This text will show you how to lower your expenses and keep away from regrets when shopping for your first residence.

Learn to financially put together for homeownership, how one can calculate what worth residence you possibly can afford, how one can navigate your approach via mortgage loans and the closing course of, and extra.

Discover out every little thing you have to learn about first-time residence shopping for so you possibly can get pleasure from your house, with out regrets, for a few years to come back.

- Are You Ready For Homeownership?

- What Type Of Credit Do You Need To Buy A Home?

- How Much Money Should You Save To Buy A Home?

- The “Are You Ready To Buy A Home” Checklist

- 4 Ways To Dramatically Reduce The Cost Of Your New Home

- How To Buy Your First Home

- Beyond Purchasing Your First Home

Are You Prepared For Homeownership?

Shopping for your first house is an thrilling enterprise, one that you simply’ll bear in mind for a lifetime.

Earlier than you soar in and begin purchasing for houses, although, it’s vital to know how the method works and how a lot cash it actually prices to buy, and personal, a house.

When you perceive how the method works and the way a lot every little thing prices, you’ll be prepared to find out when could be the most effective time so that you can purchase your first residence.

On this part, we’ll show you how to decide whether or not you’re financially able to buy a house by guiding you thru the next questions:

- Why do I wish to purchase a house?

- Am I financially ready to purchase a house?

- What are the hidden bills of homeownership?

- What’s the full checklist of bills concerned in shopping for a house?

- Is my credit standing sturdy sufficient to purchase a house?

You’ll additionally uncover tips about how one can funds and save to your first residence, so that you’re 100% prepared when the time comes.

Why Do You Need To Purchase A Dwelling?

Many individuals purchase a house as a result of they assume it’s the “regular” factor to do. They see their mates shopping for houses, and plenty of occasions — merely wish to sustain with the gang.

Buying a house is a severe monetary step, and when you’re not prepared for it, you shouldn’t be swayed by peer stress or the necessity to match into “regular.”

A survey printed by Highland Solutions towards the tip of 2020 revealed some fascinating details about immediately’s “regular” funds:

- The vast majority of individuals (63%) have been residing paycheck-to-paycheck for the reason that spring of 2020.

- The vast majority of individuals (67%) remorse not having saved more cash previous to 2020.

- The overwhelming majority (82%) of individuals say they couldn’t afford a $500 emergency in the event that they encountered one.

- Practically half of the individuals surveyed (44%) say they had been already residing past their means earlier than the pandemic hit.

When you’re excited about shopping for a house as a result of it’s the “regular” factor to do, or as a result of nearly all of your mates are doing it, it’s best to rethink.

The majority of millennials (individuals ages 25-40) owners remorse their residence shopping for selections, in keeping with a 2021 survey by Bankrate.

Of the 64% of millennials that remorse their home-buying choices, 68% of them cite monetary causes for his or her regret, together with:

- Excessive upkeep and homeowner-related prices (21%)

- Not pleased with their mortgage charge (12%)

- Mortgage fee is simply too excessive (13%)

- Really feel they paid an excessive amount of for his or her residence (13%)

- Say their residence was not funding (9%)

The excellent news is that each one of those monetary regrets will be averted by understanding the prices and course of upfront.

Regular individuals find yourself broke.

Regular millennials have regrets after buying their houses.

The vast majority of individuals find yourself broke, careworn, and remorseful on the subject of their funds and their houses.

As a substitute of trying to the bulk to your thought of “regular,” assume just like the minority.

The minority of individuals will analysis home-buying prices, processes, and home-owner bills earlier than they decide when and what to buy.

The minority of individuals would possibly wait a bit longer to purchase their first residence, however after they do, they’ll know their funds can deal with it.

The minority will transfer ahead with the boldness that they will afford their residence as a result of they’ve taken the time to teach themselves in regards to the course of and bills earlier than leaping in.

Are You Financially Ready To Purchase A Dwelling?

On this part, we’ll present you navigate and financially put together to your first residence buy by answering questions equivalent to:

- How a lot does it price to purchase a house?

- How will you put together for the hidden prices of homeownership?

- How a lot mortgage are you able to afford?

- How a lot cash must you save before you purchase a house?

- How will you slash the worth of your house?

- What kind of credit score do you have to purchase a house?

How A lot Does It Value To Purchase A Dwelling?

It’s straightforward to underestimate the prices concerned in buying a house as a result of there are a number of you hardly ever hear about.

Along with a downpayment, you’ll additionally must be ready to pay closing prices, reserves, insurance coverage and taxes, and survey-appraisal-inspection charges.

Let’s check out every of those prices and discover out how one can put together for them.

Downpayment: 20% Of Buy Worth

The downpayment is the amount of money you set down on your house and isn’t coated by your mortgage mortgage.

For many individuals, saving for the downpayment on a house is the hardest monetary problem of the whole course of.

Your mortgage lender most likely gained’t require a 20% downpayment. Actually, many solely require 2-3% of the acquisition worth.

Your banker will most likely soar via hoops to get you in with the bottom down fee doable — as a result of they earn more money (and commissions) while you save much less and borrow extra.

For instance, when you’re buying a $200,000 residence and also you make a 3% down fee of $6,000 as a substitute of a 20% downpayment of $40,000, your lender pockets an additional $18,000 over the lifetime of your mortgage.

Placing lower than 20% down on a house is a expensive mistake that will trigger you to remorse your buy for a few years.

Whenever you put lower than 20% down on a house, right here’s what occurs:

- It’s important to pay to your banker’s non-public mortgage insurance coverage (PMI), which prices between .5% – 2% of the acquisition worth yearly. PMI is insurance coverage that covers your banker when you default on the mortgage, nevertheless it has no advantages to you, the borrower.

For instance, you’d pay about $285 monthly additional (along with your common mortgage fee) for personal mortgage insurance coverage on an average-priced ($285,000) residence.You’ll pay to your banker’s PMI till you might have a minimum of 20% fairness in your house, at which level you possibly can request to get it dropped. By legislation, the lender isn’t required to drop your PMI till you’ve received 22% fairness in your house.

Fairness is your mortgage quantity vs what the house is definitely value. So, when you purchase a house for $200,000, and you have to take out a $150,000 mortgage mortgage, meaning you’ll have $50,000 fairness in your house. Even while you attain the required fairness, getting the PMI eliminated out of your mortgage could be a problem that requires paperwork, a brand new appraisal, and infrequently months of ready.

- It’s important to borrow more cash to buy your house, which might find yourself being A LOT dearer than you may think.For instance, when you purchase a $200,000 residence with a 2% downpayment ($4,000) as a substitute of a 20% downpayment ($40,000) on a 30-year mortgage, that residence will find yourself costing you about $400,000 over the lifetime of your mortgage.Curiosity, charges, and shutting prices are all greater while you skimp on the down fee

For individuals who assume just like the minority, a 20% downpayment presents a possibility to save lots of a small fortune when buying a house. Not solely are you able to skip the PMI prices, however you’ll additionally save 1000’s on curiosity over time.

Closing Prices: 1.5% – 2.5% Of Whole Buy Worth

Whenever you signal to your mortgage mortgage, there are further prices and costs that aren’t coated by your down fee. These closing prices, that are often break up between you and the vendor, add to the whole of 2% – 5% of the acquisition worth of your house. Rely in your half of the closing prices totaling 1.5% – 2.5% of the acquisition worth.

Closing prices cowl issues like utility charges, title acquisition, any escrow expenses that cowl insurance coverage or property taxes, and actual property agent commissions. “Closing prices” is an umbrella time period that covers a wide range of bills in actual property transactions. The precise expenses differ by state.

Nonetheless, you can not keep away from closing prices though, as they’re a vital a part of each actual property transaction.

For instance, when you’re shopping for a $250,000 residence, you’ll most likely pay between $5,000 – $12,500 in closing prices. Many lenders provide to roll your closing prices into your mortgage mortgage, however you then’ll need to pay curiosity on these prices. When you perceive funds, you’ll attempt to pay your closing prices up entrance as a result of it’s one other glorious alternative to save cash on the whole price of your house.

Reserves: Equal To Two Mortgage Funds

Most lenders require you to have sufficient money within the financial institution (known as “reserves”) to cowl a minimum of two months (or extra) of mortgage funds.

