Why You Can’t Ignore Student Loan Payments

Skipping your student loan payments can affect more than your credit rating.

Missing one or two payments can affect your credit and make it difficult to get caught up financially.

The longer you let your payments slide, the more severe penalties you incur.

If you get more than 270 days behind on payments your loan can go into default, giving the government rights to:

- Take up to 15% of your paycheck.

- Take your tax refund.

- Take part of your Social Security benefits.

For example, disabled veteran Rick Tallini of Long Island, New York had trouble making his payments for 26 years.

Originally, Rick worked a full-time job while attending law school at night.

He finished law school with $60,000 in student loan debt.

Because he had trouble finding steady employment after law school and never got quite his footing as a lawyer, Tallini was unable to make steady payments on his student loan debt. After years of struggling with unemployment and underemployment, his loans went into default.

Even after filing bankruptcy, Tallini’s student loan debt was not cleared but instead continued to grow.

- Ricks’s original $60,000 in loans grew to a $350,000 balance over the course of 26 years.

Twenty-six years after graduating, the disabled veteran now struggles to keep his loans out of default to protect his Social Security benefits.

Avoid Income-Driven Repayment Plans If Possible

If you can’t find a way to afford your payments, you might consider enrolling in an income-driven repayment plan (IDR) to help you avoid defaulting on your loans. The US Department of Education provides several repayment plan options for people who can’t afford their current payments.

We recommend you avoid income-driven repayment plans because they aren’t a healthy path to a financially solid future.

- The problem with IDR’s is that you can end up owing more than you borrowed even when you make on-time payments for years.

IDR plans adjust your monthly loan payment to an amount you can afford, which may be as low as zero dollars per month.

However, income-driven repayment plans come at a very high price.

At a time when your money is scarce, yet probably still hard-earned, the delayed costs associated with IDRs can put you so deep in debt that even your future grandchildren may be affected.

An IDR can lead to out-of-control interest fees that accrue over time and put you deeper in debt than when you started.

- When you pay student loans on a sliding-fee scale rather than sticking to the original (typically 10-year) plan, you can expect your overall loan balance to grow over time.

That’s because lenders keep charging interest regardless of what you can afford.

Often, the monthly payments you make on an IDR plan can’t keep up with the cost of the loan itself (interest).

If you remain on an IDR plan for a long period of time, your loan balance could end up larger than the amount you originally owed — even if you make every payment on time.

- For example, Kaitlyn Blount Crow graduated in 2015 with a degree in communications and $31,000 in student loan debt. She struggled to find a reliable job in journalism — or any full-time job at all. Crow enrolled in a federal-driven income repayment plan that adjusted her payments according to her earnings, which sometimes meant she didn’t have to pay anything at all. When she landed a full-time job, Crow began making $150 monthly payments, (which still wasn’t enough to cover the interest portion of her loan).

After making $2,249.28 worth of loan payments, Kaitlyn’s balance was $3,448.76 more than what she originally borrowed. What began as Crow’s $34,000 in loan debt grew to $34,448, even though she made her payments on time as agreed.

Crow’s story isn’t unique.

Many people make student loan payments on time every month only to watch their balance get bigger over time.

