The excellent news is most of us can anticipate to dwell longer. The unhealthy information is that the decline of defined-benefit pensions, together with chronically low rates of interest, makes it tougher for us to keep away from outliving our cash.

For these with out office defined-benefit pensions, annuities can offset that danger by appearing as a type of longevity insurance coverage. You hand over capital to an insurance coverage firm immediately in trade for a assured circulation of earnings for so long as you reside. In an actual sense a DB pension, with its assured payouts, is annuity-like. As are applications just like the Canada Pension Plan (CPP) or Outdated Age Safety (OAS).

Regardless of related terminology, defined-contribution pensions, RRSPs, TFSAs, and non-registered financial savings should not actual pensions, cautions Schulich Faculty of Enterprise finance professor Moshe Milevsky. Whereas these autos will assist out in retirement, the one means you possibly can create an actual assured earnings for all times is to annuitize, he explains within the second version of Pensionize Your Nest Egg.

Nonetheless, annuities are underutilized as a result of they’re misunderstood or considered as undesirable. But, new “fintech” alternate options could do the identical factor as annuities, solely utilizing phrases comparable to peer-to-peer longevity insurance coverage or funding funds with longevity insurance coverage.

Milevsky argues that even at immediately’s rock-bottom rates of interest, annuities ought to pay greater than comparable fixed-income investments due to the built-in mortality credit. “Anybody who purchased an annuity 5 years in the past may be very joyful,” Milevsky says.

He provides: “Everybody ought to have a supply of earnings that’s predictable, inflation-adjusted and can final for the remainder of their lives.” The trick is realizing when to annuitize. The longer you wait, the extra you obtain on a month-to-month foundation. Milevsky’s rule of thumb is to annuitize when the loss of life fee exceeds the rate of interest. For instance, comparatively few die by 65, so the loss of life fee is underneath 1%; purchase an annuity now and it provides you with little greater than present rates of interest. Wait till your mid-70s and the loss of life fee begins to rise. That’s when annuities begin to look a lot better.

This query usually arises the yr a retiree turns 71 and is pressured to transform an RRSP right into a Registered Retirement Earnings Fund (RRIF) or an annuity. Price-only planner Marie Engen, co-owner of Boomer & Echo, says this isn’t an both/or case. You most likely ought to do each, notably as you progress into your 70s and 80s. Ideally, she says, pensions and annuities will cowl primary retirement bills, leaving the remainder for funding progress and extra liquid entry to cash for extra pleasant life-style bills.

For wholesome males, Milevsky suggests annuitizing between 70 and 80, including 5% or 10% extra annually, till you’re nearly fully annuitized between ages 80 and 95. As a result of spouses and kids might be impacted, the entire household wants to hitch the dialog, notably since capital that has been annuitized can’t be transformed again. Which means your heirs will inherit little or none of what’s annuitized.

Take note the excellence between registered and non-registered annuities. Funds from registered annuities are absolutely taxable like RRIFs and, on loss of life, heirs will probably be taxed based mostly on a same-day valuation. Based on Ivon Hughes of Montreal-based LifeAnnuities.com, a wholesome 65-year-old male not wanting a assure interval would get $531.49 month-to-month earnings from a $100,000 registered annuity. At age 71 this earnings rises to $636.34, and at age 80, he’ll get $946.76.

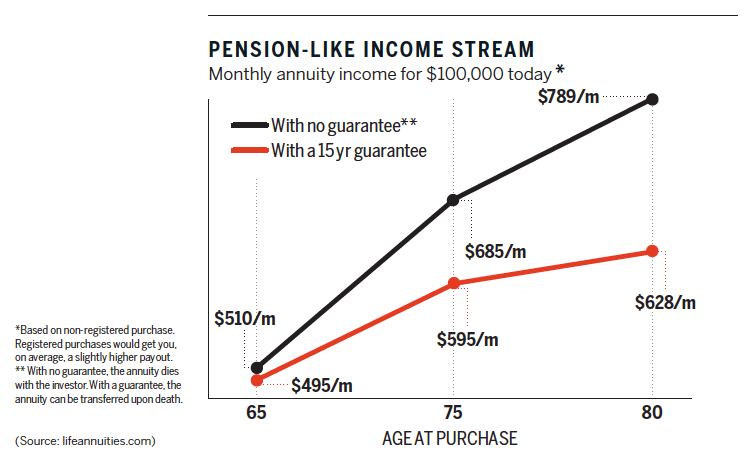

With non-registered “prescribed annuities” the curiosity paid out is taxable however not the return of capital. Take note, the Canada Income Company is updating its mortality tables and rising the taxable portion—individuals are dwelling longer. That makes annuitizing with registered funds extra enticing, Milevsky says. A $100,000 non-registered annuity with no assure interval pays out $509.97 at 65, $606.12 if acquired at 71, and $789.03 at age 80.

Milevsky favours plain-vanilla annuities and cautions towards shopping for too many bells and whistles: each time you add ensures, minimums, and survivorship advantages, you water down the mortality credit.

{kind=link}