Nonetheless, we strongly suggest that you simply don’t buy a house earlier than you financial institution a minimum of six months of residing bills.

A full financial savings account equal to 6 months of residing bills is vital to making sure that you simply don’t fall behind in your mortgage funds when you immediately lose your revenue, run up towards emergency residence repairs, or expertise another kind of economic emergency.

How A lot Does It Value To Purchase A Dwelling?

It’s straightforward to underestimate the prices concerned in buying a house as a result of there are a number of you hardly ever hear about.

Along with a downpayment, you’ll additionally must be ready to pay closing prices, reserves, insurance coverage and taxes, and survey-appraisal-inspection charges.

Let’s check out every of those prices and discover out how one can put together for them.

Downpayment: 20% Of Buy Worth

The downpayment is the amount of money you set down on your house and isn’t coated by your mortgage mortgage.

For many individuals, saving for the downpayment on a house is the hardest monetary problem of the whole course of.

Your mortgage lender most likely gained’t require a 20% downpayment. Actually, many solely require 2-3% of the acquisition worth.

Your banker will most likely soar via hoops to get you in with the bottom down fee doable — as a result of they earn more money (and commissions) while you save much less and borrow extra.

For instance, when you’re buying a $200,000 residence and also you make a 3% down fee of $6,000 as a substitute of a 20% downpayment of $40,000, your lender pockets an additional $18,000 over the lifetime of your mortgage.

Placing lower than 20% down on a house is a expensive mistake that will trigger you to remorse your buy for a few years.

Whenever you put lower than 20% down on a house, right here’s what occurs:

- It’s important to pay to your banker’s non-public mortgage insurance coverage (PMI), which prices between .5% – 2% of the acquisition worth yearly. PMI is insurance coverage that covers your banker when you default on the mortgage, nevertheless it has no advantages to you, the borrower.

For instance, you’d pay about $285 monthly additional (along with your common mortgage fee) for personal mortgage insurance coverage on an average-priced ($285,000) residence.You’ll pay to your banker’s PMI till you might have a minimum of 20% fairness in your house, at which level you possibly can request to get it dropped. By legislation, the lender isn’t required to drop your PMI till you’ve received 22% fairness in your house.

Fairness is your mortgage quantity vs what the house is definitely value. So, when you purchase a house for $200,000, and you have to take out a $150,000 mortgage mortgage, meaning you’ll have $50,000 fairness in your house. Even while you attain the required fairness, getting the PMI eliminated out of your mortgage could be a problem that requires paperwork, a brand new appraisal, and infrequently months of ready.

- It’s important to borrow more cash to buy your house, which might find yourself being A LOT dearer than you may think.For instance, when you purchase a $200,000 residence with a 2% downpayment ($4,000) as a substitute of a 20% downpayment ($40,000) on a 30-year mortgage, that residence will find yourself costing you about $400,000 over the lifetime of your mortgage.Curiosity, charges, and shutting prices are all greater while you skimp on the down fee

For individuals who assume just like the minority, a 20% downpayment presents a possibility to save lots of a small fortune when buying a house. Not solely are you able to skip the PMI prices, however you’ll additionally save 1000’s on curiosity over time.

Closing Prices: 1.5% – 2.5% Of Whole Buy Worth

Whenever you signal to your mortgage mortgage, there are further prices and costs that aren’t coated by your down fee. These closing prices, that are often break up between you and the vendor, add to the whole of 2% – 5% of the acquisition worth of your house. Rely in your half of the closing prices totaling 1.5% – 2.5% of the acquisition worth.

Closing prices cowl issues like utility charges, title acquisition, any escrow expenses that cowl insurance coverage or property taxes, and actual property agent commissions. “Closing prices” is an umbrella time period that covers a wide range of bills in actual property transactions. The precise expenses differ by state.

Nonetheless, you can not keep away from closing prices though, as they’re a vital a part of each actual property transaction.

For instance, when you’re shopping for a $250,000 residence, you’ll most likely pay between $5,000 – $12,500 in closing prices. Many lenders provide to roll your closing prices into your mortgage mortgage, however you then’ll need to pay curiosity on these prices. When you perceive funds, you’ll attempt to pay your closing prices up entrance as a result of it’s one other glorious alternative to save cash on the whole price of your house.

Reserves: Equal To Two Mortgage Funds

Most lenders require you to have sufficient money within the financial institution (known as “reserves”) to cowl a minimum of two months (or extra) of mortgage funds.

Nonetheless, we strongly suggest that you simply don’t buy a house earlier than you financial institution a minimum of six months of residing bills.

A full financial savings account equal to 6 months of residing bills is vital to making sure that you simply don’t fall behind in your mortgage funds when you immediately lose your revenue, run up towards emergency residence repairs, or expertise another kind of economic emergency.

Owners Insurance coverage and Property Taxes: Varies

Most month-to-month mortgage premiums will embody property taxes and residential insurance coverage.

Nonetheless, your banker could require you to pay for one 12 months’s value of property taxes and owners insurance coverage and presumably six month’s of property taxes — upfront (on the time of closing). Your lender then deposits this tax and insurance coverage cash into an escrow account and pays it in your behalf when due.

- Owners insurance coverage is necessary when you’re paying to your residence with a mortgage. It prices a mean of $1,200 per 12 months and helps be certain that you gained’t lose cash or your house to occasions equivalent to fireplace, lightning, or vandalism. The value of householders insurance coverage varies relying on the coverage you select and the worth of your house and property.

- Property taxes are taxes you pay on your house and property and are usually paid on a once-or-twice per 12 months schedule. How a lot you pay for property taxes depends upon the worth of your property and your native tax charges.The average U.S. homeowner pays about $2,375 per 12 months in property taxes, nonetheless, in some states the charges are twice as excessive.

Survey, Appraisal, And Inspection Charges: $600 – $2000

You’ll most definitely pay out about $300 – $1500 in survey and appraisal charges (relying on the worth of your house) and one other $300 – $500 for personal residence inspection charges when buying a house.

These charges differ relying on what state you reside in and what kind of inspections you request.

- A property survey verifies the boundary traces and authorized description of the property your home sits on. In some circumstances, a property survey will not be required (relying on the place you reside and what lender you employ). Nonetheless, a property survey is an important step in residence shopping for and one you shouldn’t skip even when you’re not legally required. Getting a transparent understanding of your property traces is vital to know the place you and your surrounding neighbors can and might’t construct, backyard, fence, or pave.Property surveys price a mean of $400 – $700, nonetheless, chances are you’ll pay extra for bigger properties or sure terrains or places.

- A home appraisal is when an unbiased, skilled appraiser evaluates the house you’re about to purchase, considering:Whenever you put in a bid on a house and are available to a worth settlement with the vendor, you then need to get the house’s value evaluated by knowledgeable, unbiased appraiser. This step protects the lender for the reason that residence serves as collateral for the mortgage.Appraisers work for the lender, however you reimburse them for the charge (often $300 – $400) as a part of the closing prices.Appraisers take the next into consideration when figuring out the worth of your house:

- Location

- Sq. footage

- Situation

- Additions and renovations

- Actual property worth of the neighborhood

If the appraiser evaluates your house for lower than the promoting worth, your lender won’t cowl the overage within the mortgage mortgage. For instance, when you and the vendor agree on a worth of $200,000, however the appraisal evaluates its value at $190,000, your financial institution will solely provide you with a mortgage for $190,000.On this case, you possibly can renegotiate with the vendor, pull the provide and get your cash returned, pay for the distinction in money, or problem the appraisal.

- A house inspection usually prices between $300 and $1,000, and it ensures that you simply get what you assume you’re paying for. Whenever you put a suggestion in on a house, it’s smart to barter a 7-day contingency that permits you to rent a personal inspector who will decide whether or not there are any issues with the house.

For instance, chances are you’ll not notice that your house is liable to flooding, and find yourself paying $20,000 in repairs solely months after you progress in.Even newly-built houses can have issues equivalent to holes within the roof, improperly put in flooring and staircases, or poor building that makes the house unsafe.

Remember that simply because the house seems good and downside free on the floor, there may be some main points occurring beneath the ground or behind the partitions.

