A couple of 12 months in the past, I ran Meta Platforms (Nasdaq: META) by means of my Worth Meter display.

My conclusion was that the inventory was extraordinarily undervalued.

For the primary four-plus months afterward, my name seemed horrible.

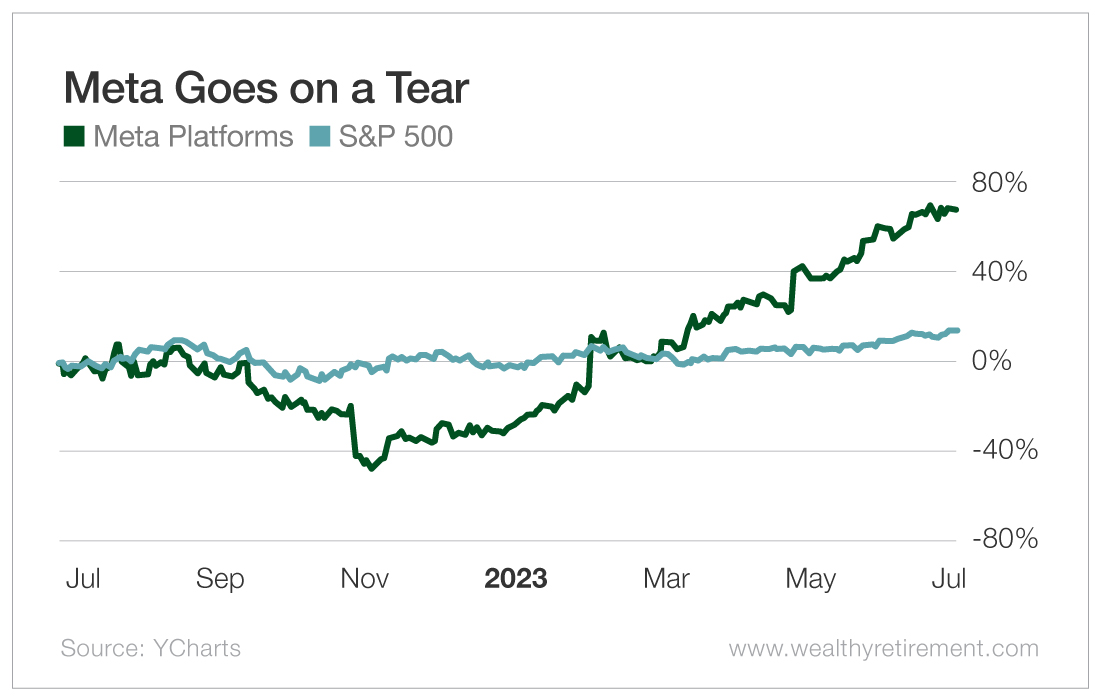

Between June and November, Meta’s inventory was practically minimize in half, badly trailing the efficiency of the S&P 500.

However from there, Meta has been on an absolute tear.

From early November 2022 by means of as we speak, Meta shares have gone from $90 to $286, as of this writing.

With this big rebound, my name now appears to be like fairly good…

Excellent truly.

Meta’s share worth is now up 68%, outperforming the S&P 500 by nearly fivefold over the identical interval.

This as soon as once more reveals how endurance is probably the one most essential attribute an investor can possess in the event that they wish to beat the market.

Regardless of the preliminary near-50% decline, Meta has been an enormous winner.

So how does Meta’s valuation look as we speak?

At the moment, the market is appraising Meta at $705 billion.

That’s an enormous quantity, nevertheless it’s nonetheless down from the height valuation of greater than $1 trillion that the inventory hit in 2021.

For the present $705 billion market valuation, anybody shopping for shares of Meta as we speak is getting a enterprise that generated $23 billion in earnings final 12 months.

From a valuation perspective, that equates to a 3.3% earnings yield ($23 billion / $705 billion = 3.3%).

That doesn’t look extremely low cost to me.

In truth, it appears to be like slightly costly.

However there’s one thing hidden within the numbers that we should think about…

Meta is aggressively spending on analysis and improvement by means of its Actuality Labs subsidiary, which is targeted on the metaverse.

Final 12 months, Actuality Labs misplaced $13.7 billion.

With out that, Meta would have earned greater than $40 billion from its core Fb enterprise.

In some unspecified time in the future, the aggressive spending and cash shedding by means of Actuality Labs are going to cease.

In truth, the Actuality Labs subsidiary may ultimately make cash. Maybe a whole lot of it!

However I don’t know that it’ll.

And modeling how a lot cash Actuality Labs goes to burn by means of or ultimately create is extraordinarily troublesome given how little we find out about it. Although the analyst group has been engaged on it.

At the moment, the consensus analyst estimate for Meta’s earnings per share for this 12 months is $11.72. With Meta’s share worth at $286, that equates to a price-to-earnings (P/E) ratio of 24.

For 2024, the consensus analyst earnings estimate jumps to $14.60 per share. That might be a P/E ratio of 20 occasions 2024 earnings.

Each of these numbers strike me as being a fairly truthful valuation for this excellent enterprise.

Once I gave Meta an “Extraordinarily Undervalued” ranking in June 2022, we have been in a position to buy shares of this firm at nearly half these valuations.

We’ve had an awesome run with Meta’s inventory, however the worth proposition right here has modified.

At present, The Worth Meter charges Meta Platforms as “Appropriately Valued.”

![Ethereum [ETH] investors must know this before opening a long position](https://nourishmoney.com/wp-content/uploads/2022/08/Untitled-design-53-1000x600-120x86.png)

{kind=link}