If you’re eager on worth investing, as I’m, whether or not the inventory market is overvalued issues a ton. And these days, I discover myself questioning this as a rule.

It shouldn’t be a tough query to reply. However what I’ve found is that few traders even need to know the reply.

Why? As a result of most appear to care little about intrinsic worth and are as an alternative extra all in favour of perceived worth. The thought appears to be “So long as there’s a higher idiot prepared to purchase my shares for extra, it’ll work out ultimately.”

That’s nice wishful pondering. Nevertheless it’s exactly the improper approach to strategy investing. Each long-term traders and short-term merchants should care about what they’re shopping for – whether or not they intend to carry endlessly or flip for fast features.

Profitable traders perceive that shares’ costs ultimately comply with their true worth, though timing that convergence isn’t all the time straightforward. As Warren Buffett famously put it, “Value is what you pay; worth is what you get.”

Not figuring out (or caring) if an funding is underpriced or overpriced means making monetary selections at midnight.

However I assume, pricey reader, that you’re extra considerate about your wealth than most – and neither afraid of nor apathetic to monetary actuality.

So… are shares presently overvalued? Let’s discover the reply.

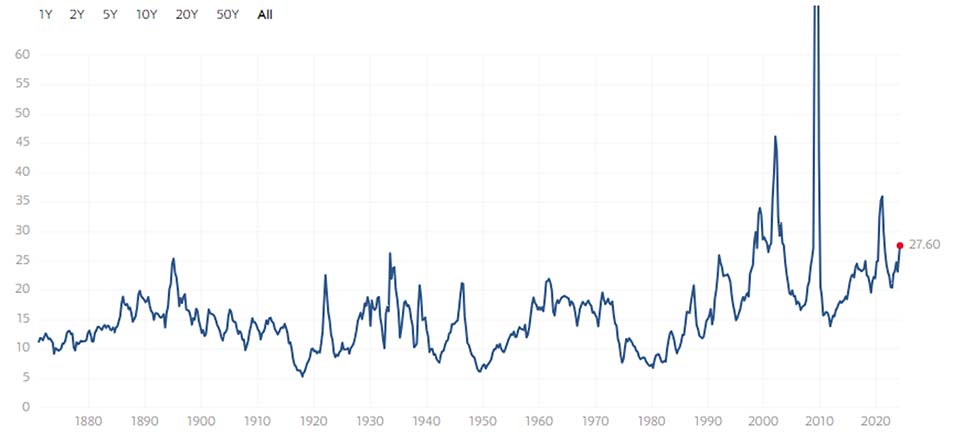

One of many easiest methods most people attempt to reply this query is by turning to a so-called worth a number of. For instance, the price-to-earnings (P/E) ratio – a inventory’s worth divided by its earnings per share – is extensively used as a gauge of whether or not shares are low-cost or costly.

Over 150-plus years, the S&P 500’s common P/E has been about 16. However proper now, it’s about 72% increased at 27.6.

So it appears like we’ve gotten our reply. Shares are overvalued. Plain and easy.

However we’re not fairly performed but…

You see, whereas P/E is straightforward sufficient to grasp, it’s not with out flaws. In truth, it could possibly be seen as oversimplifying the image.

Another is Nobel laureate Robert Shiller’s cyclically adjusted price-to-earnings (CAPE) ratio, which components in inflation and enterprise cycles by utilizing common inflation-adjusted earnings over 10 years.

The market’s present CAPE ratio of 34.2 is double its long-term common of 17. So similar to P/E ratio, the CAPE ratio is telling us valuations are increased than they’ve been traditionally.

However not like P/E, the CAPE ratio says one thing extra…

Shares aren’t simply overvalued. They’re extraordinarily overvalued.

In truth, the CAPE ratio has been this excessive solely 4% of the time.

This needs to be alarming. However as I already famous, most retail traders and merchants don’t appear to care as a lot about valuations as they used to. (It’s as if they will’t think about a cause NOT to purchase shares.)

On condition that so few care, do these excessive valuations actually matter ultimately?

Completely, sure.

Historical past has repeatedly confirmed that there’s a real value of overpaying for shares: a lot, a lot decrease long-term returns.

Even decrease than these of risk-free property.

Once more, let’s flip again to the CAPE ratio.

At any time when the market’s CAPE ratio has topped 30, shares have tended to underperform Treasurys over the next 10-year interval. (And, once more, CAPE is presently close to 35.)

Sure, you learn that proper. We’re speaking in regards to the highest-performing asset class in historical past underperforming the most secure asset class on the earth… by a large margin.

Frankly, it’s embarrassing – particularly when you think about how value-blind traders are as of late. Nevertheless it’s a lesson they’ll must study a method or one other.

The underside line is that this: By no means get comfy overpaying as a inventory investor. It comes with an enormous – and completely avoidable – value to your wealth in the long term.

Be considerate about your wealth, and all the time take into account worth.

Or else.

Be wonderful,

Anthony

{kind=link}