Final December, I put Fleetcor Applied sciences (NYSE: FLT) via The Worth Meter.

Fleetcor supplies cost playing cards for its 100,000-plus clients to offer to their staff to allow them to pay for company bills, like gasoline and lodging.

These playing cards enhance the management these clients have over worker spending and get rid of the executive prices concerned in submitting and processing expense studies.

Fleetcor was based as a tiny enterprise with lower than $25 million in income by Ron Clarke in 2000.

Over the previous twenty years, Clarke grew the corporate into one which generated $3.4 billion in income and virtually $1 billion in web earnings final 12 months.

With this unbelievable development, you gained’t be shocked to study that Fleetcor’s inventory has carried out extremely effectively.

Since Fleetcor went public in 2010, the inventory has elevated eightfold and has vastly outperformed the general market. Clarke nonetheless runs Fleetcor, and he personally owns greater than $1 billion value of inventory.

Clarke has made himself and his shareholders wealthy.

Final December, I rated Fleetcor’s inventory as being “Barely Undervalued.”

I wrote, “Anytime we will purchase shares of an organization with these traits at all-time low valuations, we must always do it. Alternatives like this are few and much between.”

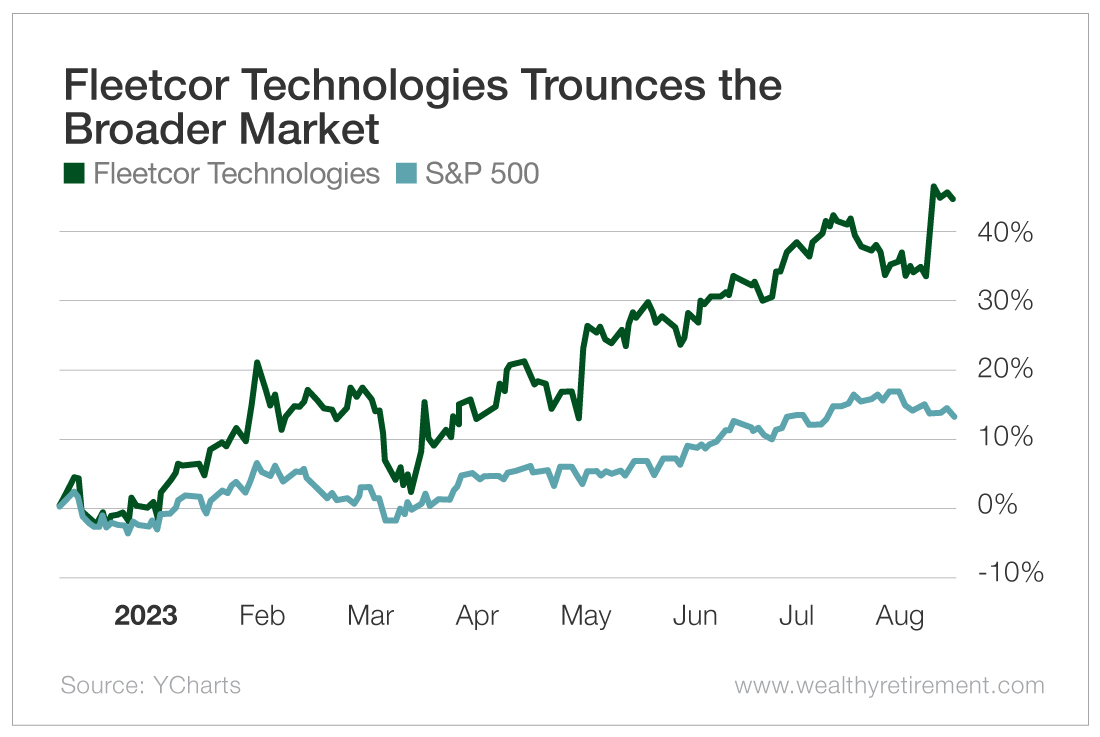

Since then, Fleetcor’s share worth has risen 44%, which is greater than triple the 13% enhance within the S&P 500.

A 44% share worth enhance is a really good return over three years…

With Fleetcor, we noticed an enormous soar in simply over eight months!

A transfer this quick begs the query of whether or not Fleetcor’s valuation has elevated as rapidly as its inventory worth.

Fleetcor’s “Barely Undervalued” score might have to be revised…

Final December, the inventory was buying and selling at 15 instances trailing earnings.

That was a really engaging valuation level for an organization with a protracted observe document of rising earnings at an annualized price of 10% to fifteen%.

With the sharp rise in Fleetcor’s buying and selling worth, the price-to-earnings ratio for the inventory is now greater than 21.

Whereas I don’t suppose that’s costly for an organization with Fleetcor’s observe document, I do suppose it’s a very reasonable valuation.

The large high quality of this firm hasn’t modified since final December, however the attractiveness of the share worth clearly has.

I’m revising my Worth Meter score of Fleetcor Applied sciences shares from “Barely Undervalued” to “Appropriately Valued.”

Relaxation assured, I’ll be keeping track of this long-term development inventory for an additional likelihood to amass it at a greater worth.

Our 44% return in eight months was an incredible success, and I’d like to do it once more!

When you have a inventory that you simply’d prefer to have rated by The Worth Meter, go away the ticker image within the feedback part beneath.

{kind=link}