Solely knowledgeable inspector can examine these areas and present you what’s actually occurring.With an inspection contingency, you possibly can uncover issues before you purchase and work the worth of repairs into your negotiations.

Rent your individual property inspector, as a substitute of taking the referral your actual property agent offers you. An agent’s aim is to shut on the house, which is a battle of curiosity for the client who desires to completely examine it first.To discover a official residence inspector (there are various scammers), try organizations such because the American Society of Home Inspectors, International Association of Certified Home Inspectors, or the National Academy of Building Inspection Engineers.

Whenever you buy a house, you have to be ready to pay for greater than the down fee. Along with a downpayment, you’ll additionally must pay closing prices, reserves, taxes and owners insurance coverage, and survey/appraisal/inspection charges.

How A lot Does It Value To Personal A Dwelling?

Have you ever ever thought, “Hmm, I’m paying $1,000 in month-to-month lease — at that worth, I may very well be making month-to-month mortgage funds alone residence as a substitute!”?

That line of pondering can get individuals in deep monetary hassle, since proudly owning a house entails a lot greater than month-to-month mortgage funds.

Owners’ insurance coverage, property taxes, upkeep, utilities, affiliation charges, and seasonal providers all contribute to the general worth of proudly owning a house.

When you’re not ready for the extra prices and don’t funds for them upfront, you would possibly uncover that proudly owning a house is hardly the perfect you dreamed of.

64% of millennials say they’ve home-buying regrets,and 21% of these say excessive upkeep charges and homeownership prices are the rationale for his or her regret.

On this part, we check out among the prices related to proudly owning a house, so you possibly can put together forward of time and keep away from regrets.

Mortgage Funds, House owner Insurance coverage, And Property Taxes

Dwelling mortgage, insurance coverage, and taxes are sometimes lumped into one class as a result of they’re usually mixed into one month-to-month fee (particularly through the first few years).

Typically, you’ll make one month-to-month fee (that features mortgage, insurance coverage, and taxes) to an escrow firm that can flip round and make particular person funds for you. This makes it simpler on you when writing out the payments every month, and likewise satisfies your lender, who wants a assure that your insurance coverage and taxes are paid on time.

Mortgage funds are the worth you negotiate together with your lender while you take out the mortgage mortgage.

Mortgage funds embody:

- Principal: the amount of cash you borrowed from the lender

- Curiosity: the price of your mortgage, primarily based on a share quantity of your mortgage

Each greenback you fiscal via the financial institution is a greenback it’s important to pay curiosity on, and the curiosity in your mortgage mortgage at all times prices greater than it appears.

For instance, when you solely put a 2% downpayment on your house, you possibly can find yourself paying $200,000 in curiosity on a $200,000 residence with a 30-year mounted mortgage.

That’s why monetary preparation is vital when buying a house. To cut back the general price (curiosity) of your mortgage:

- Make a downpayment of a minimum of 20%.

- Construct a excessive credit score rating so you will get decrease rates of interest.

- Pay greater than the required minimal mortgage funds. The faster you repay your mortgage mortgage, the much less it prices you in curiosity.

Owners insurance coverage is a type of insurance coverage that protects your house and property, together with your home equipment and possessions, and likewise protects you from lawsuits if somebody will get damage in your property.

If somebody or one thing damages your house, property, or possessions, owners insurance coverage is the one option to get better your monetary loss.

Owners insurance coverage isn’t required by legislation.

Nonetheless, when you take out a mortgage mortgage, your lender would require you to have owners insurance coverage.

No matter price or necessities, all owners want home-owner insurance coverage coverage. With out it, if a storm or fireplace destroys your house, you can find yourself homeless whereas nonetheless owing a whole lot of 1000’s of {dollars} in your mortgage mortgage.

If you’re shopping for a house or already personal one, insurance coverage is a should — whether or not or not it’s required by a lender or the legislation.

Do you know? Practically 50% of People stay in earthquake-prone areas and 90% of People stay in areas thought-about “seismically lively.”

When buying a owners insurance coverage coverage, it’s best to take out sufficient insurance coverage to cowl the price of rebuilding your house, in case a hearth or storm destroys it.

The typical U.S. owners insurance coverage coverage is about $1,200 per 12 months, however don’t depend on yours being that low.

There are a number of elements that may improve or lower the price of your insurance coverage, together with:

- The place you reside: For instance, Oklahoma owners pay a mean $4,445 per 12 months, whereas Vermont residents pay solely $600 – $650.

- What measurement deductible you set

- What number of reductions you possibly can declare

- The placement and age of your house

- Whether or not you have to add further protection to guard towards conditions that aren’t coated in typical insurance policies, equivalent to earthquake, flooding, or sewage backup. When you personal high-priced art work, jewellery, or different possessions, you might also want further protection.

The price of owners insurance coverage can differ by extremes relying on a number of elements, so take a pair minutes to get insurance coverage quotes or be taught the typical price in your space before you purchase a house.

Property taxes assist fund your community by paying for colleges, first responders, water, sewage, infrastructure, and extra.

Property tax prices differ from one nation to a different, and chances are you’ll even be required to pay each metropolis and county taxes, relying on the place you reside. Averages throughout the U.S. vary from .018% to 1.89% of your house’s assessed worth.

When budgeting for a house, remember that the price of property taxes and owners insurance coverage can rise over time.

| Platform | Minimal Funding | Hyperlink |

|---|---|---|

|

$10 | Signal Up |

|

$1,000 | Signal Up |

|

$25,000 | Signal Up |

Upkeep Prices

Sustaining your houses’ security and performance requires that you simply regularly spend money on repairs, upgrades, and (ultimately) renovations.

In a typical 12 months, the typical home-owner spends $9,081 on family tasks, in keeping with a report by HomeAdvisor.

Nonetheless, due partly to rising labor and provide prices, owners spent an common of $13,138 on enchancment, upkeep, and repairs in 2020.

Dwelling repairs don’t at all times occur on a predictable schedule, so that you wish to put aside some cash each month for repairs.

How a lot you have to make investments will rely upon the age and high quality of building of your house, plus the price of supplies and labor in your space.

In response to John Ghent, president-elect of the American Society of Dwelling Inspectors, right here’s how a lot it’s best to plan to spend the following on residence repairs and upkeep:

- Houses ten years and youthful: .75% of its worth yearly

- Houses ten-twenty years outdated: 1.5% of the house’s worth

- Houses twenty-thirty years outdated: 1% – 3% of the house’s worth

For instance, when you stay in a $200,000 home that’s 25 years outdated, it’s best to funds a minimum of $3,000 per 12 months on residence repairs, upgrades, and enhancements.

When that residence reaches 30 years of age, you’ll funds $6,000 per 12 months.

Nonetheless, the Homeadvisor report talked about above reveals that folks most likely spend a bit extra on their houses than Ghent recommends saving.

Utilities

When you’re used to residing in an condominium, dorm, or your dad and mom’ home, you then’ll wish to do a little bit of analysis to seek out out what utilities may cost a little for the kind of residence you’re on the lookout for.

One report, by Inspire Clean Energy, recommends that owners put aside about $275 monthly for primary utilities equivalent to:

- Electrical ($118)

- Fuel ($72)

- Water ($70)

- Trash/recycling ($14)

Remember that you’ll additionally wish to embody web and cable in your utility payments, which generally run about $50 – $300 monthly, relying on the place you reside and what bundle you select.

When you stay in an space with excessive climate (sizzling or chilly), utilities will price extra.

It’s common to obtain a $400 month-to-month invoice for electrical energy alone throughout extraordinarily chilly winters, and working air-con in excessive warmth can get almost as costly.

When you purchase a big residence, utilities will price extra.

The average size of a home within the U.S. is roughly between 2,300 – 2,500 sq. toes, and if you are going to buy a bigger residence it’s best to anticipate to pay extra for utilities.

On a 4,000 square-foot residence, the typical electrical price alone is about $200 – $300 per month in most states. Over 4,000 sq. toes, it’s best to add about $5 – $7 in electrical prices for each 100 sq. toes.

Additionally remember the fact that bigger houses carry extra hidden prices, together with (for many) landscaping, housekeeping, pool cleansing, membership memberships, safety, and extra.

