In July 2020, I tipped readers off to the most important insider buy I had ever seen.

The CEO of the Canadian reinsurer Fairfax Monetary (OTC: FRFHF) had simply spent $150 million of his personal cash to purchase shares of Fairfax.

Clearly, this was not only a trivial insider buy that was finished so the CEO may say he believed in his personal inventory.

This was a large insider buy that would have been finished for just one motive…

The CEO, Prem Watsa, believed his firm was extremely undervalued.

However we truly didn’t even want to invest on the rationale for Watsa’s buy.

As a result of the acquisition was so huge, Fairfax was obligated to difficulty a press launch. In that launch, Watsa mentioned…

At our [annual general meeting] and on our first quarter earnings launch name, I mentioned that our shares are “ridiculously low-cost.”

That assertion mirrored my recognition that within the 35 years since Fairfax started, I’ve by no means seen Fairfax shares promote at a much bigger low cost to their intrinsic worth than they’ve just lately.

I’ve now backed up my sturdy phrases by buying near US$150 million of Fairfax shares available in the market over the previous few days, as I imagine that this will likely be a superb long-term funding.

Watsa’s common buy worth was $308 per share.

That turned out to be a steal of a deal, and the person has made a boatload of cash.

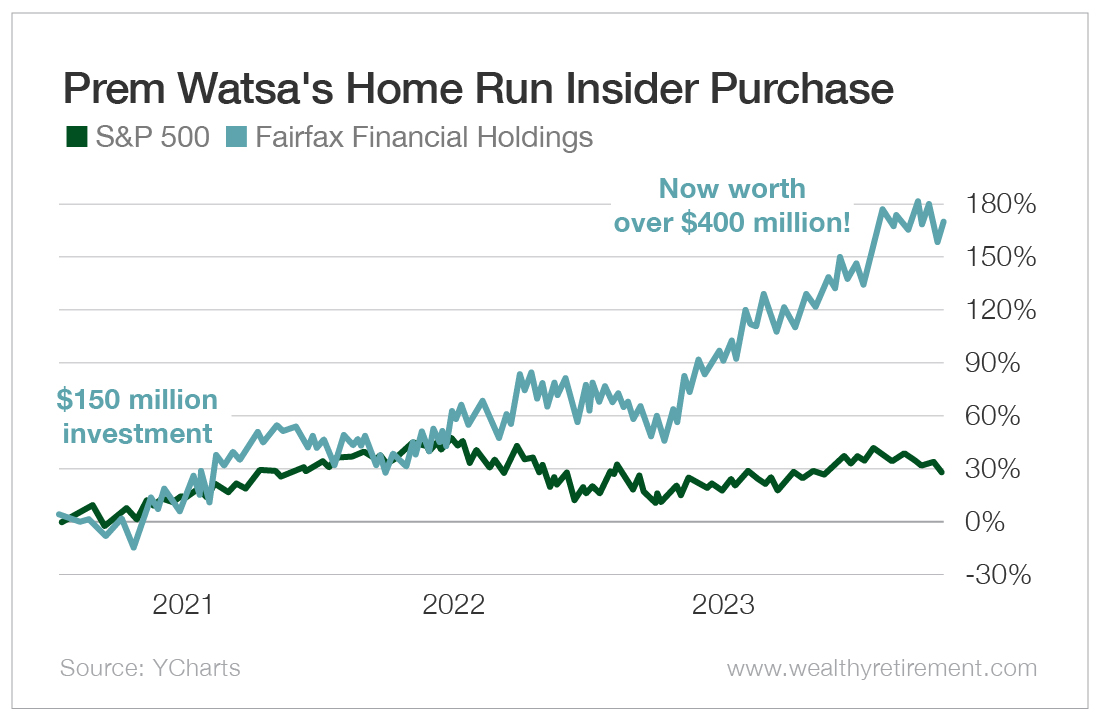

Since he purchased at $308 a little bit greater than three years in the past, Fairfax shares have steadily elevated and are actually buying and selling at effectively over $850 as I write.

That funding by Watsa has outperformed the S&P 500 by greater than 6X over that point.

Watsa’s $150 million funding in 2020 is now price over $400 million.

Which means he’s remodeled $250 million on this commerce alone!

Are Fairfax Shares Nonetheless Enticing Immediately?

Traditionally, Fairfax has traded at near 1.2 instances its guide worth.

However when Watsa made his $150 million funding, Fairfax was buying and selling at simply 0.7 instances guide worth. That was a giant low cost to the historic norm.

Proper now, Fairfax is buying and selling at 1.1 instances guide worth.

Whereas that’s barely under the corporate’s historic valuation, it definitely isn’t the deeply discounted valuation that prompted Watsa to make his huge buy.

This enhance within the firm’s valuation is without doubt one of the causes Watsa’s 2020 funding has been so profitable. Nevertheless it isn’t the one motive.

Guide worth itself has additionally grown in a serious manner.

Fairfax’s guide worth per share has greater than doubled from $409 on the time of Watsa’s buy to $834 as we speak.

This highly effective mixture of the enterprise greater than doubling its worth and the market lastly making use of a extra cheap a number of to that worth is what has made Watsa $250 million!

With the inventory now buying and selling just a bit bit below Fairfax’s historic price-to-book (P/B) ratio of 1.2, the corporate clearly isn’t the unimaginable cut price it was in mid-2020.

However due to Watsa’s skill to develop the corporate’s guide worth and its nonetheless moderately enticing P/B ratio, The Worth Meter charges Fairfax Monetary as being “Barely Undervalued.”

In case you have a inventory that you simply’d wish to have rated by The Worth Meter, go away the ticker image within the feedback part under.

{kind=link}