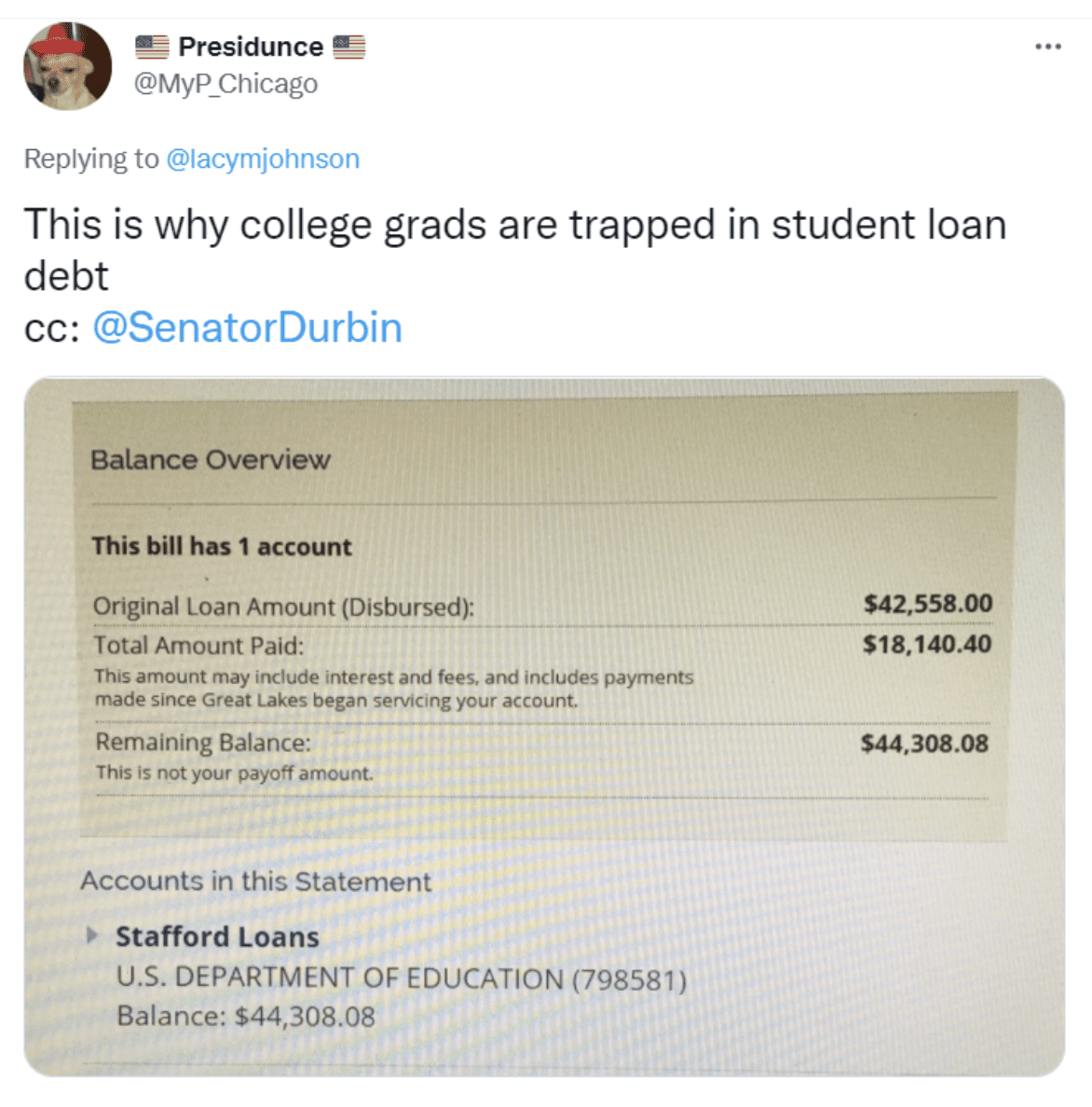

Twitter user @MyP_Chicago, shared a balance statement on Twitter that displays a starting debt of $42,558 that grew to $44,208.08 even after $18,140.00 in payments.

A normal person assumes that making on-time payments every month means their loan balance gets lower and lower over time until it’s eventually paid in full.

A normal person assumes that making on-time payments every month means their loan balance gets lower and lower over time until it’s eventually paid in full.

When you sign up for income-based payments, though, the interest that builds up can be greater than your loan payments. That means you never catch up on the interest or make a dent in your principal balance.