House owner Or Apartment Affiliation Charges

House owner or rental affiliation charges could or will not be required, relying on whether or not your future house is a part of an affiliation.

Be warned that many home-owner and rental associations have clauses that permit them to lift the month-to-month charges when wanted.

So, what looks like an inexpensive $200 month-to-month charge while you buy the house may find yourself costing you $400 a month when you’re not cautious in regards to the contract.

As well as, if you wish to make sure upgrades or modifications to your property or residence, the affiliation should approve it first. They’re usually very particular about what you possibly can change, which might make it very troublesome to buy round and discover the most effective worth for a brand new fence or different landscaping.

The HOA could set the worth & constructing materials for a particular undertaking, so when you’re not able to tackle a sure undertaking at their worth level, chances are you’ll wish to take into account transferring to a different neighborhood with out an HOA or charge.

Nonetheless, an HOA could typically maintain some property upkeep and minor indoor repains, which may prevent cash over time. Remember to look into whether or not these conveniences are well worth the price ticket earlier than you progress into an HOA neighborhood.

Seasonal Companies

Landscaping, snow removing, pool charges, and home cleansing prices may issue into your house bills.

When you stay in an HOA neighborhood, a few of these providers could also be coated. Nonetheless, you’ll need to cowl these bills your self when you stay in a conventional neighborhood.

How A lot Cash Ought to You Spend On A Dwelling?

13% of millennials with home-owner regrets say their mortgage funds are too excessive.

How are you aware how a lot to spend on a house so that you simply don’t remorse your mortgage funds later?

Keep in mind, your house prices cash to purchase and keep:

- Closing prices + curiosity on closing prices when you fold them into the mortgage mortgage

- Your mortgage mortgage + curiosity in your mortgage mortgage

- Non-public mortgage insurance coverage (in case your down fee is lower than $20,000)

- Dwelling insurance coverage

- Property taxes

- Upkeep, repairs, and enhancements

- Utilities

Many private finance consultants suggest holding your mortgage funds to not more than one-third of your gross revenue, however we at Minority Mindset assume that’s a recipe for catastrophe.

Month-to-month Mortgage Funds Ought to Not Exceed 27% Of Your Web Revenue

To make sure you can maintain management of your different month-to-month bills, we suggest not permitting your mortgage funds to exceed 27% of your month-to-month web revenue.

For instance, when you and your partner every take residence $3,000 monthly (whole of $6,000 monthly), you’ll restrict your month-to-month mortgage funds to not more than $1,500 monthly.

And, in case you have kids in your future and one father or mother will keep residence for a couple of years, you should definitely funds primarily based on one particular person’s revenue, not two.

To make sure you can afford your mortgage funds, together with all the opposite prices of homeownership, maintain your month-to-month mortgage funds to lower than 27% of your month-to-month take-home pay.

How To Allocate Your Revenue As A House owner

By planning your home-owner funds earlier than you start purchasing, you’ll save your self quite a lot of stress and nervousness.

Planning forward will show you how to make a greater determination on which residence to purchase, and permit you to benefit from the course of of shopping for your first residence.

Minority Mindset recommends allocating your home-owner funds with the 75/25 methodology:

- 75% of your web revenue towards spending

- 25% of your web revenue towards investing.

If for some purpose, you don’t have a full six months of residing bills in your emergency financial savings account, then the 75/25 allocation would change to 75/15/10:

- 75% of your web revenue towards spending

- 15% of your web towards financial savings

- 10% of your web revenue towards investing

The spending class is the place the majority of your revenue goes, and also you wish to just be sure you don’t permit it to exceed 75% of your web revenue.

Remember to embody the next within the spending portion of your budgeting:

- Meals

- Garments

- Utilities

- Month-to-month mortgage funds

- All insurances: well being, automotive, owners, pet

- All medical bills, together with prescriptions

- Debt funds (equivalent to loans and bank cards)

- Snow removing and garden care

- Trash pickup

- Dwelling upkeep and repairs

- Leisure

Investing is an important a part of any month-to-month funds, so that you additionally wish to make certain that you possibly can afford to allocate 25% of your revenue towards investing every month.

By allocating your revenue with the 75/25 methodology, you possibly can plan for a financially steady future that helps you easily handle the bills associated to proudly owning a house.

What Kind Of Credit score Do You Want To Purchase A Dwelling?

Credit score scores in 2021 are extra vital than ever earlier than.

Right this moment, your credit score scores are checked for nearly every little thing, together with fundamentals equivalent to rental flats, employment, cellphone plans, and insurance coverage charges.

How Credit score Scores Have an effect on Dwelling Shopping for

Not solely do you want a sure credit standing to qualify for a mortgage mortgage, however the power of your credit score can even have an effect on the price of your mortgage mortgage and owners insurance coverage coverage.

You would possibly qualify for a mortgage mortgage in case you have poor credit score, nonetheless, your mortgage funds can be a lot greater than somebody with good credit score.

For instance, in case you have low credit score and find yourself with a 4.5% rate of interest on a $300,000, 30-year mortgage mortgage, you pay $173 extra every month than somebody with good credit score who will get a 3.5% rate of interest.

Over time, the prices of poor credit score are almost unimaginable.

For the $300,000 residence with the upper 4.5% rate of interest, you find yourself paying $62,252 extra (over the lifetime of your mortgage) to your residence than somebody with a 3.5% rate of interest.

- Within the instance above, the home-owner pays $173 extra every month for a complete of $62,252 extra over the lifetime of their mortgage — as a consequence of poor credit score.

Earlier than you take into account buying a house, it might be value your effort and time to strengthen your credit standing earlier than making use of for a mortgage mortgage.

You’ll be able to often enhance your credit score inside 5 – 6 months, but when it takes longer, it’s well worth the wait. you’ll save an excessive amount of cash in your month-to-month mortgage funds and the general price of your house mortgage.

How Do Credit score Rankings Work?

Most banking establishments use the FICO credit score system to charge your credit score.

FICO assigns a 3-digit quantity to signify how trustable they assume you might be on the subject of borrowing cash and paying your payments on time.

Right here’s what FICO scores signify:

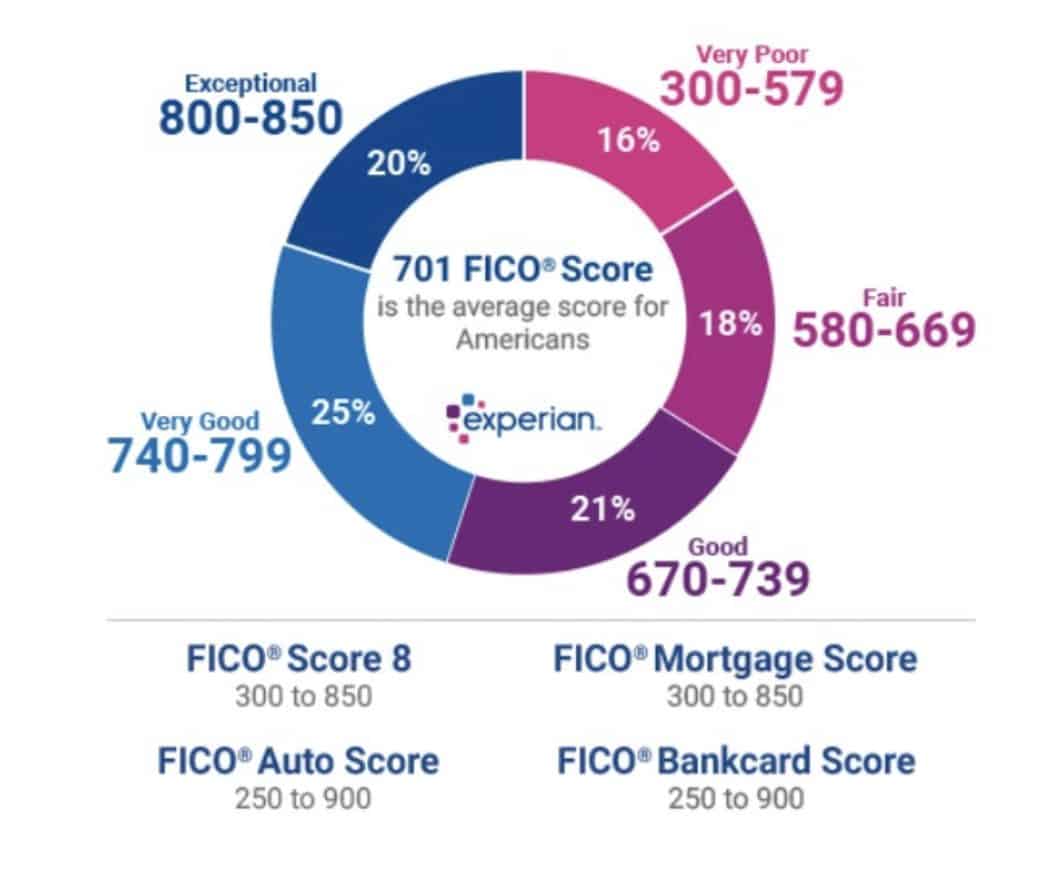

In response to a report by Experian, right here’s what your FICO rating means:

- 300 – 579 FICO rating: Very Poor, you most likely gained’t get accepted for any kind of credit score.16% of People fall into the “Very Poor” credit score class.

