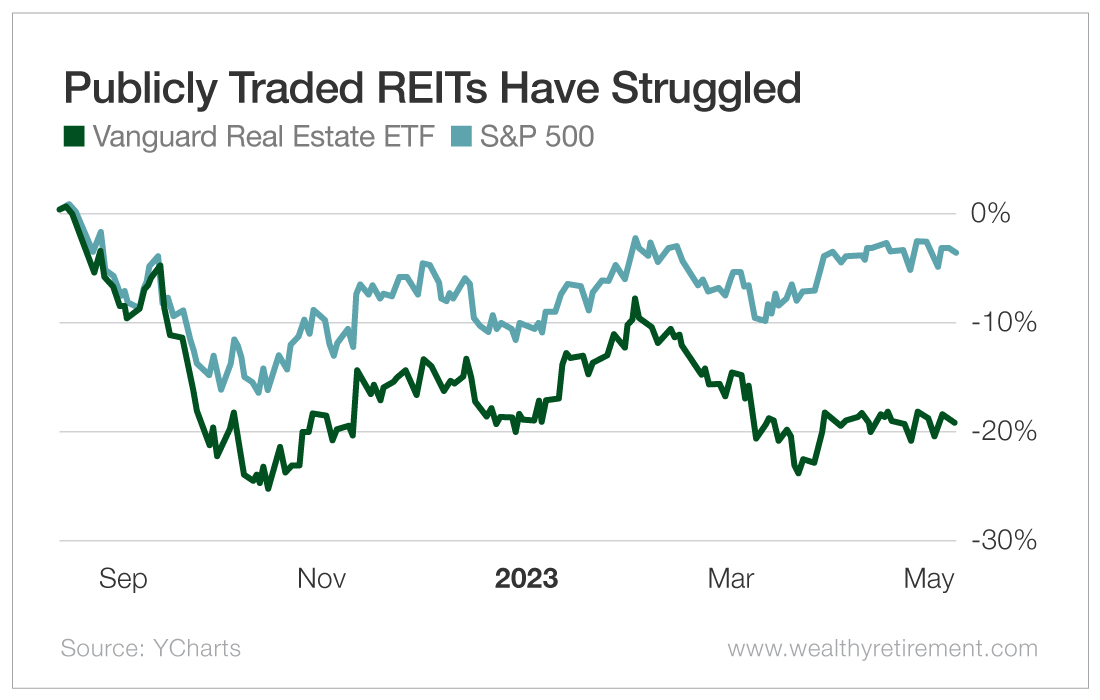

The previous 9 months haven’t been enjoyable for actual property funding belief (REIT) buyers.

The Vanguard Actual Property ETF (NYSE: VNQ) is in bear market territory, down nearly 20% from the place it traded final fall.

That’s a lot worse than the three% decline within the S&P 500 over the identical interval.

The fast rise in rates of interest has pushed the downturn within the REIT sector.

REITs use debt to finance parts of the true property they personal. Rising rates of interest imply increased curiosity bills, which negatively impression earnings.

Additionally placing a damper on the REIT sector are the record-high business workplace emptiness charges within the U.S. Within the first quarter, workplace vacancies hit a regarding 18.6%.

The work-from-home pattern isn’t good for workplace landlords.

The considerations that buyers have concerning the REIT sector are legitimate. However when a complete sector will get bought off like this, you possibly can wager some infants get thrown out with the bathwater.

On this case, Alexandria Actual Property Equities (NYSE: ARE) is one such child.

ARE REIT on Our Radar

Alexandria is concentrated on a really particular actual property area of interest. Its actual property is rented by pharmaceutical and healthcare corporations.

As an alternative of standard workplace areas, Alexandria owns properties which can be specialised to swimsuit the pharmaceutical and healthcare companies that use them.

These properties are distinctive and never interchangeable with the common workplace buildings which can be at present experiencing excessive emptiness charges. Because of this Alexandria’s tenants won’t be leaving the corporate for cheaper workplace area down the road.

Alexandria’s 2023 earnings outcomes converse to the truth that this isn’t simply one other plain previous workplace REIT.

Within the first quarter, 94% of Alexandria’s rental area was occupied. That charge was the identical a yr in the past, and it’s far superior to these of Alexandria’s REIT friends.

And even higher, the typical rental income that Alexandria receives from its tenants elevated by a document 48% within the first quarter!

Clearly, the REIT emptiness downside isn’t affecting Alexandria. Not solely are Alexandria’s occupancy ranges excessive, however the lease being generated from tenants has additionally skyrocketed.

Rising rates of interest are additionally not an issue for the corporate.

Over 96% of its debt is mounted at a mean rate of interest of simply 3.6%, that means rising rates of interest have had just about no impression on the enterprise.

Plus, the typical remaining time period on that debt is greater than 13 years. So Alexandria is locked in at wonderful borrowing charges for a very long time to return.

Regardless of being insulated from the components which have crashed the REIT sector, Alexandria’s share value has fallen 30% over the previous yr.

With this sell-off, Alexandria’s shares look attractively priced. The inventory is at present buying and selling at simply 65% of the corporate’s internet asset worth.

Which means we’d be paying simply $0.65 on the greenback in opposition to the worth of the belongings that Alexandria holds.

On high of that, Alexandria pays a really safe dividend, which now yields nearly 4%.

An inexpensive value and a giant dividend yield is a pleasant mixture.

The REIT sector is down huge, and this has created a really good alternative to personal shares of this high-quality REIT at a gorgeous entry value.

The Worth Meter charges Alexandria Actual Property as “Extraordinarily Undervalued.”

{kind=link}