that you just’d prefer to have rated by The Worth Meter, depart the ticker image within the feedback part.

{kind=link}