- 580 – 669 FICO rating: Honest, you’re thought-about a “subprime” borrower — if you will get accepted for any credit score, your rates of interest can be very excessive. 18% of People fall into the “Honest” class.

- 670 – 739 FICO rating: Good, lenders take into account you “trustable” and also you’re more likely to get common rates of interest on credit score. Solely 8% of individuals with “good” credit score scores fall significantly behind on funds.

- 740 – 799 FICO rating: Very Good, you’ll get pleasure from decrease rates of interest on loans and qualify for higher bank cards.

- 800 – 850 FICO rating: Distinctive, you’ve reached the highest credit score tier and are granted the bottom rates of interest. You’re more likely to get accepted in most credit score conditions.

To find out your credit score rating, FICO makes use of 5 separate standards.

To find out your credit score rating, FICO makes use of 5 separate standards.

1. Cost historical past: 35%

Cost historical past is a big consider figuring out your credit standing, because it accounts for 35% of your credit score rating.

One or two late funds could not destroy your credit score when you usually pay on time. Nonetheless, in case you have a historical past of late or non-payment, you’ll have a troublesome time constructing credit score rating.

An ideal fee historical past will assist to lift your credit score rating, nonetheless, it gained’t provide you with an ideal credit score rating.

The amount of cash you owe, size of your credit score historical past, quantity of recent credit score you’ve utilized for or obtained, and the mix of credit sorts you employ are additionally figuring out elements of your FICO rating.

The forms of credit score that issue into your rating embody:

- Bank cards and retail credit score

- Installment loans

- Any finance firm accounts

- Mortgage loans

- Public information and assortment objects

2. How a lot cash you presently owe: 30%

How a lot you presently owe to collectors accounts for 30% of your FICO credit score rating.

Owing cash could be a optimistic, however when you’re utilizing most of your obtainable credit score or in any other case give the impression that you simply’re financially overextended, chances are you’ll get pegged as an at-risk borrower.

3. Size of your credit score historical past: 15%

The size of your credit score historical past accounts for 15% of your credit score rating.

A long credit history isn’t required for rating, however it will possibly assist.

Fico scores take into account the next when figuring out your rating:

- The age of your oldest account, latest account, and common age of all accounts

- How lengthy it’s been because you used your accounts

4. New credit score: 10%

The quantity of recent credit score you’ve utilized for or obtained has a ten% affect in your credit score rating.

When you’ve opened a number of new accounts in a short while interval, particularly in case you have a brief credit score historical past, it will possibly get you flagged as a high-risk borrower.

5. Credit score combine: 10%

The several types of credit score you presently use play a ten% position in your credit score rating.

Having a stability of credit score sorts which might be efficiently managed (with good fee histories) can increase your credit score rating as a result of it reveals you can deal with funds.

For instance, a wholesome stability of installment accounts (equivalent to auto and pupil loans) mixed with revolving accounts (equivalent to credit score, gasoline station, and retail retailer playing cards) could assist increase your credit score rating.

In fact, the above solely improves your credit score rating in case your fee historical past with every account is nice. If yours present late or lacking funds, then it might hurt your credit score rating.

Specializing in the above 5 elements might help enhance your credit score rating.

When you’re in a position to get your rating within the “Very Good” or “Distinctive” class, you’ll get a greater rate of interest in your mortgage mortgage and save some huge cash.

A wonderful credit standing will prevent a small fortune on the general price of your house.

What Credit score Rating Do You Want To Purchase A Dwelling?

Credit score rating necessities differ by lender, however most require a minimal credit score rating of 620 to get a mortgage.

Nonetheless, it’s best to goal for a minimal 740 credit score rating before you purchase a house, so that you get a good rate of interest on the mortgage mortgage.

As a substitute of speeding into homebuying, we suggest you are taking the time to enhance your credit score rating till it reaches a minimum of 740.

How To Enhance Your Credit score Rating For Dwelling Shopping for

You probably have very poor or no credit score, listed here are 9 suggestions that can assist you begin constructing a greater credit score rating:

- Repay all of your debt. You probably have quite a lot of debt, take into account choosing up additional work to assist pay it off extra rapidly.

- Use bank cards responsibly, paying off the stability in full on the finish of every month.

- Hold all of your funds and payments present — at all times.

- Apply for brand spanking new credit score solely as wanted, and don’t apply for a number of new accounts without delay.

- Don’t shut any bank card accounts until they’re costing you cash, as a result of a number of accounts might help increase your credit standing.

- Check your credit reports for errors and work to get them eliminated.

- Use secured loans, secured bank cards, and different credit score builders equivalent to passbook loans, in case you have no credit score in any respect.

- Take a look at non-profit lending circles to acquire loans that may strengthen your credit score rating. For instance, the Mission Asset Fund affords inexpensive loans that may assist construct your credit standing.

- Get credit score to your on-time utility, cellphone, and rental funds via providers equivalent to Experian Boost and Rental Kharma.

You’ll be able to most likely enhance your credit standing inside 5 – 6 months, nonetheless, if it takes longer, it’s effectively well worth the time. A great credit standing improves the standard of your monetary life in a number of methods, together with reducing your mortgage prices.

How A lot Cash Ought to You Save To Purchase A Dwelling?

Earlier than you start purchasing for a house, examine that your funds are so as and that you simply’ve received sufficient cash saved as much as put together for homeownership

1. Emergency Financial savings Account: Equal To Six Months Of Dwelling Bills

The primary monetary step towards homebuying is to make sure that you’ve received a full emergency financial savings account, equal to 6 months of residing bills, within the financial institution.

Sudden life occasions are regular, and so they occur to everybody sooner or later.

You could possibly immediately lose your revenue, incur hefty medical bills, or have to exchange or restore your automotive.

Monetary emergencies usually require fast money, which is why a financial institution is the most effective place to retailer your financial savings account.

A financial savings account doesn’t ask questions when you have to withdraw cash, and gained’t cost you charges or penalties for early removing, the way in which that many investments do.

Constructing an emergency financial savings account equal to 6 months of residing bills will assist make sure you towards most of life’s monetary emergencies.

It’s going to additionally almost assure you can make your mortgage, owners insurance coverage, and property tax funds on time so that you simply don’t need to worry dropping your house as a consequence of an surprising life occasion.

Your month-to-month bills as a home-owner can be greater than what you’re most likely used to. You’ll wish to base your financial savings requirement in your month-to-month funds as a home-owner

Homeownership requires you to put aside cash every month for repairs and upkeep, greater utility payments, landscaping, and different home-owner prices.

When calculating how a lot you have to save, determine six months of residing bills in your new residence — not six months of bills on the scaled-back funds you’re most likely residing on proper now.

A full emergency financial savings account will assist shield you and your loved ones from any monetary disaster that would threaten the well-being of your house and household.

2. Dwelling Shopping for Prices: 2% – 5% Of Buy Worth

Along with a full emergency financial savings account, you additionally wish to save up sufficient cash to cowl your closing prices so that you don’t need to fold them into your mortgage mortgage.

