Right here’s a easy query for you: Are you spending greater than you earn every month?

Let’s get much more particular: Are you spending precisely what you earn every month?

In the event you create a zero-based price range, that’s exactly what you’ll be doing. Imagine it or not, it’s a easy price range plan that ensures you’ll spend each Casadefinance Reader you make every month in a productive method.

Sound scary? Belief us, it’s the furthest factor from it. We clarify precisely what zero-based budgeting is and the way this budgeting type might help you.

What Is Zero-Based mostly Budgeting?

The zero-based price range — also referred to as zero-sum budgeting or ZBB if you happen to’re hip on company finance — is a technique of month-to-month budgeting through which each greenback you make is spent or saved consistent with your targets and bills.

Zero-based budgeting is a well-liked strategy in enterprise, however you don’t need to be sitting within the boardroom for the annual budgeting course of to make it be just right for you. You can begin utilizing the knowledge of this budgeting methodology to start out getting a deal with in your private funds.

For example, When you’ve got $4,500 coming on this month, you’ll allocate precisely $4,500 throughout all of your payments, discretionary bills, financial savings funds and monetary targets.

The right way to Make a Zero-Based mostly Funds

Budgeting will get a nasty status. However the reality of the matter is that setting an incredible price range doesn’t prohibit you — it truly units you free. And in comparison with conventional budgeting, the zero-based price range is essentially the most customizable and versatile price range on the market.

Right here’s find out how to make a zero-based price range that matches your funds, life-style and targets.

Step 1: Decide Your Earnings

Step one to determining your zero-based price range is to trace precisely what you earn every month. Which means all of your aspect jobs, bonuses, tax refunds, presents, irregular earnings — every thing. Any deposit that’s made to your checking account must be accounted for.

For many people, this may differ month to month. Do your finest to make an informed prediction of what your earnings might be. You’ll be able to at all times add to it or take away from it all through the month.

For our instance, let’s say you carry house $4,500 monthly.

