Retirement doesn’t need to be an all-or-nothing proposition on the subject of drawing earnings versus incomes extra of it. This column advocates a few issues: one, drawing steadily on increasingly a number of streams of earnings; and two, persevering with a minimum of on a part-time foundation the stream of earnings generally known as earned earnings.

Certainly, an evaluation commissioned by Larry Berman, host of BNN’s Berman Name and Chief Funding Officer of ETF Capital Administration, confirmed the highly effective affect of incomes simply $1,000 in part-time earnings every month between the age of 65 and 75; or within the case of {couples} $2,000 a month between them.

The evaluation ready by ETF Capital’s Fabien Ouellette vividly reveals that in comparison with incomes nothing further in any respect after the standard retirement age of 65, incomes such modest quantities of additional earnings (whether or not as a part-time worker or on a self-employed foundation) magically accomplishes two issues.

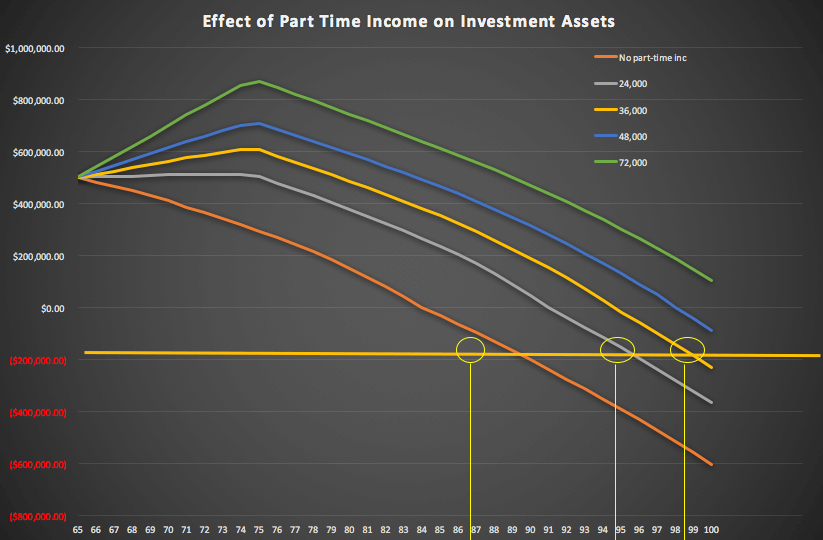

Within the case of a retiree with life-style bills of $60,000 who undertakes a full-stop retirement at 65, incomes no further earnings, there’s a sharp fall in a $500,000 (mixed registered and non-registered) portfolio beginning at age 65. By the point they attain their early 80s, the nest egg is depleted to zero. (That is proven within the orange line within the graph beneath.)

The result is far completely different for a pair incomes simply $2,000 a month between them part-time after 65 and going till 75 (proven because the gray line within the chart). That’s about $250 per week per partner. The dramatic impact is that even that modest quantity of earnings delays the portfolio’s drop beneath zero past their early 90s. In the course of the ten-year interval of working part-time, not solely does the nest egg not decline the primary ten years, nevertheless it really rises! The impact is that by the point you attain 75 and at last cease working even part-time, the portfolio declines from a better degree and far more steadily.

In fact, the extra you’re employed, the higher: for a pair incomes $3,000 a month between them (the yellow line), the portfolio nonetheless has greater than $200,000 by their 90s! Equally, the evaluation additionally reveals what occurs in the event you work further exhausting, which many would possibly argue wouldn’t even qualify as retirement and even semi-retirement. At $4,000 a month (proven in blue) the portfolio is barely depleted in any respect by the point they attain 100!

Lastly, in essentially the most excessive case of incomes $6,000 a month – which is just about a full-time job for a lot of – the portfolio virtually doubles to $870,000 by age 75 and just about by no means declines beneath zero, irrespective of how prolonged your longevity proves to be. (That’s proven within the inexperienced line on the chart).

Bear in mind, even within the latter excessive case of working virtually full-time to 75, you stop to work in any respect after that age—however the advantages of these ten years of part-time work prolong proper to the tip of even an extended lifetime. ETF Capital cautions that its calculations relied on sure assumptions on market returns, tax charges and what you do with the excess cash, and that counting on further work at this age is NOT an alternative choice to a very good monetary plan.

We may after all speak concerning the social, well being and different advantages of working part-time in retirement (along with the monetary advantages mentioned right here) however that might require a complete ebook to explain. The truth is, I’ve simply co-authored a ebook on simply that topic, an excerpt of which ran within the current Summer time situation of MoneySense, and which is talked about beneath.

Jonathan Chevreau is MoneySense’s Retired Cash columnist and the founding father of the Financial Independence Hub. He will be reached at [email protected]. He and Michael Drak have simply revealed the ebook Victory Lap Retirement.

{kind=link}