Piling your closing prices into your mortgage mortgage implies that your month-to-month funds can be greater and also you’ll pay extra for the mortgage itself.

- Right here’s a fast recap of the bills you’ll want while you purchase your house:

- Down fee: 20% of buy worth

- Closing Prices: 1.5% – 2.5% Of Whole Buy Worth

- Reserves: Equal To Two Mortgage Funds (you should utilize your emergency financial savings for this)

- Further Bills (survey, appraisal, and inspection charges): $600 – $2000

- Dwelling insurance coverage and property taxes: Equal to 6 months of taxes and insurance coverage

Earlier than you start purchasing for houses, just be sure you have an emergency financial savings account equal to 6 months of (home-owner) residing bills, plus the estimated closing prices, saved and sitting in your financial institution.

The “Are You Prepared To Purchase A Dwelling” Guidelines

Sixty-four % of millennials remorse their residence shopping for selections, and we wish to just be sure you don’t fall into that class.

This guidelines will show you how to keep away from the issues that trigger most millennials to remorse their choices.

_____ Are you conscious of the prices concerned in buying a house?

Shopping for a house prices cash, together with a downpayment, curiosity on the mortgage mortgage, and shutting prices.

_____ Do you come up with the money for saved?

_____ Do you might have six months of home-owner residing bills in your financial savings

Account?

_____ Do you might have a 20% money down fee saved?

_____ Do you come up with the money for saved to cowl closing prices?

_____ Are you able to afford the brand new month-to-month mortgage funds?

_____ Are your mortgage funds lower than 25% of your web month-to-month revenue?

_____ Does your whole month-to-month spending funds (together with mortgage and home-owner

bills) price lower than 75% of your month-to-month web revenue?

_____ Do you take into account your house an funding?

A house isn’t an funding. When you consider your house as an funding, you’ll seemingly be dissatisfied. There’s no assure that it is possible for you to to promote it for a revenue — and even at market worth. You’ll put time, power, and cash into it over time. Proudly owning a house rewards you with numerous advantages, nonetheless, it shouldn’t be thought-about an funding.

_____ Have you learnt what measurement home you need?

Be clear in your sq. footage minimal and most before you purchase, so that you don’t have regrets in regards to the measurement of your house.

_____ Have you ever selected the most effective location for your loved ones?

Be clear in your location targets so that you simply don’t get emotionally persuaded into compromising on the place you wish to stay. You’ll be able to repair up, develop, renovate, and personalize many facets of a home, however its location won’t ever change — be sure to find it irresistible!

_____ Have you ever shopped round to seek out the most effective rates of interest and lenders?

Relating to rates of interest, even a small fraction of a % can hit your pocketbook arduous. Remember to evaluate charges on a website like Credible earlier than selecting a lender!

4 Methods To Dramatically Scale back The Value Of Your New Dwelling

To this point on this information, we’ve coated quite a lot of details about how costly it may be to purchase a house.

On this part, we do the other. We’ll present you 4 methods to drastically scale back the worth of your house, which might go a great distance towards masking a few of your house shopping for and homeownership bills.

1. Discover The Greatest Potential Curiosity Charge For Your Mortgage Mortgage

Evaluating rates of interest before you purchase a house can prevent a whole lot each month, including as much as tens of 1000’s over the time period of your mortgage.

For instance, when you’re shopping for a $300,000 residence on a 30-year mounted mortgage, and also you stick with the usual fee plan:

- A 4.5% rate of interest means you’ll pay about $1,520/month mortgage funds and a complete of about $547,220 to your residence.

- A 3.5% rate of interest means you pay about $1,347/month mortgage funds and a complete price of $484,968 to your residence.

On this instance, a one % distinction in curiosity equals greater than $60,000 over the lifetime of your mortgage.

Comparability websites equivalent to Credible permit you to view present rates of interest with the intention to select the lender with the bottom charges.

As a part of your mortgage negotiations, ask the lender for a mortgage with no prepayment penalties and request a no-fee financing deal. These agreements permit you to repay your house earlier with out penalties and to additionally reduce down closing prices.

2. Keep away from Non-public Mortgage Insurance coverage Charges

When you make a downpayment of lower than 20% in your future residence, you’ll seemingly get hit with PMI charges, which often price between .5% – 2% of the whole worth of your house.

Keep away from the extra PMI charges by saving a 20% downpayment earlier than you start purchasing for a house.

3. Negotiate A 7-day Contingency

When negotiating the worth of a house with the vendor, ask for a 7-day contingency as a part of the deal.

The 7-day contingency permits you to again out of the deal, for any purpose, inside 7 days.

- Rent a personal property inspector to instantly examine the house for vital points that may price you cash to repair. In the event that they discover any, you possibly can again out of the deal or work the price of repairs into your negotiations.

Negotiating a 7-day contingency is important to thorough monetary planning as a result of it will possibly show you how to keep away from emergency repairs that will price 1000’s of {dollars} throughout your first 12 months of homeownership.

4. Make Bi-weekly Mortgage Funds

As a substitute of creating one month-to-month mortgage fee, take into account splitting the price in half and making a half fee each different week.

This helps you make a couple of additional funds annually, and the savings over time is spectacular.

For instance, in case your common month-to-month mortgage fee is $764, pay $382 each different week as a substitute.

For a $160,000 mortgage with 4% curiosity on a 30-year mounted mortgage, this technique will prevent $18,703 over the lifetime of your mortgage, AND you’ll pay it off two and half years early.

With a little bit understanding of how residence shopping for works, it can save you fairly a bit of cash when buying a brand new residence.

To cut back your prices, discover the most effective rates of interest, keep away from non-public mortgage insurance coverage charges, negotiate a 7-day contingency, and make biweekly mortgage funds.

How To Purchase Your First Dwelling

Whenever you’ve saved and budgeted every little thing vital to buy your first residence, listed here are the steps you’ll take to purchase it:

- Set your funds.

- Prepare to buy.

- Discover a lender and get pre accepted.

- Store to your new residence.

- Make a suggestion — understanding “escrow”

- Full the closing course of.

Step One: Set Your Funds

When you perceive the whole prices of buying and proudly owning a house (outlined within the sections above), you’re prepared to start budgeting for a house.

Pre-purchase Concerns For Shopping for A Dwelling

Earlier than you take into account buying a house, you wish to have the next monetary factors so as:

- 20% of the acquisition worth of your house saved for the down fee

- Six months of residing bills put aside for emergency financial savings

- Credit score rating of fine or (ideally) excellent

When you might have the fundamentals in place, you’re prepared to think about whether or not you’re ready for the month-to-month prices and buy prices concerned in shopping for and proudly owning a house.

Buy Prices Associated to Shopping for A Dwelling

When individuals store for houses, they usually concentrate on the general buy worth and what their common month-to-month mortgage funds will add as much as.

In all the joy, it’s straightforward to overlook that there are vital buy prices concerned when buying a house, a lot of which aren’t coated by the mortgage mortgage.

Hold the next purchase-related bills in thoughts when budgeting to purchase a house:

- Closing prices (1.5% – 2.5% of whole residence buy worth), that are typically included in your mortgage mortgage. It’s higher to pay to your closing prices up entrance so that you simply don’t need to pay curiosity on them by together with them in your mortgage.

- Miscellaneous bills (about $600 – $2,000) equivalent to survey, appraisal, and inspection charges.

- One 12 months of home-owner’s insurance coverage (worth varies relying on your house and its location). This expense isn’t included in your mortgage mortgage, so you have to pay for it individually.

- Six months of property taxes, which differ by county and are due at closing.

- Monetary reserves of two or extra months (relying on lender) of mortgage funds in your account. You ought to be fantastic on this requirement if you have already got your 6-month emergency financial savings accounts in place.

Subsequent, you’ll check out your projected month-to-month bills, to plan for the additional prices you’ll incur as a home-owner.

Homeownership Bills

To make sure you can afford a house, maintain your month-to-month mortgage funds (together with owners insurance coverage and property taxes) to lower than 27% of your web revenue.

Additionally remember the fact that when you’re planning on having kids and one father or mother will keep residence with them, it’s best to funds primarily based on one revenue as a substitute of two.

