When you wait lengthy sufficient, the inventory market will serve up a chance to buy an organization you want at an interesting value.

This week, I’m placing Brookfield Infrastructure Companions (NYSE: BIP) by way of The Worth Meter, and I believe you’re going to like what you see.

Brookfield has a quite simple marketing strategy.

The corporate buys high-quality, long-lasting infrastructure property that generate predictable money flows for many years.

I’m speaking about towers, tunnels, highways, pipelines, energy crops, electrical strains and railways…

Plus another belongings you wouldn’t consider. (Extra on these beneath.)

These are big-dollar infrastructure property that present key companies within the areas the place they function.

There aren’t many firms that may write the checks to buy these sorts of property.

However Brookfield is one in every of them, and the corporate is superb at what it does.

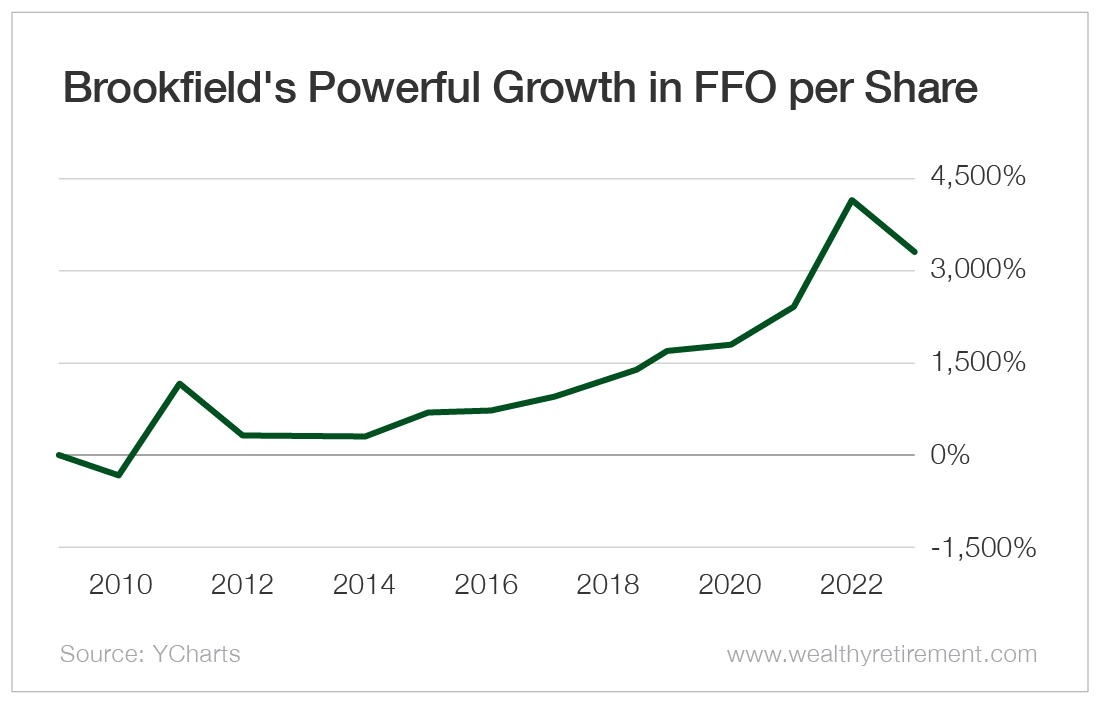

Since its inception in 2008, Brookfield has grown its funds from operations (FFO) per share by greater than 3,000%.

The corporate splits its property into 4 principal infrastructure segments.

No. 1: Regulated Utilities

Utilities are boring!

However they’re boring in a wonderful method.

Brookfield’s utilities are reliably worthwhile, and their money flows improve at a gradual tempo over time.

The corporate properly selected to diversify its utility property geographically so it wouldn’t be overly influenced by any single regulatory regime.

These property embrace energy era services, electrical energy transmission strains and a commodity export terminal.

Collectively, they’re price billions.

For the primary six months of 2023, Brookfield’s utilities generated $432 million – which was roughly one-third of the corporate’s FFO.

No. 2: Transportation

Brookfield’s transportation infrastructure property are distinctive, irreplaceable and important to their areas.

For instance, the corporate is the one supplier of a railway community within the southern portion of western Australia, the place it owns 5,500 kilometers (km) of monitor.

It additionally has 3,800 km of toll roads in Brazil, Peru and India…

To not point out port terminals within the U.Okay. and Australia and a liquefied pure gasoline export facility within the U.S.

Thus far this 12 months, these transportation property have generated $391 million in FFO, which is slightly below the quantity the utilities property have generated.

No. 3: Power

Brookfield owns a number of midstream power property.

“Midstream” refers back to the infrastructure that delivers oil and gasoline after they’ve been pumped out of the bottom.

The corporate operates greater than 15,000 km of pipelines in the USA and one other 10,000 km in Canada.

It can also retailer roughly 600 billion cubic ft of pure gasoline for its prospects.

By the primary six months of 2023, Brookfield generated $359 million in FFO from its midstream property.

No. 4: Information

Regardless of being Brookfield’s smallest phase, knowledge presents an enormous development alternative going ahead.

Firm administration says the demand for knowledge is rising sooner than the demand for some other commodity on the planet.

As a way to facilitate that development, the world wants firms like Brookfield to proceed investing in knowledge transmission and storage methods.

Brookfield has already invested $1.5 billion into its knowledge phase (which generated $142 million in FFO within the first half of 2023), and it owns 485 million watts of working capability.

This phase is rising, and it’s rising quick.

All of This Infrastructure Creates Progress and Dividends

This large base of infrastructure property gives Brookfield with sturdy (and rising) free money flows.

The corporate has used that free money circulate to steadily develop its dividend by an annualized 8% per 12 months over the previous decade.

Nevertheless, as a result of rise in rates of interest, the share costs of firms like Brookfield have had a tough go to this point in 2023.

There may be much less demand for dividend shares when traders can get excessive charges of return from time period deposits and Treasury payments.

There may be additionally concern that infrastructure firms that carry debt, together with Brookfield, will see a dip in income because of rising charges.

However I’m not involved about that on this case, as 90% of Brookfield’s debt is mounted fee.

Furthermore, the rise in rates of interest has truly led to decreased competitors with regard to buying new infrastructure property.

Which means decrease buy costs and better returns for the corporate’s investments going ahead.

With the inventory down 12 months thus far, Brookfield presently yields a robust 6%.

Plus, administration is projecting FFO to develop by 12% yearly over the subsequent three years.

Now’s a unbelievable time to purchase shares of an amazing firm that provides a big, steadily rising dividend.

The Worth Meter charges Brookfield Infrastructure Companions as being “Barely Undervalued.”

When you’ve got a inventory that you just’d wish to have rated by The Worth Meter, go away the ticker image within the feedback part beneath.

{kind=link}