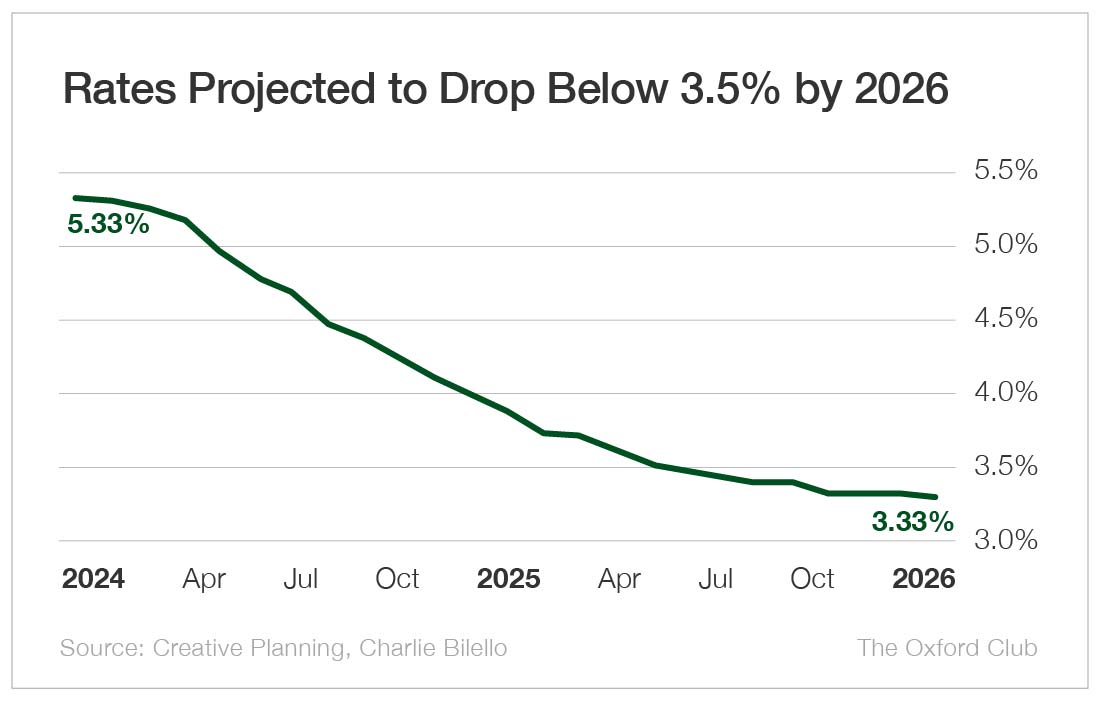

The market is at the moment forecasting a large lower in rates of interest over the subsequent couple of years.

Fed funds futures are projecting a 2-percentage-point decline between now and the top of 2025.

On this macro surroundings, the utilities sector ought to have a powerful tailwind for the subsequent two years.

Utilities are very delicate to rates of interest as a result of they should make investments closely of their capital-intensive operations (energy crops, water infrastructure, and so on.) and so they use a big quantity of debt financing to do it.

Debt isn’t an enormous drawback for these corporations, although, as a result of their money circulation from operations is extraordinarily dependable. Utilities usually have monopolies of their respective markets.

Now, the debt does minimize into earnings when rates of interest are rising, as a result of larger charges trigger corporations’ curiosity expense to extend. However the reverse is true when charges are falling: Curiosity expense goes down, and earnings widen.

Moreover, when rates of interest are decrease and time period deposits are much less enticing, traders turn out to be extra within the regular dividends utilities pay.

In March 2021, I beneficial an influence supplier by the identify of Vistra Corp. (NYSE: VST).

My bullish view on the corporate was not a results of the rate of interest outlook in any means, form or kind. Rates of interest have been close to 0% on the time, so they’d nowhere to go however up.

What I noticed in Vistra was an extremely low cost, cash-generating enterprise that the market had punished unfairly for a one-time hit to earnings.

Since then, the inventory has achieved extremely effectively regardless of the rise in rates of interest.

Vistra has returned 145%, versus 28% for the S&P 500 and simply 3% for the Utilities Choose Sector SPDR Fund (NYSE: XLU).

Readers who jumped on this commerce gained huge!

However you might be questioning how Vistra’s valuation takes care of this large worth enhance.

The quick reply is that I believe Vistra’s inventory nonetheless seems fairly low cost.

Over the subsequent a number of years, Vistra is anticipated to generate roughly $2 billion per 12 months in free money circulation.

Once we divide the corporate’s anticipated $2 billion in free money circulation by its enterprise worth of $27 billion, we discover that it’s at the moment buying and selling at a 7.4% free money circulation yield.

That’s a pretty valuation, and I anticipate Vistra’s free money circulation to solely enhance over time.

Even higher is what Vistra is doing with that free money circulation: aggressively returning it to shareholders.

Vistra at the moment has a dividend yield of two.14%. The dividend will develop as free money circulation retains rising. In reality, Vistra has almost doubled its quarterly dividend over simply the previous 4 years.

The corporate can be changing into extra aggressive with share repurchases.

Its share depend has dropped from 488 million to 357 million over the previous two years.

That’s a powerful share depend lower of 27%.

This sort of discount in share depend is extraordinarily helpful to shareholders when the inventory is undervalued, which Vistra’s has been.

Because the variety of shares drops, every remaining shareholder owns a proportionately bigger piece of the corporate.

I just like the utilities sector for the subsequent couple of years, and Vistra nonetheless represents wonderful worth inside it.

The corporate has a powerful free money circulation yield and stable development forward of it. It has been good to us previously, and I imagine it would proceed to be.

The Worth Meter charges Vistra shares as being “Barely Undervalued.”

In case you have a inventory that you just’d wish to have rated by The Worth Meter, go away the ticker image within the feedback part under.

{kind=link}