The markets had been reeling towards the tip of final week as scorching CPI figures despatched the most important indexes right into a tailspin. In the meantime, it stays to be seen how Iran’s missile and drone assault on Israel on Saturday evening shapes the struggle within the Center East and impacts market sentiment within the week forward.

Trying on the larger image on the place the markets are heading, based on Chris Harvey, head fairness strategist from Wells Fargo, buyers shouldn’t fear an excessive amount of proper now. ‘There’s extra room for upside,’ he tells us, in a latest notice on present market circumstances. Harvey expects shares to maintain transferring up; he now places his year-end prediction for the S&P 500 index at 5,535, up from the prior 4,625, implying a acquire of 8% from present ranges.

“In our view,” Harvey says, explaining his place, “the bull market, AI’s secular development story, and index focus have shifted buyers’ consideration away from conventional valuation measures and towards longer-term development and discounting metrics. Because the finish of 2022, buyers’ valuation thresholds appeared to lower whereas time horizons elevated, a operate of this secular optimism. We decreased our fairness danger premium to zero greater than a yr in the past, and now the main focus shifts out to 2025.”

Constructing on this, the inventory analysts at Wells Fargo are searching for the shares that stand to realize as soon as the bull run resumes. They’ve picked out two shares for double-digit returns this yr, and a glance into the TipRanks databanks exhibits that every will get a Sturdy Purchase score from the consensus view. Listed below are the small print, and the Wells Fargo feedback.

GitLab (GTLB)

First up is GitLab, a DevOps agency that has created an open-source platform for DevSecOps. This seems like a mouthful, however employees within the discipline will perceive: GitLab presents its prospects a specialised platform answer to optimize quick, environment friendly software program growth and excessive returns from the tip product. As famous, GitLab’s platform is obtainable as open-source software program; the corporate’s founding idea was that ‘everybody can contribute.’ The corporate’s open-source mannequin permits all of its customers to, in the event that they want, change into contributors to the platform code; because of this, the mannequin includes a quick tempo of innovation.

The open-source platform additionally feeds straight into GitLab’s ‘freemium’ enterprise mannequin, with a base degree of entry and repair out there to all customers whereas higher-level performance and upgrades, in addition to larger-scale assist, can be found for paying subscribers. GitLab claims to have 1 million paying energetic license customers out of some 30 million complete customers; on the enterprise finish, the corporate employs roughly 2,000 folks in 60 nations all over the world, and has over 3,300 energetic contributors making additions to the open-source platform code.

In latest months and weeks, GitLab has begun folding AI expertise into its software program platform, as a part of an total technique that can use AI, notably generative AI, to ‘remedy buyer ache factors,’ that’s, to resolve customers’ most urgent issues and create a seamless expertise. GitLab has a partnership with Google, to make use of the tech large’s generative AI expertise inside its personal cloud infrastructure; utilizing the tech inside GitLab’s personal cloud will permit the corporate to take care of its personal prospects’ privateness and safety.

Along with branching into AI, GitLab has additionally not too long ago moved to accumulate Oxeye. The acquisition transfer, introduced final month, will carry Oxeye’s cloud-native safety functions and danger administration capabilities into GitLab’s platform, and increase GitLab’s talents in software program composition evaluation and regulatory compliance. GitLab may also acquire performance in tracing vulnerabilities from the code to the cloud, an necessary discipline for an open-source agency.

On its monetary facet, GitLab final reported outcomes for its fiscal interval 4Q24, which ended this previous January 31. Revenues for the quarter got here to $163.8 million, for a 33% year-over-year acquire – and beat the estimates by $5.54 million. GitLab reported earnings of 15 cents per share by non-GAAP measures, beating the forecast by 7 cents per share.

On the unfavourable facet, GitLab’s ahead steering for fiscal yr 2025 predicted a income vary of $725 million to $731 million – whereas the analysts had hoped to see income steering of $732.2 million. Shares in GitLab tumbled by 21% after the miss, and the inventory hasn’t recovered since.

Nonetheless, overlaying this inventory for Wells Fargo, analyst Michael Turrin is impressed by the corporate’s strikes into AI and the chance afforded buyers by the shares’ present relative low cost. He writes, “We imagine GTLB is well-positioned to profit from genAI tailwinds given its code era use-case in Duo Professional — possible the earliest genAI usecase to see adoption in software program, in our view. We est. GTLB’s present alternative could possibly be as a lot as $750M ARR, benefiting from each add-ons of the AI SKU in addition to incremental buyer upgrades… With shares -21% (now -23%) off since 4Q eps, the FY25 mannequin now extra conservatively set, and an AI-led product cycle taking form, we see an opportunistic entry for GTLB shares.”