Along with mortgage, insurance coverage, and tax funds, you’ll wish to embody the next bills in your projected home-owner funds:

- Mortgage funds, owners insurance coverage, and property taxes are usually lumped into one fee, particularly through the early years of your mortgage. Typically, you’ll make one month-to-month fee to an escrow firm, and so they flip round and make funds to the financial institution, insurance coverage firm, and authorities in your behalf.

- When you don’t make a down fee of a minimum of 20% on your house, you possibly can depend on paying to your banker’s non-public mortgage insurance coverage (PMI). PMI protects your financial institution must you default in your mortgage, nonetheless, it does completely nothing for you. PMI, which is often folded into your month-to-month mortgage funds (together with insurance coverage and taxes) is e-x-p-e-n-s-i-v-e. It usually prices between .5% – 2% of the whole worth of your house annually.

For instance, if you are going to buy a $285,000 residence, anticipate to pay about $285 additional (on high of your mortgage) each month. Hopefully, you save up for a downpayment of a minimum of 20% on your house so you possibly can keep away from losing a big amount of cash paying to your banker’s insurance coverage. In any other case, you’ll want to incorporate this price in your funds till you might have 20% fairness in your house.

- Upkeep prices run a mean of .75% – 3% of your house’s worth annually (relying on the age of your house).

- Utilities, which can price extra in a house than you pay in an condominium. Utilities embody electrical energy and warmth, so please you should definitely funds for excessive climate highs and lows. Air-con and warmth price far more when the climate is excessive.

- House owner or rental affiliation charges, which might rise over time.

- Seasonal providers equivalent to landscaping, snow removing, pool charges, cleansing, and different associated bills.

Shopping for a house entails three facets of budgeting: Pre-purchase preparations, buy prices, and homeownership bills.

When you’ve budgeted for homeownership and perceive how a lot residence you possibly can afford, you’re prepared to maneuver on to the pre-approval course of.

Step Two: Get Prepared To Store For A Dwelling

Earlier than you progress on to the subsequent steps of homebuying (discovering a lender and getting pre-approved), you have to be absolutely ready to start purchasing for a brand new residence instantly.

A little bit of analysis can go a great distance when purchasing for houses, so take into account the next earlier than you safe a lender.

Analysis Actual Property Brokers If You Plan To Work With One

At this level, you gained’t be assembly with or hiring an actual property agent, however it’s best to determine whether or not you’re going to make use of one and who you would possibly take into account working with.

Hiring a real estate buying agent isn’t required, however it’s extremely really helpful.

PROS And CONS Of Hiring A Actual Property Agent When Procuring For A Dwelling

PROS:

- It usually doesn’t price you a dime to rent a purchaser’s agent.

- An actual property agent saves you time and power, since they know the market and might help you zero in on houses which might be match for you.

- An agent handles the true property contact for you.

- A great agent is aware of how one can correctly current a suggestion in order that it doesn’t get rejected as a consequence of lacking data or poorly written language.

- An agent helps you handle affords, contingencies, inspections, and different deadlines.

- An agent has connections to each kind {of professional} you want alongside the way in which. Whether or not it’s a contractor, inspector, legal professional, or another kind of specialist, agent will offer you stable suggestions for whomever you want in your crew.

- An actual property purchaser’s agent will show you how to negotiate pricing in your new residence, and they’ll additionally perceive when a house is overpriced. This helps you make acceptable residence affords so that you simply neither overpay nor offend the vendor.

- An agent will maintain your schedule on monitor when it’s time to purchase. This helps you keep away from delayed closings and missed deadlines that may result in vital issues when shopping for a house.

CONS:

- Potential conflicts of curiosity: It’s doable your agent could suggest a contractor or inspector in her community reasonably than one who’s finest for you.

- Threat of hiring a foul agent: an inexperienced or sloppy agent may cause main issues in the event that they mishandle your contracts and paperwork

Total, an actual property purchaser’s agent can prevent an excessive amount of time, cash, and nervousness when buying a house.

When you determine to rent an actual property purchaser’s agent when purchasing for a house, do your analysis to seek out one with an excellent popularity, private suggestions, and glorious opinions.

Analysis Actual Property Attorneys If You Plan To Rent One

You’re not required to rent an legal professional when shopping for a house.

A house is a big buy, although, and a lawyer can grant you peace of thoughts by serving to you navigate contracts and buy phrases, reasonably than entrusting the authorized facets to an actual property agent.

An actual property lawyer understands all facets of the house shopping for course of, and a few individuals rent attorneys to assist handle the contract because it develops with the true property agent.

The lawyer may also advise you on different issues equivalent to potential lender delays that would have an effect on your closing, inspections, and title search.

A residence’s last contract consists of dozens of pages of authorized paperwork that may rapidly overwhelm patrons (particularly first-time owners), so chances are you’ll wish to take into account hiring one that can assist you navigate the method.

When you’re buying a house in a special state, shopping for one via an property sale, public sale, or financial institution, or shopping for a house with structural or different main harm, it’s best to at all times rent a lawyer to assist with your house buy.

When you’re a first-time homebuyer that’s not promoting one other property on the identical time, hiring an legal professional is elective — however will grant you an additional degree of safety and safety towards errors and different potential issues.

When you do wish to rent an legal professional, this can be a good time to ask round for suggestions on good attorneys.

Don’t search for the most affordable or most-promoted, flashy legal professionals. As a substitute, examine private references, opinions, expertise, and historical past when hiring an actual property legal professional.

Analysis Houses In Your Space

Earlier than you start touring houses and speaking to brokers, do a little bit of analysis on houses and places within the space you’re all for shopping for.

Go into your search with a good suggestion of what location you’d wish to stay in (even perhaps what neighborhood) primarily based on costs, colleges, visitors, commutes, and different elements that matter most to you.

The place you purchase your house could have a big influence on pricing and negotiations. The extra you understand upfront, the faster and extra successfully you’ll have the ability to store for and negotiate in your new residence.

When you’ve carried out all of your analysis and ready your funds, you’re able to discover a lender and get pre-approved to your new residence mortgage.

Step Three: Discover A Lender And Get Pre-approved For Your Mortgage Mortgage

When you’ve budgeted for homeownership and accomplished your pre-purchase analysis, the subsequent step in home-buying is to discover a mortgage lender and get pre-approved for a mortgage mortgage.

Decide What Kind Of Mortgage Mortgage You’ll Select

Mortgage loans include several options, and figuring out your selections upfront helps you discover a lender that gives the most effective charges for the kind of mortgage you need.

The choices you’ll select from embody the mortgage’s time period, kind of rate of interest, and mortgage kind.

- Mortgage time period refers to how lengthy you’ll take to repay the mortgage, and could also be 30 years, 15 years, or one other size of time. The mortgage time period impacts your month-to-month mortgage funds, the rate of interest, and the general price (whole curiosity) of your mortgage.We suggest a 30-year time period as a result of the decrease funds offers you a bit of additional safety, in case you face monetary hardships sooner or later. Plus, you possibly can slash the price of your mortgage (curiosity) by making funds each different week as a substitute of each month, or by doubling your month-to-month funds.

Longer-term loans are dearer and usually include greater rates of interest.

Shorter-term loans are inexpensive and usually include decrease rates of interest.

- Rate of interest kind refers as to whether you’ll take out a fixed-rate or adjustable-rate mortgage. We suggest a fixed-rate mortgage.

Fastened charge loans offer you one rate of interest that is still the identical all through the time period of your mortgage. They’re a bit greater however provide low threat and stability with the intention to funds for and afford your mortgage.

Adjustable charge loans usually present decrease rates of interest at first, however the charges change all through the time period of your mortgage. The fluctuations introduce problems, equivalent to delayed curiosity funds, that may improve the stability in your mortgage. Moreover, adjustable charges imply you can’t funds for one regular mortgage fee, since it will possibly improve at any time.

- Mortgage kind refers as to whether you’ll take out a traditional, FHA, or speciality mortgage. Most loans are standard, nonetheless there are other types of loans equivalent to FHA and speciality loans which have been created by the federal government and lenders for individuals in distinctive conditions.

Prepayment penalties are charges imposed while you pay your mortgage off sooner than agreed. Verify together with your lender to make sure your mortgage mortgage doesn’t cost prepayment penalties.

