A pivotal occasion on the monetary calendar handed final Wednesday, however I think lots of you missed it.

Every quarter, the Federal Reserve releases a Abstract of Financial Projections (SEP), during which the central financial institution’s high resolution makers reveal their expectations for the unemployment price, GDP and inflation.

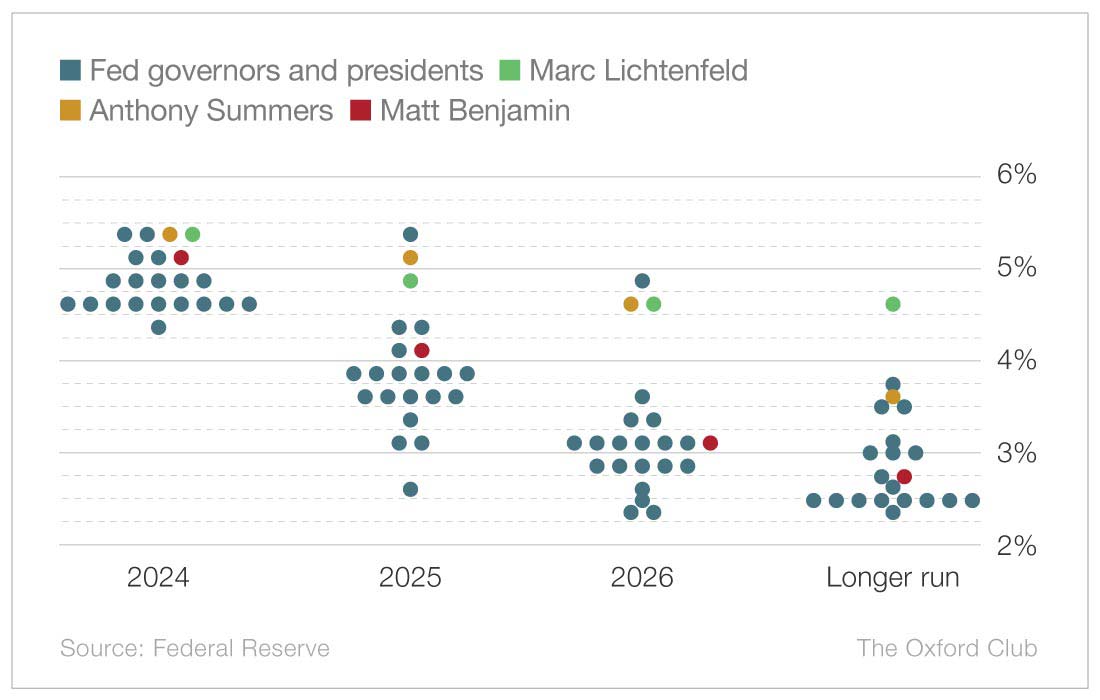

However one part of the SEP tends to attract extra consideration than some other: the dot plot.

It is a diagram that reveals the place the Fed’s presidents and governors – together with Fed Chairman Jerome Powell – imagine rates of interest are headed within the coming years.

Beneath, you’ll see a mannequin of the Fed’s most up-to-date dot plot, which was launched final Wednesday. The blue dots in every column signify the federal funds price projections from the Fed’s seven governors and the presidents of its 12 particular person banks.

However we’ve added a enjoyable twist for you…

To maintain the Fed trustworthy, we’ve added three extra dots in every column to signify the expectations of three of our personal Oxford Membership consultants: Chief Revenue Strategist Marc Lichtenfeld, Director of Buying and selling Anthony Summers and Senior Markets Knowledgeable Matt Benjamin.

As you possibly can see, our consultants aren’t as optimistic because the Fed about future price cuts.

Now, predicting the place rates of interest will land a number of years prematurely is a idiot’s errand. As we all the time say, we’re not within the enterprise of market timing. However rates of interest can have a big impression on each the markets and the financial system, so wanting on the historic information and considering forward could be extremely helpful (and worthwhile!).

Marc, Anthony and Matt went into extra element on the thought course of behind their predictions beneath…

Marc Lichtenfeld

Chief Revenue Strategist

I don’t imagine the Fed has garnered this a lot consideration since CNBC used to attempt to guess the route of rates of interest by how full former Fed Chairman Alan Greenspan’s briefcase looked.

Within the Annual Forecast Subject of The Oxford Revenue Letter in January, I went towards the grain and stated rates of interest wouldn’t drop by a lot – if in any respect – in 2024 as a result of lack of a recession and the potential for inflation to proceed burning too brightly.

Thus far, that’s been the case. Initially of the yr, the consensus was that there could be six price cuts in 2024. Right now, based on each the Fed’s dot plot and the federal funds futures market, that quantity is down to a few.

However I don’t imagine there will probably be any.

Inflation, whereas down considerably, remains to be not shut sufficient to the Fed’s 2% goal. February’s shopper value index studying was 3.2%. That’s not horrible, nevertheless it’s nonetheless removed from the Fed’s aim.