Step 2: Record Your Recurring Bills

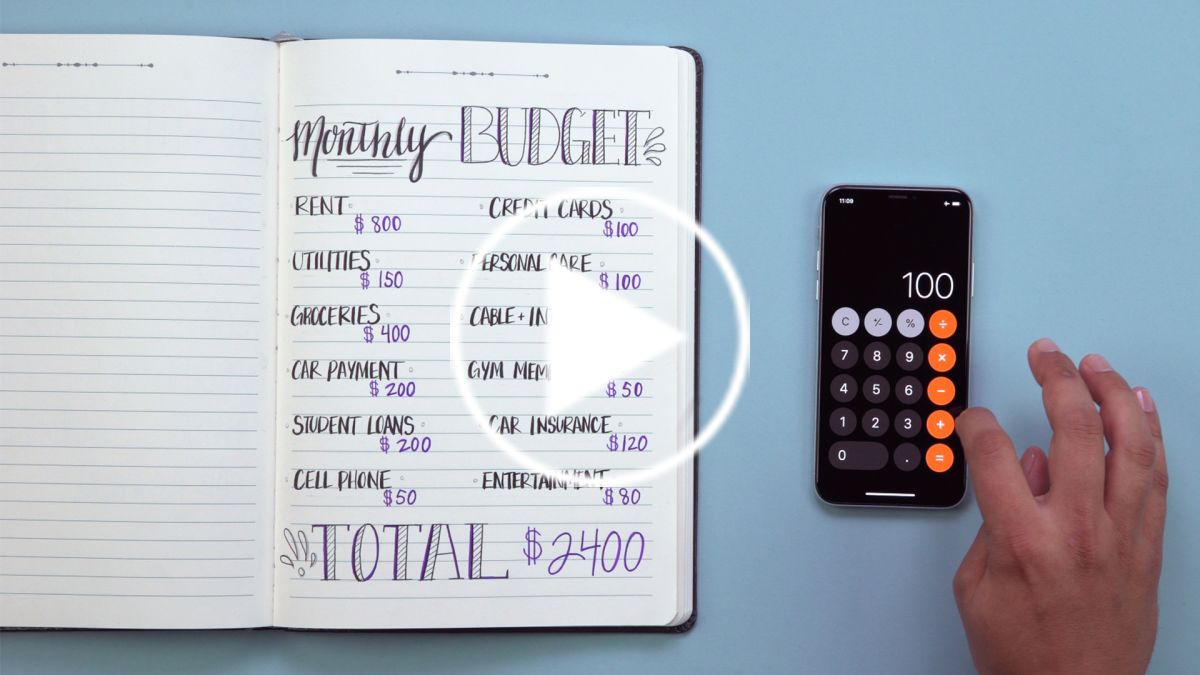

Begin with the payments you recognize you’ve got every month, like your hire or mortgage, utilities, cellphone, web, cable, automobile insurance coverage and automobile cost. These expenditures must be pretty steady, so that you’ll in all probability understand how a lot cash to allocate for these prices.

Subsequent, undergo your financial institution statements for the final 90 days to see what you’ve spent on discretionary purchases, like shopping for garments or consuming out. This will sound daunting, however you’re in all probability extra predictable than you suppose, so that you’ll begin to see a sample fairly rapidly.

Lastly, embody bills that you simply solely pay a few times a yr. This can embody payments like HOA charges or license and registration renewals.

Your record may look one thing like this:

Consider Your Present Spending

| Fundamentals | Providers | Debt/Financial savings | Misc | Whole |

|---|---|---|---|---|

| Housing $1,455 | Insurance coverage $275 | Automobile cost $235 | Garments $145 | |

| Gasoline $200 | Mobile phone $145 | Bank card cost $500 | Leisure $345 | |

| Groceries $400 | Web $45 | Scholar loans $220 | Consuming out $400 | |

| Utilities $135 | Netflix $15 | Financial savings $0 | Items $35 | |

| … | … | … | Miscellaneous $100 | |

| $2,190 | $480 | $955 | $1,025 | $4,650 |

It’s OK if in case you have variable bills or often spend quite a lot of enjoyable cash on a month-to-month foundation. Look over your earlier month’s price range to see precisely the way you had been spending cash and what classes you need to trim or broaden in your new price range.

Step 3: Set Your Objectives

A conventional budgeting course of takes your earnings minus prices and places no matter is leftover towards investments or financial savings. Not like earlier budgets you might have used, a zero-based budgeting system makes financial savings and investments a part of the plan.

Earlier than you begin constructing your price range, take a second to think about your monetary targets. Are you excited to get rid of your debt? Making an attempt to pad your emergency fund? Working to make amends for your retirement contributions? All good targets.

A zero-based budgeting system is nice for attaining monetary targets rapidly, as a result of there’s no proportion cap on how a lot cash you possibly can put each month towards anyone class.

Step 4: Prioritize Your Expenditures

You’ll be able to hold your value classes broad (housing, transportation, targets, discretionary) or break them down in as a lot element as you need. For the needs of value administration, it might be useful to solely escape the bills the place you wrestle with overspending. It’s as much as you.

However nevertheless you break them down, you’ll need to prioritize these prices by significance. What’s essential to survive ought to at all times be first, adopted by the quantity you need to allocate to your monetary targets. Then end along with your discretionary bills.

Step 5: Race to Zero

Relying on the place you’re at after budgeting, you’ll both must shave some {dollars} off your price range and decrease prices or allocate some additional.

Further {dollars} can simply be added to your top-priority targets or used to provide somewhat bump to your discretionary spending. Consider this as an motion you’re taking month-to-month towards balancing your annual price range consistent with your monetary targets and priorities.

The instance price range above contains $4,650 of bills, however our earnings is barely $4,500. So on this case, our budgeter must resolve the place to seek out $150 in value financial savings.

