Bengen printed his findings within the October 1994 situation of the Journal of Monetary Planning, later popularizing them within the e book Conserving Consumer Portfolios Throughout Retirement. His secure 4% annual withdrawal charge was dubbed “The 4% Rule” or “The Bengen Rule.” It described the utmost annual withdrawal charges (adjusted for inflation) that guarantee buyers received’t outlive their cash over a 30-year retirement. Over a decade later, in 2006, Bengen loosened the rule a bit for U.S. buyers, for withdrawal as much as 4.5% for tax-sheltered funding accounts and 4.1% for taxable ones.

Nevertheless, in as of late of minuscule and typically detrimental rates of interest, monetary planners are extra cautious about 4%, some preferring to pencil in 3%. (Within the final situation of MoneySense, it was famous that the rule could also be too excessive a proportion for these aged 65 however too low for these 75 or older.) Even the identical journal that Bengen was in later printed The 4% Rule will not be Protected in a Low-Yield World, by Wade Pfau. It argued that until bond returns revert to their historic ranges inside 10 years, 32% of nest eggs would “evaporate early.” In a Morningstar article, Pfau added {that a} nest egg with 40% in equities might withdraw solely 2.8% a 12 months initially to have a 90% likelihood of lasting 30 years. But, in 2013 T. Rowe Worth discovered a portfolio with 60% shares might use an preliminary withdrawal charge of 4.3%.

Clearly, retirees dwelling on capital should pay shut consideration to asset allocation, tax effectivity and precise spending ranges. Markets have so much to do with it, unpredictable although they could be. Within the unique 4% formulation, Bengen used the worst 30-year retirement interval within the final 90 years: the 1973-1974 recession had each excessive inflation and deep market declines. The Vanguard Group recommended “a extra dynamic method” that varies withdrawal charges with market efficiency. It discovered a 50/50 asset combine and a 3.8% withdrawal charge adjusted to inflation would have an 85% likelihood of lasting over 30 years.

Whether or not you go along with a cautious 3% or a extra aggressive 4% or 5% charge with expectations of slowly digging into capital over time, retirees ought to understand that linear projections can not indefinitely be projected into the long run. Doug Dahmer, president of Burlington-based Emeritus Retirement Options, says retirees should think about years when spending will leap effectively past regular withdrawal ranges. Typical expenditures will probably be house-related upkeep like changing a roof or furnace, shopping for a brand new automobile, or pricey “as soon as in a lifetime” world excursions.

Then there’s inflation. The calculation is comparatively easy. Word Bengen’s 4% is used when opening the portfolio at retirement. That fastened greenback quantity is adjusted for inflation every subsequent 12 months. For instance, with a gap steadiness of $500,000, 4% is $20,000 within the first 12 months. With a 2% inflation the withdrawal quantity will probably be $20,400 the next 12 months. If inflation had been 3% the 12 months after that, you then’d multiply $20,400 by 1.03 to get $21,012.

Regardless of all of the variations, one advisor nonetheless likes and makes use of the 4% rule. John DeGoey, portfolio supervisor with Toronto-based Industrial Alliance Securities Inc. and writer of The Skilled Monetary Advisor, makes use of a tweak he calls the “Rule of 16.” He says sustainable depletion charges rely partly on the age you begin to attract down a portfolio. “The sooner you begin, the decrease the mandatory depletion charge.” DeGoey divides the quantity 16 into the consumer’s age for a goal “secure depletion charge quantity” listed to inflation. So in case you retire and begin to attract down your portfolio at 64, dividing by 16 offers you precisely the 4% annual withdrawal charge. Retire earlier and the speed drops; retire later and the speed rises, which is what you’d count on. Somebody who retires at 72 can take out greater than 4% and really feel secure, DeGoey says: “Until we’ve got one other Nineteen Thirties cycle, or that particular person lives to 103!”

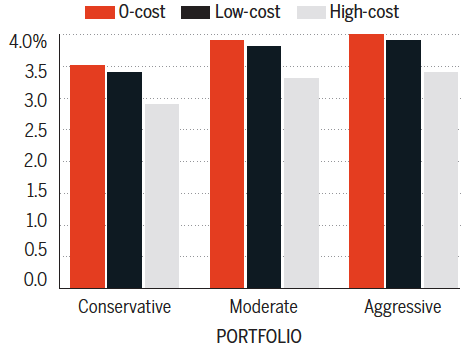

Planning horizon (30 years)

Hypothetical portfolio withdrawal charges assuming 30-year planning horizon

![Bitcoin [BTC] holders anticipating a bear market floor should read this](https://nourishmoney.com/wp-content/uploads/2022/10/harrison-kugler-35Ma3Hy_5yU-unsplash-1-1000x600-75x75.jpg)

{kind=link}