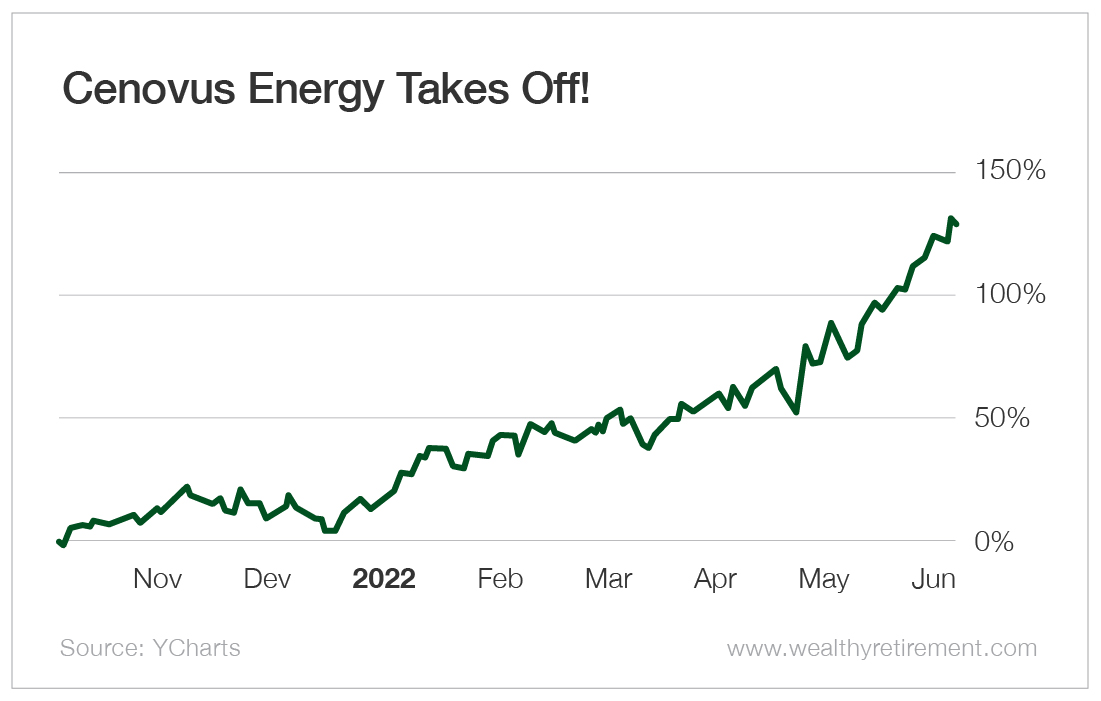

The final time I obtained actually excited concerning the valuation of an oil producer was in October 2021.

The inventory was Cenovus Power (NYSE: CVE), and I described the corporate’s valuation as being insanely low cost.

Shares of Cenovus have been then providing a staggering 27% free money movement yield.

That meant if the corporate had needed to, it may have paid a 27% dividend to shareholders.

Not surprisingly, Cenovus shares carried out very properly after that – greater than doubling in lower than a yr.

I’ve now noticed one other oil producer that jogs my memory of Cenovus.

The one distinction is that the valuation of this inventory appears even higher.

The oil producer this time is Baytex Power (NYSE: BTE).

With the latest acquisition of Ranger Oil, Baytex is targeted on primarily Texas and the Eagle Ford oil formation.

For the second half of 2023, Baytex expects to supply 92,000 barrels per day (bpd) in Eagle Ford.

Different key belongings for Baytex are mild and heavy oil belongings situated in Canada, the place the corporate produces one other 60,000 bpd.

The worth proposition provided by Baytex shares is very simple.

On the buying and selling worth of slightly below $6 per share as I write, the free money movement yield for Baytex shareholders is unbelievable.

With West Texas Intermediate crude oil costs approaching $90 per barrel as I write, Baytex is now providing a free money movement yield of greater than 30%.

With oil at $80 and even $70 per barrel, the free money movement yield from Baytex shares on the present share worth is engaging.

And in terms of earnings investing, understanding free money movement is essential.

Free money movement is extra money {that a} enterprise is throwing off.

This money may be returned to shareholders within the type of dividends or share buybacks, or it may be used to strengthen the company steadiness sheet.

A ten% free money movement yield is generally one thing I’d contemplate very engaging. At present, Baytex has triple that.

And Baytex administration’s plan for this extra money has been clearly articulated.

With the just lately accomplished acquisition of Ranger Oil, Baytex’s complete web debt elevated to $2.6 billion.

Till the corporate’s web debt is lowered to $1.5 billion, Baytex might be utilizing 50% of free money movement to cut back debt, and the opposite 50% might be directed to dividends and share repurchases.

Sensible.

As soon as debt is lowered to $1.5 billion, 75% of free money movement might be returned to shareholders via dividends and repurchases.

The decrease the debt, the larger the dividend payout.

Provided that Baytex is projected to have annual free money movement of just about $1.5 billion at present oil costs, it isn’t going to take lengthy to convey its debt down to focus on ranges.

Then, more money may be returned to shareholders.

The Worth Meter charges shares of Baytex Power as being “Extraordinarily Undervalued.”

Baytex shares may double and nonetheless not be costly.

When you’ve got a inventory that you just’d prefer to have rated by The Worth Meter, depart the ticker image within the feedback part beneath.

{kind=link}