Brinker Worldwide (NYSE:EAT) is a inventory on the rise. The American hospitality chain affords variety within the type of a number of eating places — Chili’s Bar & Grill, Maggiano’s Little Italy, and It’s Simply Wings — and operates throughout 29 international locations. The agency applied a number of constructive adjustments to its operations in latest months and seems to be reaping the advantages. Nonetheless, I’m bullish due to Brinker’s valuation. The inventory has a price-to-earnings-to-growth (PEG) ratio of 0.8x, making it a uncommon worth decide in a crowded U.S. market.

A Winner in Informal Eating

Informal eating was hit onerous through the pandemic, but it surely’s making a comeback. Brinker has three major restaurant manufacturers, as famous above. Chili’s Bar & Grill affords a basic informal eating expertise with a deal with inexpensive and comforting Tex-Mex meals. It’s bought a loyal buyer base and seems to be successful over new prospects in a aggressive market.

In reality, a latest viral TikTok urged that eating in at Chili’s at the moment represents a less expensive possibility than a McDonald’s (NYSE:MCD) takeout. Chili’s has a “3 for Me” deal costing round $11 that features an appetizer, drink, and meal. Regardless of the viral-nature of the TikTok, it’s value highlighting that McDonald’s affords a $1 $2 $3 menu, however costs can differ by location. Chili’s has additionally been voted among the many high 50 hottest restaurant chains within the U.S.

Maggiano’s Little Italy affords a extra upscale informal eating expertise, serving a variety of home-comfort Italian meals for households and celebrations. It has a smaller footprint than Chili’s, but it surely caters to a selected area of interest and is well-regarded throughout the U.S.

Subsequent, we’ve got It’s Simply Wings, a comparatively new digital model launched in 2020 for supply and takeout. Brinker initially targeted on It’s Simply Wings as a delivery-only model. Nonetheless, it lately built-in the unit into the Chili’s menu as a consequence of weakened demand for digital manufacturers general. Total, information suggests it’s been a helpful addition to the corporate’s portfolio and has allowed Chili’s to achieve credibility as a “wing participant,” based on Brinker’s CEO.

Promising Developments

Brinker Worldwide can be implementing a two-pronged technique to enhance all-important margins. The corporate’s administration staff highlighted within the final earnings name that they lately launched a brand new menu with a 2% enhance in pricing. Moreover, the agency has considerably simplified the menu by eradicating much less common dishes and focusing extra on these with stronger margins. This streamlining reduces prices whereas permitting the agency to deal with its core choices.

Administration additionally highlighted that it’s seeing sturdy tailwinds from the alcohol division. That is constructive, as alcohol is all the time one of many highest-margin merchandise that eating places provide. The corporate says it has been capable of greater than double the gross sales of its specialty margaritas—made out of a pre-mix and offered for $10 and above—that are extraordinarily worthwhile. Administration additionally urged that the addition of wings to Chili’s menu could positively influence alcohol gross sales.

The corporate hopes the addition of Coors Gentle and Miller Lite to the menu will compound this, that means they now provide the highest 4 beers for joyful hour at very enticing worth factors.

Administration’s clear focus is on profitability, they usually’re assured these adjustments will result in greater margins. Brinker raised its profit forecast for Fiscal Year 2024, anticipating earnings per share between $3.45 and $3.70 and whole income between $4.30 billion and $4.35 billion. That’s up from revenue of $4.1 billion in Fiscal 2023 and earnings of $2.83 per share.

EAT Inventory Is a Sturdy Worth Play

On this more and more crowded market, it may be onerous to search out firms with sturdy and engaging valuation metrics. The corporate is at the moment buying and selling at 12.6x ahead earnings, placing it at a slight low cost to the sector. In the meantime, analysts see Brinker’s earnings rising a powerful 16.6% within the medium time period.

In flip, the ahead earnings metric falls to 11.4x in 2025 and 10.2x in 2026. Collectively, we even have a PEG ratio of 0.8x. Whereas the PEG ratio is, in fact, depending on analysts’ forecasts — which will be mistaken — I usually discover this metric to be the strongest indication of worth for non-dividend paying shares.

Is Brinker Worldwide Inventory a Purchase, In response to Analysts?

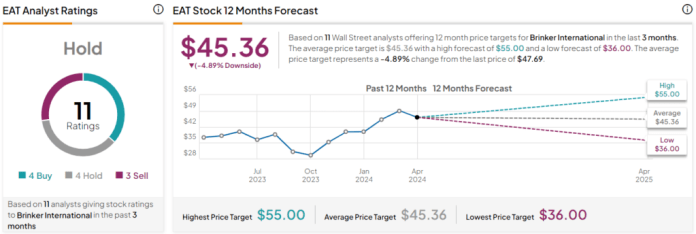

Brinker Worldwide has a Maintain consensus ranking on TipRanks primarily based on 4 Buys, 4 Holds, and three Sells given by analysts up to now three months. The average EAT stock price target is $45.36, implying 4.9% draw back potential.

The Backside Line on EAT Inventory

Regardless of the Maintain consensus ranking, I stay bullish on Brinker. It’s seeing some sturdy tailwinds in its enterprise, together with enhancing alcohol gross sales, and it’s specializing in enhancing its margins by shrinking the menu to double down on high-margin dishes. From a valuation perspective, it definitely doesn’t look costly at 12.6x ahead earnings, whereas its 0.8x PEG ratio is the true winner.

The put up Serving Worth with a 0.8x PEG Ratio – TipRanks Monetary Weblog appeared first on FinanceGrabber.

{kind=link}