To quantify his outlook on the inventory, Turrin charges the shares as Chubby (Purchase), with a $70 value goal that signifies room for a 22.5% upside within the coming months. (To observe Turrin’s monitor document, click here.)

GitLab’s 20 latest analyst opinions break all the way down to 16 Buys and 4 Holds, for a Sturdy Purchase consensus score. The shares are priced at $57.07 and their $73.35 common goal value implies a 28.5% one-year upside potential. (See GitLab’s stock forecast.)

monday.com (MNDY)

Sticking with the tech sector, we’ll flip our sights on monday.com, a cloud software program agency that gives prospects a variety of labor administration merchandise. These embody workplace system optimization instruments, mission administration and CRM, and advertising and marketing and gross sales ops instruments, all provided on a cloud-based platform. monday.com targets its merchandise at enterprise shoppers of each scale, making the platform out there to subscribers on the software-as-a-service mannequin. The corporate can depend names equivalent to Coca-Cola and Uber amongst its buyer base.

monday.com was based in 2012, and in its first decade of operation, the corporate earned widespread acceptance primarily based on its repute for high quality and assist – and its easy-to-use, ‘low-code, no-code’ platform. Clients can rapidly adapt monday’s work administration methods to suit their very own wants, primarily based on idiosyncratic enterprise fashions, personnel practices, and operational scales.

Since launching its product in 2014, this firm has constructed itself into the go-to place for work administration software program. The corporate has over 1,800 workers, sustaining a product line out there in some 200 nations – and is utilized by over 225,000 enterprise prospects day by day. We must always notice that 2,295 of monday’s prospects generate greater than $50,000 in annual recurring income every.

That final metric, from the corporate’s 4Q23 report, was up 56% year-over-year, complemented by 833 prospects with over $100,000 in annual recurring income, a y/y enhance of 58%. Altogether, monday.com generated $202.6 million within the quarter, up 35% y/y and $4.83 million higher than had been anticipated. The underside line, of 65 cents per share in non-GAAP measures, was 35 cents forward of the forecasts.

Turning again to Wells Fargo, the agency’s place is clearly said by analyst Michael Berg, who sees loads of potential on this firm and its inventory. Berg writes, “We view monday.com as a pacesetter in a big, $150Bn+ market. With a differentiated work mgmt platform, MNDY has a variety of sturdy development levers to seize market share to drive sturdy development, together with: 1) transfer up-market into the enterprise; 2) a quickly increasing product set to drive up and cross-sell; 3) leveraging a rising accomplice community to drive consciousness and strategic relationships; and 4) pricing adjustments.”

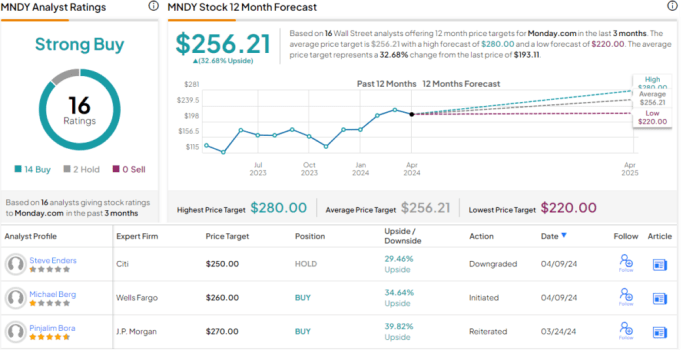

These feedback assist the analyst’s initiation of protection at an Chubby (Purchase) score, and his value goal, set at $260, implies a 34.5% share appreciation over the following 12 months. (To observe Berg’s monitor document, click here.)

Total, monday.com has 16 latest suggestions, together with 14 to Purchase and a pair of to Maintain, for a Sturdy Purchase consensus score. The shares are priced at $193.11 and their $256.21 common value goal is nearly as bullish because the WF take, suggesting a 33% upside on the one-year horizon. (See monday.com’s stock forecast.)

To search out good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Best Stocks to Buy, a instrument that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is extremely necessary to do your individual evaluation earlier than making any funding.

The publish Wells Fargo Says Purchase These 2 Shares for Double-Digit Returns – TipRanks Monetary Weblog appeared first on FinanceGrabber.

{kind=link}