Boasting a 41% market share, PayPal (Nasdaq: PYPL) is the proprietor of the only most dominant on-line cost know-how on this planet.

Nonetheless, to say that the market has given up on shares of this firm could be a significant understatement.

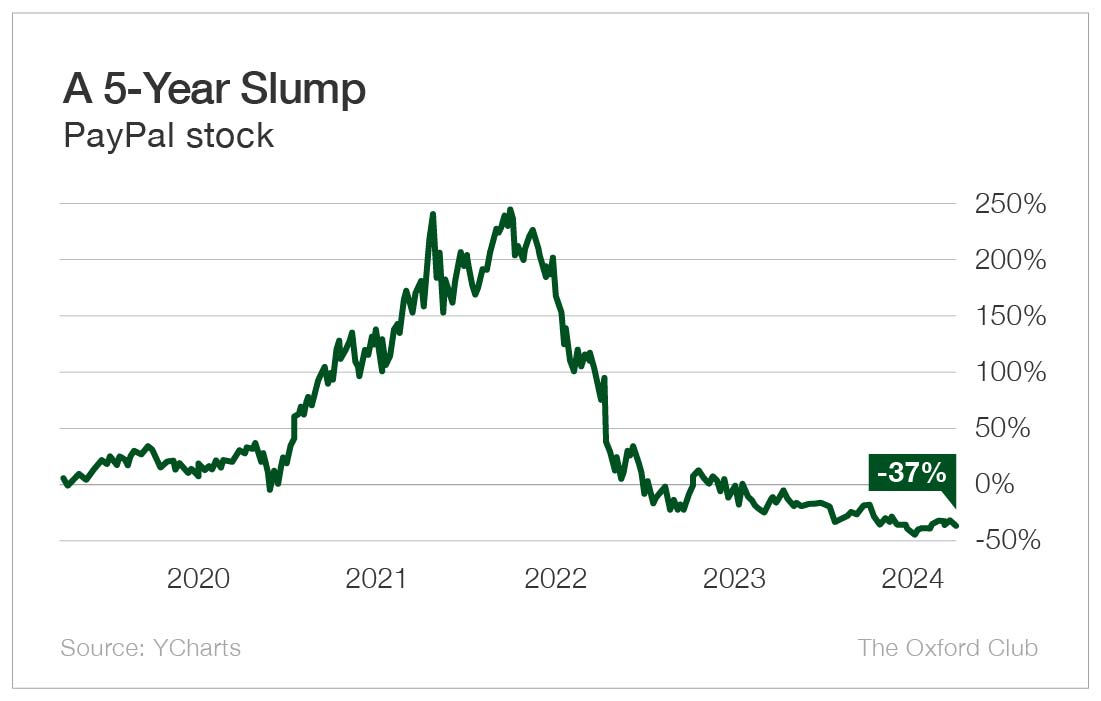

The inventory’s latest collapse has been extreme.

In July 2021, it peaked at simply over $300. At this time, the shares change fingers for round $60.

Over the previous 5 years, the inventory is down a really disappointing 37%.

Operationally, although, PayPal’s efficiency doesn’t look too unhealthy to me.

Whereas the five-year inventory chart goes approach down, the five-year income chart exhibits that PayPal continues to be rising fairly properly.

What stalled PayPal’s inventory worth wasn’t a scarcity of income progress; it was a drop in working earnings.

Whereas income has continued to develop, working income haven’t. PayPal’s working earnings went from $3.3 billion in 2020…

To $4.3 billion in 2021…

Then again right down to $3.8 billion in 2022.

So the corporate did see first rate progress over that span. However the market clearly didn’t look after the lower in working earnings from 2021 to 2022.

When a progress firm stops rising, the inventory market will be ruthless in its valuation of that firm’s inventory.

The chart beneath exhibits how dramatically PayPal’s valuation has fallen.

When the inventory was at its peak in 2021, buyers had been valuing the corporate at over 100 occasions trailing earnings.

As you possibly can see, the market is prepared to pay a steep worth for corporations it thinks are going to develop at a pleasant clip for a really very long time.

The shift towards digital funds throughout the pandemic additionally obtained buyers enthusiastic about PayPal’s inventory.

There’s little doubt PayPal was overvalued when it was buying and selling at 100 occasions earnings. However now that the market has soured on its future progress, the shares are valued way more attractively.

Right here’s the factor, although…

I don’t assume PayPal’s progress is wherever near being completed.

The transfer to digital funds continues to be a really highly effective long-term development that the corporate goes to profit from.

PayPal’s working earnings elevated from $2.6 billion over the primary 9 months of 2022 to $3.3 billion over the identical interval in 2023…

And for all of 2023, the typical earnings per share (EPS) estimate is simply $4.95.

With the share worth round $58 as I write, PayPal is buying and selling at simply 11.7 occasions its 2023 projected earnings.

That’s the type of valuation you’d count on to see for an organization that has just about no future progress on the best way.

For PayPal, that simply isn’t the case.

The common EPS estimate for PayPal in 2024 is $5.50. That will be very good 11% progress from final yr’s anticipated EPS determine.

The longer-term analyst expectations are for PayPal to proceed rising at a charge of at the very least 7% by way of 2027. And I really feel fairly assured that PayPal’s progress will proceed far past then.

What all this implies is that at present, an investor can purchase shares of PayPal at a valuation that suggests no future progress ever.

However right here’s the fact: This can be a firm that…

- Is dominant in its market

- Is being boosted by an enormous tailwind (the digital funds megatrend)

- Nonetheless has loads of progress forward of it.

The market has given up on this firm, and that has created an excellent shopping for alternative.

The Worth Meter charges shares of PayPal as being “Extraordinarily Undervalued.”

In case you have a inventory that you simply’d wish to have rated by The Worth Meter, depart the ticker image within the feedback part beneath.

{kind=link}