Airbnb inventory (NASDAQ:ABNB) has remodeled right into a cash-printing machine backed by robust income development and its profitable, high-margin enterprise mannequin. As one of many main reserving platforms favored by vacationers searching for distinctive lodging, in addition to one-of-a-kind experiences, Airbnb maintains its momentum, steadily broadening its model attain. Final 12 months’s outcomes illustrated this theme, whereas consensus estimates level to this pattern lasting for years to return. Thus, I stay invested and bullish on ABNB inventory.

Journey Trade Momentum Drives High and Backside-line Beneficial properties

Fiscal 2023 was a powerful 12 months for Airbnb, with the journey trade’s robust momentum driving strong prime and bottom-line positive factors. One would suppose that following 2021-2022’s revenge journey post-pandemic interval, the journey trade would take a breather. Nevertheless, the post-pandemic restoration momentum remained robust final 12 months, extending trade positive factors.

Particularly, in response to Eurostat, in 2023, the variety of nights booked in Europe grew by 171 million or 6.3% in contrast with 2022, pushed by notable development in each worldwide and home vacationers. The truth is, the approximate variety of nights spent at vacationer lodging throughout the 12 months reached 2.92 billion within the continent. This surpassed the pre-pandemic 2019 stage of two.87 billion by 1.6%, setting a brand new report 12 months. Globally, Statista reported that the dimensions of the worldwide tourism market grew by practically 14% final 12 months.

Being the world’s second-most visited lodging and lodge platform, solely behind Reserving Holdings (NASDAQ:BKNG) Reserving, Airbnb loved an natural tailwind from the journey trade’s robust traction. This led to Airbnb recording vital development throughout its key metrics and general financials.

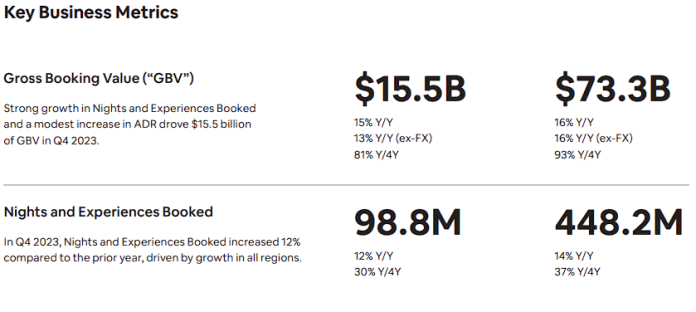

Particularly, nights and experiences booked grew by 14% to 448.2 million for the 12 months, pushed by development in all areas. This development, mixed with increased common costs on nights and experiences, led to Airbnb posting gross reserving worth (GBV) development of 16% to $73.3 billion.

Airbnb’s take fee on this quantity was comparatively steady year-over-year (14.3% in This autumn, for context), so the expansion in GBV and a smooth however favorable foreign money translation led to total revenues growing by 18% for the year to $9.9 billion.

What I like about Airbnb’s enterprise mannequin is that it’s extremely lean and capital-light, that means that the corporate can obtain large margins. The extra Airbnb scales its revenues, the upper its margins go, particularly given administration has targeted intently on controlling bills in current quarters.

Certainly, adjusted EBITDA in 2023 landed at $3.7 billion, implying an adjusted EBITDA margin of ~37%, up from final 12 months’s ~35%. Airbnb’s adjusted internet revenue (which excludes some notable positive factors recorded in 2023 that inflated GAAP internet revenue) additionally had a powerful margin of about 29%.

Nonetheless, observe that the entire reserving/reservations enterprise mannequin could be very a lot a cash-flow enterprise mannequin. For that reason, I imagine that Airbnb might be higher assessed by its free money stream. That is the place the enterprise actually shined, posting a report free cash flow of $3.8 billion, up from $3.4 billion final 12 months, implying a large free money stream margin of 39%.

Double-Digit Development to Persist For Years To Come

Airbnb’s double-digit development seems poised to persist for years to return. In my opinion, this may maintain the inventory’s bullish sentiment.

So far as this 12 months goes, administration said that 2024 began robust and expects revenues in Q1 to land between $2.03 billion and $2.07 billion, implying year-over-year development of 12% to 14%. Primarily based on this and the journey trade’s ongoing momentum, consensus estimates level towards Fiscal 2024 revenues of $11.08 billion, suggesting a year-over-year enhance of 11.8%.

Impressively, Airbnb’s consensus income estimates forecast double-digit income yearly all through 2033. Positive, after just a few years, projecting revenues turns into extremely speculative. Nonetheless, this reveals the present sentiment, which ought to offer you an thought of how the market feels in regards to the firm’s development prospects.

Moreover, free money stream development is anticipated to observe swimsuit and land at $4.04 billion and $4.62 billion in 2024 and 2025, charting an analogous trajectory. Subsequently, the corporate seems set to continue to grow quickly and printing money for years to return.

Is ABNB Inventory a Purchase, In keeping with Analysts?

Relating to Wall Avenue’s view, Airbnb has gathered blended emotions. The inventory includes a Maintain consensus ranking based mostly on 5 Buys, 19 Holds, and 4 Sells assigned up to now three months. At $144.80, the typical Airbnb stock price target implies 13.7% draw back potential.

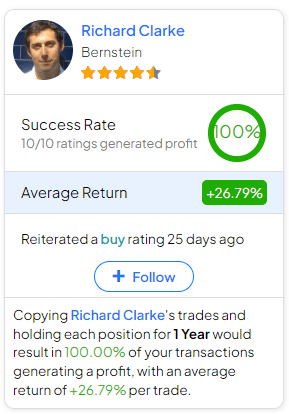

In case you’re uncertain which analyst you need to observe if you wish to commerce ABNB inventory, essentially the most correct analyst masking the inventory (on a one-year timeframe) is Richard Clarke from Bernstein. He boasts a mean return of 26.79% per ranking and a 100% success fee. Click on on the picture under to be taught extra.

The Takeaway

To sum up, I imagine that Airbnb’s rise as a cash-generating machine is simple. With a enterprise mannequin that thrives organically on the again of the journey trade’s development mixed with juicy margins, Airbnb’s free money stream technology prospects are actually fascinating.

Additional, Wall Avenue predicts double-digit income and free money stream development extending far into the longer term, suggesting that the inventory’s funding outlook stays promising. In gentle of this, I’m feeling assured about sticking with Airbnb inventory for the longer term and staying optimistic about its long-term story.

The put up Money-Printing Machine for the Lengthy Time period – TipRanks Monetary Weblog appeared first on FinanceGrabber.

{kind=link}