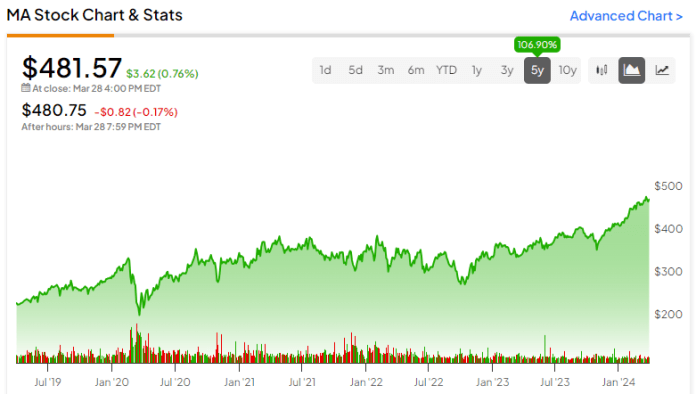

Mastercard inventory (NYSE:MA) boasts a wonderful monitor document of delivering compounding returns. Duopolizing the cardboard processing area with Visa (NYSE:V), Mastercard has grown effortlessly, capitalizing on the shift towards a cashless society and rising shopper spending developments. Mixed with its high-margin enterprise mannequin and buybacks aiding EPS development, MA inventory has grown right into a compounding machine—recording annualized returns of 21.5% over the previous decade—a pattern poised to persist.

Thus, I’m bullish on the inventory.

The Financial system Stays Sizzling, Bolstering Mastercard’s Development

Surprisingly to traders, and maybe even to the Fed, the economic system has defied expectations by staying sizzling regardless of the sharp rate of interest hikes of 2022 and 2023. Client spending has grown in 13 out of the final 14 quarters. All through this era, unemployment has constantly remained beneath 4%, with February’s price sitting at a wholesome 3.9%. Concurrently, February noticed inflation at 3.2%. Positive, it stays larger than the Fed’s excellent goal, however it’s nonetheless inside manageable bounds.

Taking a look at this knowledge, it’s not unreasonable to counsel that the Fed has seemingly achieved, or is on monitor to attain, the much-desired gentle touchdown state of affairs. It seems that rates of interest might want to keep elevated for an extended period than initially anticipated, given the energy of the economic system, even on this local weather. In any case, the unbelievable resiliency the U.S. economic system is showcasing continues to bolster Mastercard’s development. Even higher, this pattern seems poised to proceed based mostly on Wall Road’s consensus estimates.

As an instance, in FY 2023, Mastercard recorded revenue growth of 13% to $25.1 billion. To indicate you the way great Mastercard’s momentum is, understand that this double-digit income development price got here after FY 2022’s 18% and FY 2021’s post-pandemic-rebound-infused development of 23%.

Once more, this development continues to be pushed by robust fundamentals within the total economic system. With the labor market remaining robust and unemployment remaining low, rising wages and rising spending preserve fueling Mastercard’s high line. It’s also possible to see the energy in shopper spending by taking a look at cross-border funds, whose volumes rose by 24% final yr. The journey trade’s discretionary nature signifies that robust cross-border fee volumes point out vigorous discretionary spending.

Wall Road anticipates that Mastercard will proceed rising revenues at comparable charges, a minimum of for the following few years. Consensus income estimates counsel development of 12.0%, 12.6%, and 12.3% in FY 2024, FY 2025, and FY 2026, respectively. Mixed with the potential for margin enlargement and buybacks, Mastercard’s earnings, and thus, inventory worth, seem set to maintain compounding for the foreseeable future.

Excessive Margins, Buybacks, To Compound Complete Return Prospects

To say that Mastercard’s margins are excessive is an understatement. As a result of frictionless, royalty-like nature of its enterprise mannequin, the corporate’s gross margin is basically 100%. Whereas the corporate spends fairly a bit on R&D and SG&A, working margins constantly hover above 50%. Mastercard’s revenue margins are additionally simple to broaden because of the enterprise mannequin’s scalability. Final yr, Mastercard’s working margin rose from 55.2% to 55.8%.

On the identical time, Mastercard’s ongoing buybacks preserve boosting EPS development. The corporate purchased again about $9.1 billion value of inventory final yr. Whereas this will likely translate to a buyback yield of nearly 2%, buybacks have confirmed extremely accretive over the long run as a consequence of Mastercard retaining its excessive development charges extensively. For context, the corporate has repurchased and retired practically 29% of its shares since 2011.

These developments are set to persist, which, mixed with the corporate’s vigorous development price estimates, are anticipated to compound EPS and, thus, returns. Particularly, the consensus EPS estimates forecast a five-year CAGR of 17%, that means that EPS development over the medium time period is anticipated to exceed the income development estimates acknowledged earlier.

One may argue that Mastercard’s premium valuation may cap the inventory’s complete return prospects regardless of the slightly spectacular EPS development forecasts. Nonetheless, I’d disagree. Mastercard inventory just isn’t low cost, however it’s not costly both, in my opinion. At 33 occasions this yr’s anticipated EPS, I consider that Mastercard is kind of pretty valued given such an optimistic medium-term EPS forecast and the truth that this is among the deepest-moat companies on this planet.

Provided that Mastercard has traditionally traded at a premium, future returns are prone to compound in step with the corporate’s underlying double-digit development, primarily signaling a promising medium-term complete return outlook.

Is MA Inventory a Purchase, In response to Analysts?

Taking a look at Wall Road’s view on the inventory, Mastercard maintains a Robust Purchase consensus score based mostly on 28 Purchase and one Maintain suggestion assigned up to now three months. At $515, the typical MA stock price target implies 6.9% upside potential.

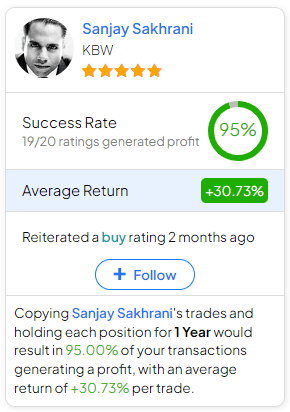

In case you’re questioning which analyst you must comply with if you wish to purchase and promote MA inventory, probably the most worthwhile analyst overlaying the inventory (on a one-year timeframe) is Sanjay Sakhrani from KBW, with a median return of 30.73% per score and a 95% success price. Click on on the picture beneath to be taught extra.

The Takeaway

In conclusion, I consider that Mastercard’s dominance within the card processing trade, together with a slightly favorable financial panorama, positions the inventory for continued good points. Undeniably, Mastercard’s robust income development prospects, pushed by sturdy shopper spending developments, and much more promising EPS development prospects reinforce its standing as a compounding machine. Thus, although the valuation does certainly appear to be it carries a premium, long-term traders are prone to proceed to be rewarded properly.

The put up This Compounding Machine Stays Intact – TipRanks Monetary Weblog appeared first on FinanceGrabber.

{kind=link}