When you’re something like my expensive departed father, it’s possible you’ll not have to learn any of my new “Retired Cash” columns, that are devoted to fixing cash administration challenges for retirees. You see, my dad was an Ontario high-school instructor and the lucky beneficiary of the well-known outlined profit (DB) lecturers’ pension plan.

He didn’t want to fret about investing—he owned solely GICs and would proudly declare that he didn’t know a inventory from a bond. Not like you, expensive reader, he didn’t have to. With a paid-for dwelling, his GICs, instructor’s pension and authorities CPP and OAS, Dad was laughing in his basic “do-nothing” retirement. He may take lengthy walks, learn to his coronary heart’s content material and entertain neighbours with glasses of sherry. Oh, and cheer for the Montreal Canadiens.

His two sons, and readers of their era, could also be much less lucky. For starters, solely a minority of staff benefit from the sort of inflation-indexed assured pension that Dad—and his widow—loved. Second, most of us can be fortunate to generate 2% a 12 months if these GICs have been held at present, versus 5%-plus a era in the past. Third, whereas Dad lived to 87, at present’s retirees ought to fear about longer life expectations. Longevity is each a blessing and a curse. You probably have good genes and a wholesome way of life, your elevated lengthy life means it’s possible you’ll be negatively impacted by the brand new regular of low rates of interest and the shortage of an actual pension for all times. You’ve gotten a greater likelihood of working out of cash earlier than you run out of time.

A fourth wrinkle in your fortune is inflation. It’s low and seems innocuous now however stays an inevitable and insidious destroyer of wealth and buying energy. The longer you reside, the extra inflation will degrade the standard of any retirement nest egg you have got managed to assemble.

It’s a horrible pity that fashionable employers are loath to supply the sort of DB pension my dad loved. For this reason the Liberal authorities and all provinces however Quebec noticed match to “modestly” broaden the Canada Pension Plan. Too late for these already or almost retired however for at present’s younger individuals, an expanded CPP would be the closest factor to the pension my father loved (not nearly as good, however shut).

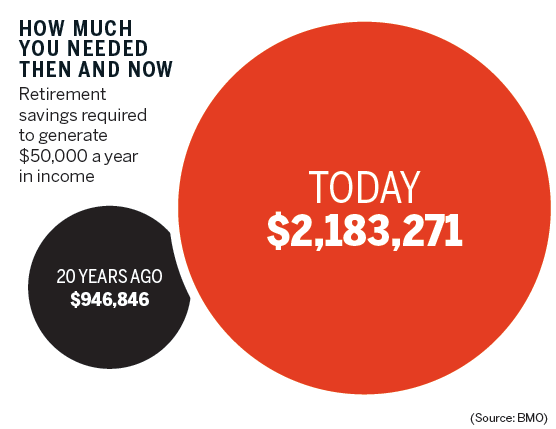

Even after CPP is totally expanded, it’s going to cowl off solely a couple of third of your working earnings (an increase from 25% of pensionable earnings which it has been doing). To generate the remainder of the earnings wanted, it will likely be vital so that you can learn publications like this one and take duty for studying about investing. When corporations shed DB pensions or not make them accessible to new hires, they’re dumping duty on your monetary future from their very own shoulders onto these of their staff.

Low rates of interest and inflation could be blamed on authorities, by which I imply the world’s central banks (together with Financial institution of Canada) that dance to the tune of the mighty U.S. Federal Reserve.

It’s a disgrace about declining pension protection but it surely’s a downright crime what governments are doing to savers. Removed from encouraging us to avoid wasting, those self same low charges frequently tempt customers to go deeper into debt. You is usually a saver, positive, however you’ll pay for it. As retired actuary skilled Malcolm Hamilton instructed me, “We have now a disaster with central financial institution insurance policies and damaging rates of interest, which makes saving [outside tax shelters] roughly futile.”

Curiosity earnings is taxed on the prime marginal fee, larger than “dangerous” belongings like shares. Buyers whose primary wealth is in RRSPs, TFSAs and non-registered investments are caught between the rock of minuscule (and even damaging) rates of interest and the onerous place of dangerous shares, which at at present’s nosebleed valuations may severely right at any second.

There’s a phrase for this struggle on savers: monetary repression. It’s a travesty, however I don’t see this altering in what’s left of most of our lifetimes. How to deal with it will likely be the raison d’être of this column. There’s by no means been such a robust want for assist in dealing with your investments in retirement, to battle again in opposition to the repression. “Retired Cash” will make that battle its mandate, whereas additionally taking a look at semi-retirement as a result of, sadly, many people will be unable to afford the “Full Cease at 65” my father loved.

Jonathan Chevreau is the Founding father of the Monetary Independence web site and co-author of Victory Lap Retirement

{kind=link}