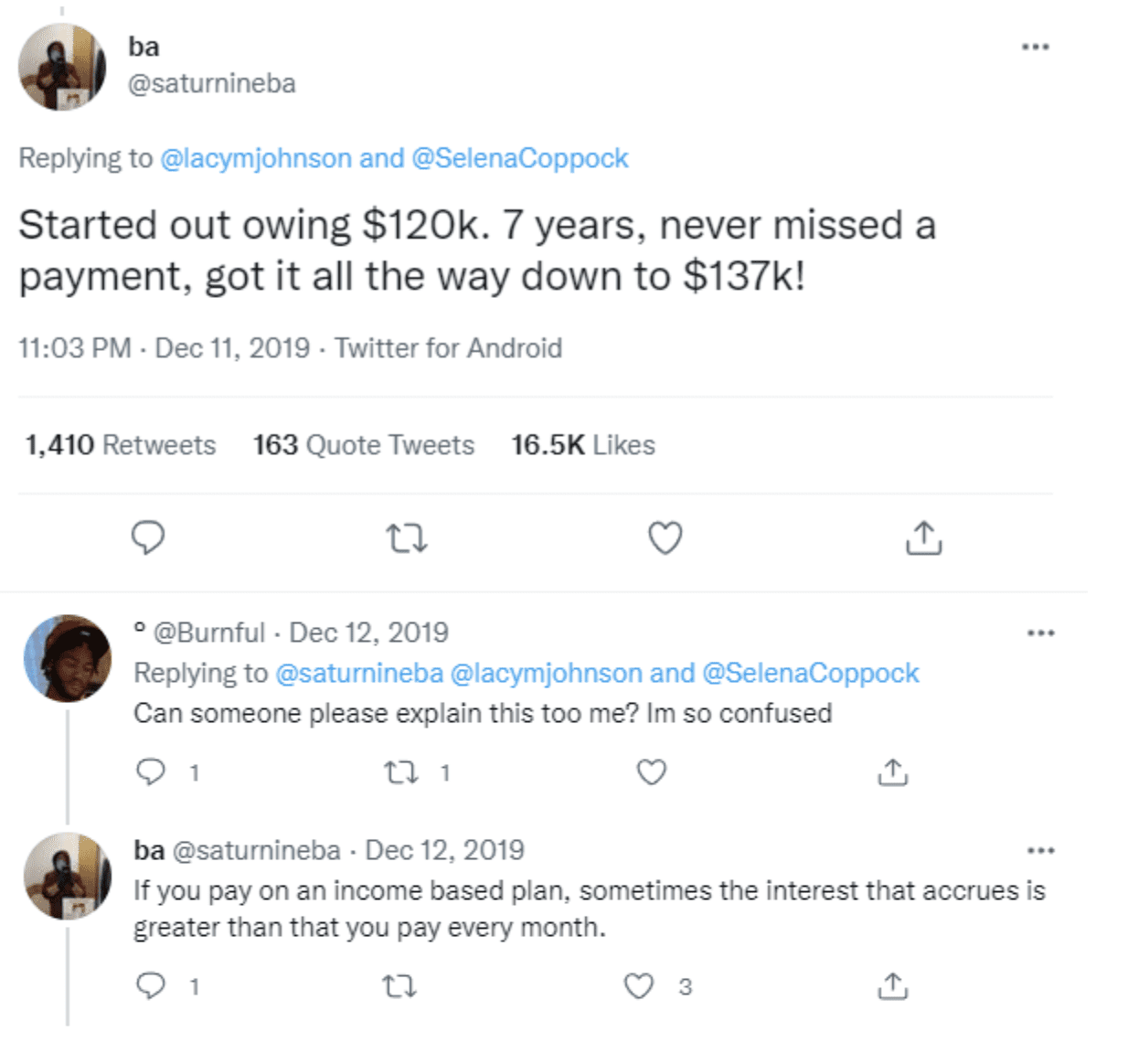

Twitter user @bsaturnineba started out with $120K in loans that grew to $137k, despite never missing a payment in seven years.

When another user asked how that’s possible, @bsaturnineba explained: “If you pay on an income based plan, sometimes the interest that accrues is greater than that you pay every month.”

If you absolutely cannot afford to make your student loan payments and an IDR is your only option, it is better than skipping payments or allowing your loans to default.

However, an IDR should be your last resort and it’s critical that you come up with a plan that ensures you won’t be on IDR for long.

Long-term use of IDR plans means you may risk compromising your family’s financial future for many years, or even for life.

{kind=link}