I’ve stated many occasions earlier than that I don’t imagine Powell desires to go down in historical past because the Fed chair who allowed inflation to reignite below his watch.

This yr can be an election yr. I don’t imagine Powell desires to do something that might be seen as politically motivated. A price minimize at this level would probably draw the ire of Donald Trump, who would possibly accuse Powell of making an attempt to slant the election in President Biden’s favor.

Lastly, there are at the moment no indicators of a recession.

We’re, nevertheless, approaching the primary yr of the presidential cycle, which is usually when recessions happen. There have been 10 recessions since 1948 (not together with the COVID-19 recession, which was a black swan occasion). Of these 10, seven occurred throughout the first yr of the presidential cycle.

The rationale for this development is the primary yr of a president’s time period is the very best yr for him to make robust choices, as a result of he has three extra years to win again favor with the voters.

So I wouldn’t be stunned to see a slowdown in 2025, which may immediate the Fed to decrease charges to round 4.75%-5%.

Anthony Summers

Director of Buying and selling

I feel there’s a slim probability that the Fed cuts charges this yr.

There are two predominant information factors that strongly undermine the case for decrease charges. The at the beginning is sticky inflation.

Over the previous two years, the Fed has made great progress in taming inflation. From its June 2022 excessive of 9.1%, it’s down roughly two-thirds to three.2%.

That’s nonetheless too excessive, although – about 60% increased than the Fed’s long-term goal of two%.

If inflation stays sticky, the Fed may have no motive to decrease charges. In truth, that might strengthen the case for increased charges, particularly given the financial system’s present power.

That brings me to the second information level: financial development.

Final yr, many analysts – myself included – had been skeptical of the Fed’s “smooth touchdown” speak. The financial information was far too blended to counsel issues had been going easily.

Nevertheless, our financial system seems a lot stronger as we speak than it did six months in the past. To see this, let’s contemplate the common of actual GDP and actual GDI (gross home revenue).

Each GDP and GDI measure the full worth of our financial output, though they calculate it in a different way. I favor the common of the 2 as a result of it can provide us a extra correct sense of our financial system’s total power, particularly when each GDP and GDI are transferring in the identical route.

Within the third quarter of 2023 (which is the final quarter for which we have now actual GDI information), the common of actual GDP and actual GDI rose by 3.4%. That was the biggest enhance since 2021, and it marked three consecutive quarters of actual financial development.

Sturdy financial information offers the Fed extra leverage to lift charges, permitting it to proceed preventing inflation with out concern of pushing our financial system right into a recession.

The Bureau of Financial Evaluation will launch fourth quarter actual GDI information this Thursday, March 28, together with its third estimate of fourth quarter GDP. I anticipate one other sturdy report.

Matt Benjamin

Senior Markets Knowledgeable

Predicting the course of rates of interest isn’t any simple process.

That’s as a result of the Fed actually is data-dependent. The Federal Open Market Committee (FOMC) will chart its course on rates of interest primarily based on the financial information that is available in… and the evaluation of that information by the 400 Ph.D. economists it employs.

And since predicting what the financial system will do is inherently troublesome, making projections on rates of interest can be tough – and it will get more and more troublesome the additional out in time you challenge. Due to this fact, my price forecast can be largely primarily based on what I imagine the financial system will do.

And take into account that any form of sudden provide or demand shock – like one other COVID-19 flare-up, an oil value spike, and so on. – would power us to throw all our projections out the window.

However assuming these issues don’t happen, I’m optimistic concerning the financial system for a number of causes, together with the strong labor market, rising shopper optimism and robust shopper spending, to not point out the surprisingly wholesome state of households’ funds (I simply regarded on the amount of cash in Individuals’ checking accounts – wow!).

These issues ought to hold the financial system and labor market buzzing by means of the tip of 2024, they usually’ll additionally hold inflation elevated above the Fed’s long-term 2% goal.

For me, that claims there will probably be few, if any, price cuts this yr. And three different elements counsel that the Fed will probably be reluctant to chop charges by greater than 50 foundation factors earlier than the tip of 2024.

First, there’s the presidential election. Although the Fed is nonpolitical, Powell and his colleagues wish to keep out of the fray if in any respect doable. So, all different issues being equal, they could wish to wait till after Election Day to change rates of interest in any important manner.

Second, I feel Fed officers wish to hold charges excessive – that manner, they’ve some ammunition to make use of if (and when) there’s an financial downturn or sudden shock.

Lastly, there’s the inventory market. Although the Fed would deny this, it’s clear it has reacted to market downturns previously with extra accommodative financial coverage. However this bull market appears to want little assist from Powell and firm. In truth, regardless that futures merchants have been paring again their expectations for price cuts since mid-January, the market has continued its rally.

The FOMC will meet six extra occasions this yr. I see, maybe, one minimize by yr’s finish and reasonable cuts over the following two years, with the federal funds price ultimately settling close to the Fed’s long-term impartial price, which neither stimulates nor restricts financial development.

[Editor’s Note: Interested in getting more commentary like this? Send your questions to mailbag@oxfordclub.com!]

{kind=link}