In case your price range is prioritized and lists bills by significance, you possibly can reduce prices by working from the underside or lowest precedence expenditures till you’ve eliminated $150:

The right way to Trim Spending

| Previous spending | New price range | Reduce | |

|---|---|---|---|

| Garments | $145 | $145 | $0 |

| Leisure | $345 | $345 | $0 |

| Consuming out | $400 | $385 | $15 |

| Items | $35 | $0 | $35 |

| Miscellaneous | $100 | $0 | $100 |

Alternatively, you would reduce prices in different areas or get rid of spending classes altogether till you refine your value administration strategy.

You could have to chop again on one film or skip a pair meals out to satisfy these new numbers, but it surely appears cheap, proper? To save cash on groceries, it might merely imply preserving a more in-depth eye on offers and never shopping for stuff you don’t really want or are inclined to waste.

The Professionals and Cons of Zero-Based mostly Budgeting

Zero-based budgeting is straightforward, but it surely’s not simple. It takes quite a lot of upfront dedication to get all the advantages. Listed below are some positives and negatives to weigh earlier than you dive in.

Zero-Based mostly Funds Professionals

- Helps establish areas of overspending

- Permits for greater allocation of earnings to monetary targets

- Customizable to suit earnings and priorities

Zero-Based mostly Funds Cons

- Extra time-consuming than incremental budgeting

- Includes reallocation all through the month

- Tougher to keep up as a result of extra inflexible budgeting course of

Zero-Based mostly Budgeting 101: The right way to Deal with Surprising Bills

The largest concern with zero-based budgeting is “spending” all of your cash each month. However this shouldn’t be an issue so long as you’ve got a buffer.

Some individuals hold an emergency fund in a separate or linked financial savings account. Others will hold an additional $1,000 or $2,000 in a checking account. Nonetheless others need a full month of bills sitting of their account earlier than they begin utilizing a zero-based price range.

The selection of how a lot buffer you’re snug with is as much as you. However you will have a buffer of some type in your checking account to keep away from being penalized for unintended overdrafting.

Past a buffer in your checking account, put the remainder of your emergency fund in a high-yield financial savings account the place it could possibly earn curiosity for you.

Zero-Based mostly Funds vs. 50/30/20

The 50/30/20 methodology is a well-liked various to the zero-based price range. However what makes them totally different?

Within the 50/30/20 methodology, 50% of your month-to-month earnings goes to requirements, 30% to desires and 20% to financial savings and debt reimbursement. Some individuals use the 50/30/20 methodology by itself as a fast and straightforward system, however it could possibly even be a baseline for zero-based budgeting or different strategies.

Whereas each strategies are nice, they serve totally different targets. So long as your earnings can accommodate the odds, a 50/30/20 price range is ideal for these simply beginning out.

But when 50% of your earnings isn’t sufficient to cowl requirements, or if you wish to put greater than 20% towards financial savings targets, then a zero-based price range is a better option for you.

Zero-Based mostly Budgeting Apps

Need assistance getting organized? There are budgeting apps and budgeting software program geared in direction of the zero-based budgeting system. Our favourite is YNAB (You Want a Funds), which is an app chock stuffed with particulars and instruments to get you began.

Take a look at our suggestions for each free and paid user-friendly budgeting apps for newcomers.

Is Zero-Based mostly Budgeting Proper for You?

Regardless of its reputation within the enterprise world, not everybody thrives on a zero-based budgeting course of. For these making an attempt to manage how they spend cash, chances are you’ll need to use different budgeting strategies to seek out value financial savings earlier than going to a zero price range.

On the flip aspect, a zero-based price range is a good strategy for these making debt funds or making an attempt to turn out to be debt free on a variable earnings. It’s a budgeting methodology that forces your checking account stability to be allotted towards priorities and helps establish the place slashing prices may make an actual distinction earlier than the following price range cycle.

Tyler Omoth is a former senior author at The FinanceGrabber who loves absorbing the solar and discovering artistic methods to assist others. Kaz Weida, a senior author at The FinanceGrabber, contributed

{kind=link}