Ideally, you’ll make half-payments in your mortgage each two weeks, that can assist you repay your mortgage faster and reduce your general curiosity prices considerably. To do that, you want a mortgage that doesn’t cost prepayment penalties.

Whenever you’ve determined what time period, curiosity kind, and mortgage kind you’ll apply for, you’re prepared to decide on a mortgage lender.

Select A Mortgage Lender

When selecting a lender, your main concern needs to be discovering the bottom rates of interest.

Not all lenders cost the identical charges, so a little bit of analysis could make a world of distinction.

Reasonably than name round and speak to particular person bankers (the old style approach), you should utilize a mortgage charge comparability website to rapidly decide who’s providing the bottom charges on mortgages.

Websites equivalent to Bankrate, Smartasset, and Credible provide the likelihood to browse mortgage charges on-line after answering a couple of easy questions.

Some websites even permit you to get pre-qualified or pre-approved for a mortgage mortgage on-line.

Speak to lenders individually to be taught what further charges and prices are associated to their mortgage loans. You might discover that some provide further financial savings at closing time, which may very well be an element when selecting the most effective mortgage.

Secondly, the popularity of your lender is vital. Do a little bit of analysis to make sure that yours is skilled and dependable, so your papers don’t get misplaced or misfiled, which may result in issues at closing time and even long-term credit score issues.

When you’ve chosen a mortgage lender, you’re prepared for the subsequent step: getting pre-approved for a mortgage mortgage.

Get A Pre-Permitted Mortgage Letter

Getting a mortgage pre-approval letter out of your lender makes it simpler to purchase a house.

The pre-approval letter lets you understand precisely what you possibly can afford.

It additionally could provide you with an edge to find the most effective offers and properties, since many actual property brokers are extra prepared to work with pre-approved patrons.

The time period “mortgage pre-approval” is commonly confused with “mortgage prequalification,” so let’s begin by understanding how the 2 processes are totally different.

- A mortgage prequalification is an informal course of that offers you an thought of how a lot cash you possibly can afford to spend on a house.Prequalification isn’t a proper approval from a lender.

Prequalification is often primarily based on the data you give, plus a “mushy credit score” (much less thorough) examine.The benefits of prequalification are that 1) it’s a simple and fast course of and a couple of) it helps you establish how a lot a lender would possibly assume you possibly can afford to spend on a house.Get a prequalification while you’re questioning whether or not it’s time to start purchasing for a house. It may be an ideal assist in figuring out what measurement residence and mortgage you would possibly have the ability to buy.Whenever you’re severe about shopping for, although, and able to soar within the automotive and go have a look at houses, you’ll wish to safe a mortgage pre-approval.

- A mortgage pre-approval is formal approval by a lender. To acquire a pre-approval, you submit documentation to confirm that each one the data you submit is appropriate. Through the verification course of, your lender will examine your credit score experiences in a course of referred to as a “arduous” credit score inquiry, which might have an effect on your credit score rating by a couple of factors.You ought to be 100% able to stroll out the door and begin purchasing for houses earlier than you request a pre-approval from a lender.

Hold your funds regular from this level ahead!

When shopping for a house, it’s vital to maintain your funds regular all through the homebuying course of.

Strive to not apply for any new credit score, make any main purchases, or give up or change jobs. Positively don’t let your self get behind on any funds!

Lenders check your credit score greater than as soon as all through the method, and — Sure, you will be denied a mortgage mortgage even after closing (though it’s uncommon).

Any modifications to your funds may additionally trigger severe delays when it’s time to shut in your mortgage mortgage.

Upon getting your pre-approval letter in hand, you’re prepared to start purchasing for a house and negotiating costs.

Step 4: Store For Your Dwelling

Now that you simply’ve budgeted, researched, discovered a lender, and obtained a pre-approval letter, you’re prepared for the enjoyable half: purchasing to your new residence.

This half goes a lot smoother in case you have an actual property purchaser’s agent as a result of they might help coordinate residence excursions and negotiate worth while you discover the correct residence.

Whenever you’ve discovered your new residence and had your provide accepted, you’re prepared for the subsequent step: making use of for the mortgage mortgage.

Step 5 : Make An Supply — Understanding “Escrow”

Whenever you discover the house that you really want and are able to make a suggestion, your actual property agent will deal with the negotiations.

Most affords embody contingencies that must be met earlier than the sale goes via, equivalent to residence inspection and value determinations, in addition to your last mortgage mortgage approval.

Presently, religion deposit of usually 1-2% of the house worth is often put into an escrow account.

This escrow protects the vendor in case the client backs out with out simply trigger, and protects the client from handing over massive quantities of money earlier than inspection and title verification are full.

The cash you set into the escrow account is often utilized to the down fee of your house when the acquisition goes via.

You’ll be able to again out of the deal in case your contingencies aren’t met, nonetheless, the provide is a binding settlement as soon as the phrases of the deal are accepted.

As soon as your provide is finalized, you progress on to the closing course of.

Step Six: Full The Closing Course of

When you’ve discovered the house you need and had your provide accepted, the closing process begins.

A mortgage “closing,” the ultimate step in homebuying, is while you signal the paperwork wanted to buy your house.

Your mortgage closing (when you take out a mortgage mortgage) and residential closing often occur on the identical time.

Whether or not you all sit round a desk inspecting paperwork or every signature is collected individually by mail or digitally depends upon what state you reside in.

Apart from you, the client(s), there are a number of different events that take part in closing:

- Your actual property agent, in case you have one

- Title insurance coverage firm

- Escrow firm

- Your actual property legal professional, in case you have one

- Vendor’s actual property legal professional

- Your lender

After closing, you might be legally accountable for the mortgage mortgage in your new residence.

Money patrons can usually shut on a home inside a pair days, however when you’re paying to your residence with a mortgage mortgage, it takes longer.

Closing a mortgage, from the time you apply to your mortgage to the ultimate signature, usually takes 45 – 60 days. The size of time it takes will be influenced by elements equivalent to your credit score rating, employment historical past, and different elements tied to your funds.

The complete closing course of consists of:

- Schedule your house inspection. This course of can take time, so it’s best to schedule the house inspection instantly to keep away from delays within the closing course of.

- Apply to your mortgage: Filling out your mortgage utility ought to solely take between 20 – 60 minutes, in case you have the paperwork prepared upfront.

- Submit your paperwork: The next paperwork are usually required to use for a mortgage mortgage:

- Employment data (title, tackle, contact data) for the previous two years

- Landlord contact data

- Financial institution, retirement, and funding account statements

- Proof of revenue (pay stubs or tax returns)

- Different paperwork as requested by your lender, equivalent to enterprise licenses, pupil mortgage deferment papers, and written explanations of any “atypical” deposits.

Moreover, your mortgage officer could request extra paperwork to additional doc monetary data associated to your revenue, property, money owed, and employment. They might additionally require you to elucidate previous conditions equivalent to bankruptcies, foreclosures, or different forms of assortment or delinquent accounts.

- Obtain a mortgage estimate and conditional approval: It’s best to obtain a mortgage estimate that particulars the phrases, circumstances, and value of your mortgage mortgage inside three days of submitting your utility.

- Appraisal: Your mortgage lender will order an appraisal when you signal and return your preliminary mortgage paperwork. Sometimes, you have to pay for the appraisal earlier than it may be scheduled.

- Lender evaluation of residence appraisal: Lenders evaluation and examine the appraisal when it is available in. Sometimes, lenders approve the appraisal. Nonetheless, if the appraised worth is far totally different than what the lender anticipated, they might schedule a second appraisal.

- Buy owners insurance coverage, which your lender would require earlier than giving last approval in your mortgage.

- Mortgage processing and underwriting: Mortgage processors evaluation all of your data and compile it into an organized file for the underwriter. They order your credit score report, confirm your employment and financial institution deposits, order a property inspection (if required) and appraisal, and order a title search in your new property. Subsequent, the mortgage processor passes your file alongside to an underwriter who will evaluation and consider all of your documentation and data.The underwriter is the one who makes the ultimate determination in your mortgage mortgage, together with whether or not you might have the power to repay the mortgage. As soon as your mortgage is accepted, your rate of interest is locked in on the financial institution’s present rate of interest.